EnergySage released its H2 2025 Home Electrification Marketplace Report on Thursday, revealing how the looming expiration of the residential solar tax credit reshaped the U.S. residential solar market and spurred a 205% increase in homeowner engagement with solar installers on the platform.

The company says the increase in engagement was driven by the July 2025 passage of the One Big Beautiful Bill Act (OBBBA), which eliminated the 30% federal tax credit for purchased residential solar systems installed after Dec. 31, 2025 under Section 25D of the tax code.

This resulted in several shifts in customer and installer behavior, including a major shakeup in market share percentage for several different solar panel manufacturers as installers rushed to purchase any available equipment to complete installations before the year-end deadline.

EnergySage said median pricing on its marketplace during H2 2025 was $2.49 per watt, and average system size was 11.8 kW.

Importantly, the report notes that most installers reported filling their annual capacity by October 2025, causing payback timeframes to jump from 7.4 years in Q3 to 10.4 years in Q4.

Data for the semiannual report, which was pulled from millions of transaction-level data points from shoppers on the EnergySage platform between July and December 2025, also revealed decreases in battery storage attachment and shifts in the solar loan financing market.

Market diversity

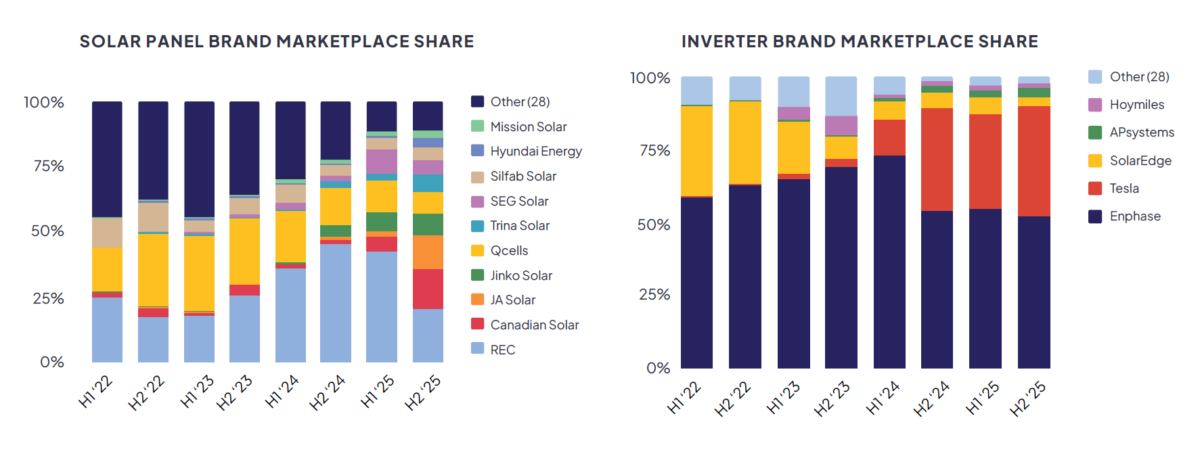

Supply constraints introduced by the rush to install systems before the end of the year forced installers and homeowners to prioritize available inventory over ideal specifications, leading to a broader variety of solar panel manufacturers holding significant market share.

Specifically, the proportion of installations using REC and Qcells modules decreased as brands such as Canadian Solar and JA Solar increased their representation on the marketplace.

Average panel wattage also shifted lower, with panels in the 430–440 W range chosen for 30% of installations (up from 8% in the previous half-year), while the share of installations using 450-460 W panels fell from 33% to 26%.

Image - EnergySage

The share of the market held by various inverter and battery manufacturers did not show the same shifts, with Enphase and Tesla maintaining their dominant positions in these areas.

Image - EnergySage

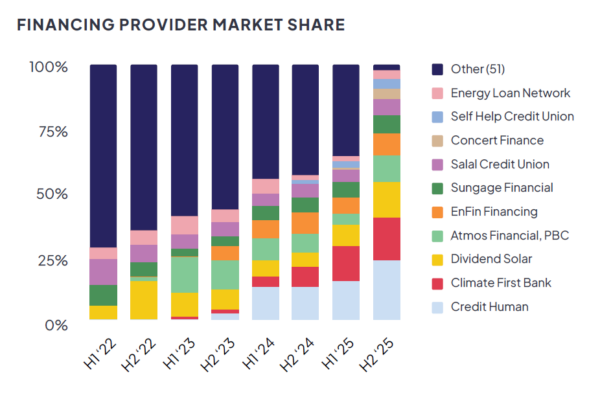

However, financing provider market share did show broader diversity, with the market spreading among a broad variety of solar-specific lenders alongside credit unions and traditional banks.

