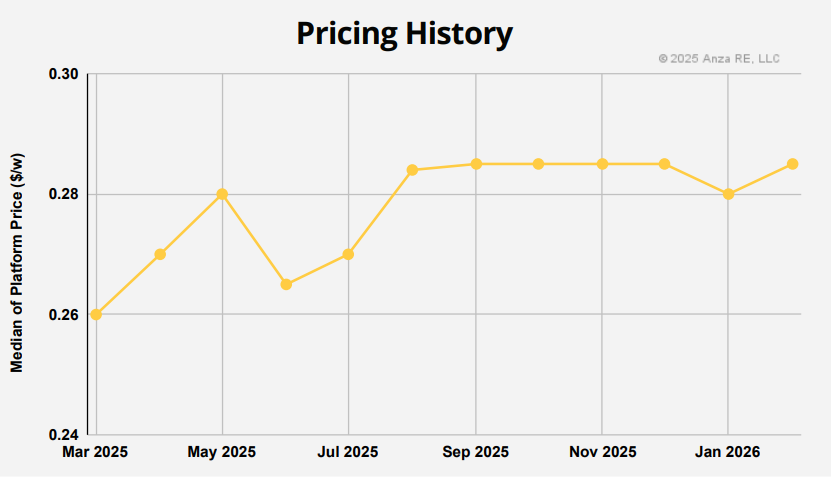

The U.S. solar market entered 2026 navigating a landscape defined by regulatory shifts and the persistent threat of supply chain disruptions. Following a year of volatility where median pricing rose by as much as 14% between January and November 2025, the first quarter of 2026 has seen prices hold at an elevated baseline.

The current stabilization at $0.28 per watt represents a shift from the $0.25 per watt levels seen in early 2025, driven by the convergence of Anti-Dumping and Countervailing Duty determinations and the tightening of domestic content eligibility.

Higher prices are driven in part by stricter Foreign Entity of Concern (FEOC) rules. Under the Treasury Department’s updated guidance, projects seeking to qualify for the full 10% Domestic Content Bonus under the Inflation Reduction Act must navigate requirements regarding prohibited foreign entity material assistance. For projects beginning construction in 2026, the applicable threshold percentage for non-PFE produced property stands at 40% for solar facilities and 55% for Energy Storage Technologies. These thresholds are scheduled to escalate by 5% annually, creating urgency among developers to secure compliant hardware before the 2027 step-ups.

Anza’s data, which aggregates median pricing from more than 40 suppliers representing over 95% of the U.S. module supply, highlights a growing price delta between compliant and non-compliant hardware. FEOC-compliant modules have seen a steady price increase of approximately 4.9% as supply chains reorganize to exclude components from restricted entities. In contrast, modules that do not meet FEOC standards saw a more aggressive price spike of 9.2% during the previous safe harbor rush.

Anza noted a convergence in the pricing of mainstream cell architectures. Mono PERC saw its historic price advantage over newer technologies nearly disappear. Median pricing for Mono PERC modules stood at approximately $0.275 per watt in Q1. This represents a 4.2% increase from late 2025 levels, as buyers favored the mature supply chain of PERC to mitigate risks associated with newer technologies.

Tunnel Oxide Passivated Contact (TOPCon) technology is currently priced at a median of $0.285 per watt. While TOPCon previously commanded a more significant premium, patent litigation among Tier-1 suppliers has introduced a layer of caution for some buyers. Despite these intellectual property concerns, the efficiency gains of TOPCon continue to drive high demand in the utility-scale segment. Heterojunction (HJT) modules remain the most expensive mainstream option, holding at $0.39 per watt. The HJT market is characterized by limited U.S. availability, with pricing driven more by specific cell origin and tariff status than by broader market commoditization.

The domestic manufacturing landscape is also showing signs of bifurcated pricing. Modules utilizing U.S.-made cells command the highest premium in the market, with prices at $0.46 per watt. The price reflects a 5.7% increase, as developers compete for a limited pool of domestically produced cells required to maximize tax credit value.

Conversely, U.S.-assembled modules that utilize imported cells have seen more volatility. Pricing for these hybrid domestic products rose to $0.36 per watt, a nearly 6% increase from the previous quarter. Many buyers are blending domestic modules with imported units or high-value domestic balance of system components like racking and inverters to hit the 40% domestic content threshold while managing overall capital expenditure, said the report.

Imported module pricing has remained relatively flat at $0.265 per watt for products not subject to the most severe trade penalties. However, the shadow of the Section 232 investigation looms over these figures. The investigation, which aims to determine if imported solar components pose a national security threat, could lead to new universal tariffs or quotas.

Furthermore, the anticipated AD/CVD determinations on imports from India, Indonesia, and Laos have begun to influence procurement strategies. Modules from Southeast Asian countries already affected by trade policy saw a 7.7% price increase late last year, and while they have eased slightly, they remain higher than pre-litigation levels.

In the Energy Storage System sector, the pricing trajectory has diverged from that of solar modules. Battery storage pricing has continued to decline, providing a counterbalance to rising module costs for integrated solar-plus-storage projects.

For a 10 MW 4-hour distributed generation system, the AC Wrap median CAPEX price fell to $212 per kWh, representing a 6.8% decrease. Self-integrated battery systems in the same segment dropped to $173 per kWh. Utility-scale storage followed a similar downward trend, with AC Wrap pricing reaching $194 per kWh and self-integrated pricing falling to $158 per kWh, a 10.6% decline from the peak levels seen in mid-2025. This downward pressure is attributed to falling lithium carbonate costs and an expansion of battery manufacturing capacity outside of China, though Section 301 tariffs on Chinese imports scheduled to hit 25% this year remain a variable.

Looking forward to the remainder of 2026, Anza warns that the status quo of $0.28 per watt module pricing may be short-lived. The potential for Section 232 tariffs on polysilicon and its derivatives could create a new wave of upward pressure, particularly for domestic manufacturers who still rely on imported raw materials.

Additionally, the Treasury’s Cost Percentage Safe Harbor tables, which allow taxpayers to use assigned cost percentages for domestic content calculations, will be a critical tool for developers navigating 2026 construction starts. As the industry moves toward the 40% domestic content requirement, the premium for U.S.-made cells is expected to remain high, further widening the gap between low-cost imported hardware and tax-advantaged domestic products.

The report concludes that procurement strategies in 2026 must be increasingly granular. Buyers can no longer focus solely on the cents per watt sticker price but must instead account for the impact of tariffs, the value of the 10% domestic content bonus, and the long-term risk of supply chain audits under the Uyghur Forced Labor Prevention Act (UFLPA) and FEOC rules.

As the market absorbs these regulatory costs, the baseline for U.S. solar pricing appears to have shifted higher, ending the era of sub-twenty-cent utility-scale modules in the American market.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.