The U.S. Virtual Power Plant (VPP) market is entering a new phase of accelerated growth, according to the inaugural VPP Market Report released by Ohm Analytics, a market intelligence and data firm serving clients in the solar, energy efficiency and home improvement markets.

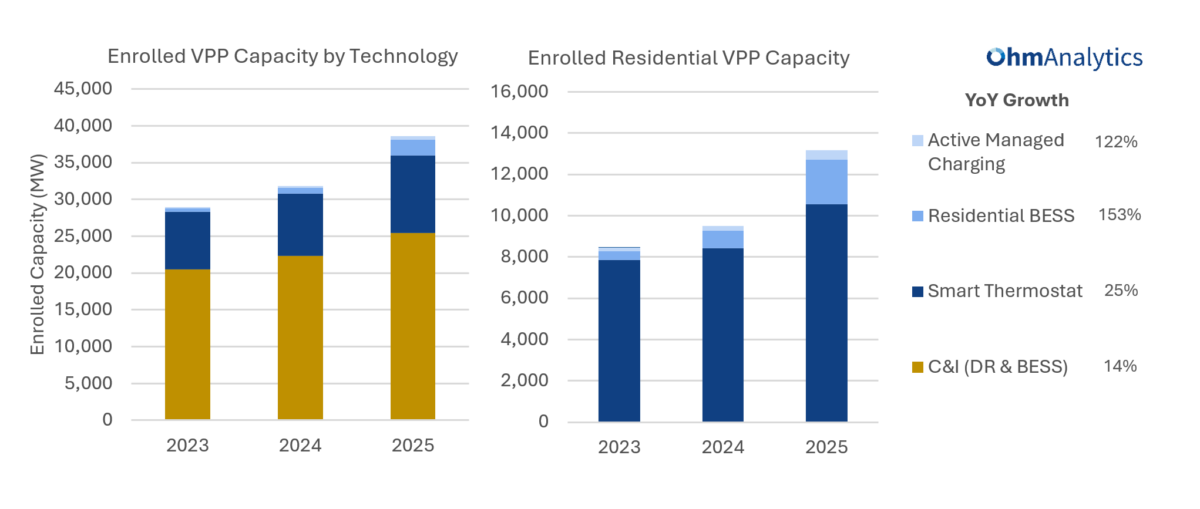

The report reveals a dramatic surge in residential battery enrollments, which grew by an impressive 153% year-over-year in 2025, contributing to an overall 21% increase in total cumulative enrolled VPP capacity, which now tops 38 GW nationwide.

The residential sector — which includes actively managed EV charging, distributed battery energy storage systems (BESS) and smart thermostats — accounted for about one third of overall enrolled VPP capacity at the end of 2025. If its share capacity continued to grow at 2025’s rate, it could overtake that of the Commercial and Industrial (C&I) sector by 2028 if current growth rates hold.

However, California’s decision to cut funding to the Demand-Side Grid Support (DSGS) program could limit capacity growth in 2026. The DSGS program, which is currently the nation’s largest VPP, accounted for 785 MW in capacity growth in 2025.

Ohm Analytics senior research and policy analyst Teddy Storrs says he expects the C&I sector’s share of overall capacity to remain larger for several years into the future, despite residential battery growth. “There’s just so much more bang for the buck out there in the C&I space,” he told pv magazine USA in a recent interview.

The second major driver of residential capacity growth in 2025 was Puerto Rico’s Customer Battery Energy Sharing (CBES+) program, which grew by 460 MW in 2025, following the Puerto Rico Energy Bureau’s approval of auto-enrollment for battery systems.

State-level actions lead the way

While researching the report, the Ohm Analytics team tracked over 150 actions taken by utilities, regulators and legislators in 2025 to actively promote VPPs.

“In the absence of federal leadership on this issue, we’re seeing states pursue really ambitious targets for clean energy for affordability programs that leverage DERs,” Ohm Analytics senior policy and research analyst Madeline Turner told pv magazine USA. “There has been some really great movement from the ground up to solve these issues in real time.”

Noteworthy developments include:

- State legislative momentum: Virginia passed legislation requiring Dominion Energy to launch a 450 MW VPP pilot, while Maryland’s IOU’s are moving forward with VPP program developed in response to the DRIVE Act of 2024 that will result in up to 2% of each utility’s peak load in VPP capacity.

- Location-based incentives: National Grid’s ConnectedSolutions+ program, launched in late 2025, became the first VPP program to offer additional compensation for Distributed Energy Resources (DERs) specifically located on capacity-constrained feeders. And Xcel Energy Colorado’s recently approved Aggregated Virtual Power Plant (AVPP) will incorporate distribution system asset deferral into its incentive structure, offering an avoided cost value of $64.74/kW-year for distribution-level services on eligible feeders.

- Data center market response: VPP providers are making the case that they can scale capacity faster and cheaper than new power plants, and Ohm analysts note 18 new VPP programs proposed by utilities in PJM and the Midwest, largely in response to a projected 100+ GW increase in data center demand by 2035.

Although the growth in VPP programs has been promising, pilot programs still account for 45% of all VPPs, meaning they are not permanently funded. The report’s authors note that continued funding and scaling beyond pilot programs is “mission-critical” to the long-term success of VPPs.

They go on to add that ratepayer-funded programs like those in development in Maryland can be more insulated and stable than programs subject to legislative revocation of funding, such as California’s now-shuttered DSGS program.

The report’s Executive Summary can be found here. Ohm Analytics’ data collection methodology relies on its industry partners, which include some of the largest installers, manufacturers, financiers, and distributed energy resource management (DERMS) providers in the industry.

The full report is available to Ohm Analytics enterprise subscribers. The company also provides select access to its market data platform at no cost to solar contractors and developers.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.