The U.S. energy storage industry entered 2026 at a breakneck pace, deploying 9.7 GWh of new capacity in the first quarter. The historic performance marks the strongest Q1 on record for the sector, representing a 32% increase over the same period last year.

According to the U.S. Energy Storage Market Outlook Q2 2026, released today by the Solar Energy Industries Association (SEIA) and Benchmark Mineral Intelligence, the record-shattering quarter comes amid escalating global geopolitical tensions, including conflicts in Iran that have severely disrupted international gas and turbine supplies.

As investors, developers, and grid operators look to hedge against the resulting energy price volatility, solar-plus-storage and standalone battery assets are rapidly solidifying their status as critical infrastructure. The insulation from global fuel price shocks has driven analysts to upwardly revise the long-term domestic forecast, with the U.S. now projected to install 613 GWh of cumulative storage by 2030.

“Energy storage’s remarkable first quarter only underscores the fundamental values of this technology: it’s insulated from fuel price shocks, keeps electricity costs down, and strengthens grid reliability,” said Darren Van’t Hof, interim president and CEO of SEIA.

However, the industry faces a complex political landscape. While demand signals have never been stronger, federal permitting bottlenecks threaten to artificially throttle deployment. SEIA analysis shows that 467 solar and storage projects currently have permits pending and remain highly vulnerable to politically motivated delays or cancellations.

The market continues to be heavily anchored by large-scale utility deployments, though distributed sectors maintained a steady baseline in the first quarter.

- Utility-Scale: The front-of-the-meter segment remains the leader in capacity additions, accounting for 7.8 GWh of the Q1 total.

- Commercial & Industrial (C&I): Businesses and industrial users added 648 MWh of capacity to insulate themselves from grid pricing spikes.

- Residential: Homeowners deployed 515 MWh of behind-the-meter storage, continuing a steady expansion that saw the residential segment surge 51% in 2025 alone.

Five trends

An analysis of the updated data highlights the core themes shaping the energy storage market over the next 12 months:

- Data centers drive “speed-to-power” demand: Generative AI and hyperscale computing are outstripping the grid’s ability to provide traditional interconnections. Tech giants like Google and Meta have signed massive procurement deals for tens of thousands of megawatt-hours of energy storage so far this year. To manage massive millisecond training loads and bypass utility bottlenecks, data center developers are increasingly co-locating large-scale battery energy storage systems (BESS).

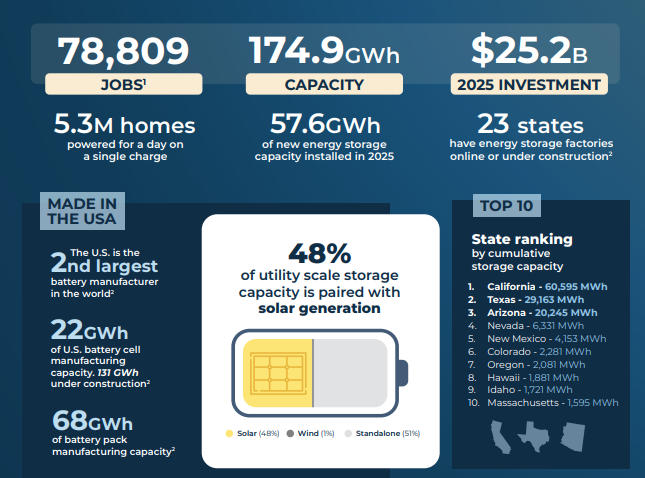

- Red state boom: Geographically, the largest utility-scale markets remained concentrated in California, Texas, and Arizona. However, 71% of all utility-scale capacity installed in Q1 was built in states carried by President Donald Trump in the 2024 election. Emerging markets like Georgia, Iowa, and Mississippi also posted notable capacity gains, demonstrating that state-level economics and grid-reliability needs are overriding partisan divides.

- Dramatic cost deflation: Rapid manufacturing scaling and improving battery supply chains have fundamentally altered project economics. The average price for utility-scale energy storage has plummeted by 55% since 2022. This sharp deflationary curve has offset rising capital costs elsewhere in the supply chain, allowing the standard battery duration for new projects to stabilize at an average of 3 hours.

- Standalone storage: While solar-plus-storage has long led the market, standalone storage installations have officially claimed the majority share, now accounting for 51% of utility-scale storage capacity. Paired solar-plus-storage projects represent 48% of the market, while wind-paired configurations hold a nominal 1%. The shift highlights a growing developer preference for deploying batteries independently to maximize revenue through energy arbitrage and ancillary grid services.

- Domestic manufacturing: Driven by domestic content incentives, the U.S. has cemented its position as the second-largest battery manufacturer in the world. Twenty-three states now have dedicated energy storage factories either online or under construction. The domestic supply chain currently boasts 22 GWh of operational battery cell manufacturing capacity, including 131 GWh actively under construction, alongside 68 GWh of active battery pack assembly capacity.

Long-term outlook

Despite regulatory friction, the mid-term trajectory for the storage sector remains aggressively upward. Front-of-the-meter utility deployment is expected to experience a 256% surge in cumulative capacity by 2030, while the residential market is forecasted to expand by 108% over the same timeframe.

“Energy storage is no longer just for backup, it’s critical energy security infrastructure,” said Shan Tomouk, BESS and energy lead at Benchmark Mineral Intelligence. “A supportive policy landscape for BESS will be crucial to enabling the rollout of AI and data centers, while mitigating adverse cost impacts to regular consumers.”

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.