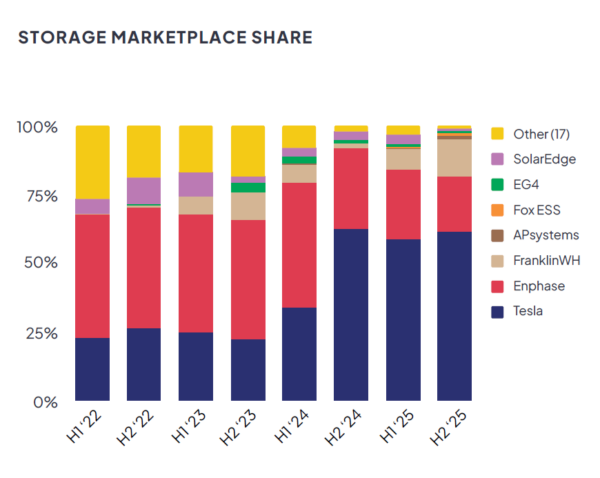

Dips in storage attachment

The report also highlighted a decline in battery attachment, showing the national rate falling from 41% to 38% in the second half of 2025. This drop was more pronounced in high-value storage markets.

California’s attachment rate dropped from 79% to 71%, Texas fell from 61% to 53%, and Hawaii decreased from 100% to 85%.

EnergySage attributed this reduction in storage attachment to installers and homeowners rushing to complete simpler, solar-only installations by the Dec. 31 deadline to secure expiring incentives. The company says that consumer interest in storage remained steady, suggesting that the dip represents deferred adoption and creates a significant retrofit opportunity moving forward.

This trend contrasts sharply with numbers recently announced by Sunrun. In its fourth-quarter earnings report, the company noted a record 71% storage attachment rate on new installations. However, Sunrun mostly installs third-party owned (TPO) systems, for which federal tax credits remain available.

The gap in immediate storage adoption for cash-purchased systems could point to a growing homeowner willingness to sign up for battery-as-a-service or virtual power plant (VPP) programs in the future.

For example, a recently-announced battery-only VPP from SOLRITE Energy allows Texas homeowners — with or without rooftop solar — to get a home battery installed and pay a $20 monthly fee alongside a rate of 12 cents per kWh. Similarly, Base Power offers Texas residents a retail energy plan that includes an on-site battery.

A shift toward whole-home electrification

For the first time, the 22nd edition of the EnergySage report expanded beyond solar and storage to analyze full home electrification, including electric vehicle (EV) charging and heat pumps.

The findings indicate a shift in consumer behavior, with homeowners increasingly moving away from what EnergySage calls “single-point” clean energy products toward a more holistic, whole-home energy management strategy.

A survey of EV charger installers revealed that just 30% of EV charger installers derive more than 50% of their business revenue from chargers alone, demonstrating that contractors are positioning themselves for integrated electrification growth.

A survey of homeowners who have used the EnergySage platform to shop for heat pumps revealed strong purchase intent, with 67% of homeowners said they definitely prefer a heat pump over other HVAC options. Survey respondents listed upfront costs, long-term energy savings and installer qualifications as the three most important priorities in their search — above government incentives and environmental impact.

Trends for 2026

Looking ahead, the industry is entering a new phase shaped by the post-Section 25D tax credit landscape.

As the residential industry faces new deadlines of July 4th, 2026 to safe harbor long-term solar projects and December 31, 2027 to install projects not covered under the safe harbor rules, EnergySage anticipates the industry could see “a market (that) prioritize(s) speed over specification” similar to the dramatic increase in engagement

This aligns with broader residential solar market trends expected in 2026. With the expiration of the 25D residential investment tax credit for purchased systems, the market is expected to shift heavily toward TPO models like leases and prepaid power purchase agreements, which still qualify for commercial tax credits.

Thousands of new solar households that deferred battery installations in late 2025 are now prime candidates for storage retrofits, but EnergySage said rules restricting products made with assistance from foreign entities of concern (FEOC) from qualifying for the tax credit may cause further pricing volatility.

Additionally, 2026 is set to be a significant year for system maintenance. As the number of older solar installations grows, and as waves of installer bankruptcies leave some system owners orphaned, there is a rising demand for companies that specialize in servicing and upgrading existing systems. EnergySage data shows that nearly 51% of solar installers say they now regularly service solar installations they did not install, with another 40% saying they do so occasionally.

Full reports on the solar, storage and home electrification marketplaces can be found on the EnergySage website.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.