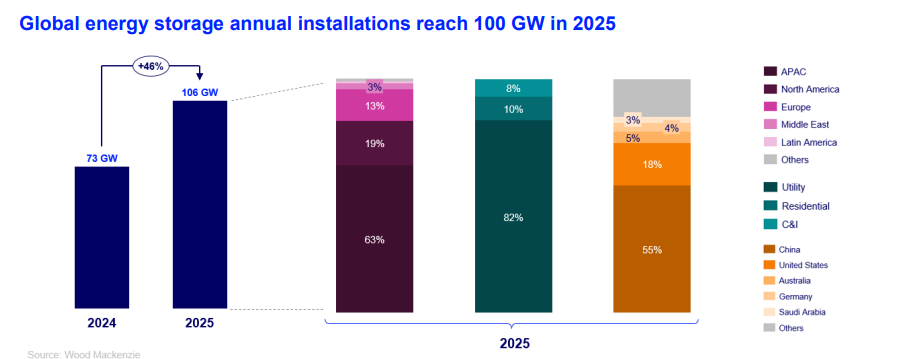

The global energy storage market reached a major milestone in 2025, with annual installations passing 100 GW for the first time. The growth comes despite major policy shifts in the world’s two largest markets, China and the United States.

China has removed its mandate to pair storage with new renewable energy projects. The country is moving toward market-based mechanisms. This creates uncertainty for future revenue.

In the United States, tax incentives remain in place. However, new supply chain constraints are making it difficult to use Chinese battery modules.

Wood Mackenzie’s latest report, “What to look for in 2026: Global Storage,” outlines five trends that will shape the coming year.

1. Supply chain restructuring

Chinese manufacturers are changing how they do business in the United States. To maintain market access, Chinese firms are expected to announce new ownership structures in 2026. Many will reduce their ownership stakes to below 25%, said the report. This move is designed to meet Foreign Entity of Concern (FEOC) requirements.

Supply remains tight, said Wood Mackenzie. Shortages that began in late 2025 will likely continue through mid-2026. The shortage is acute for certified batteries from top-tier suppliers, said the report. Wood Mackenzie expects system prices to stabilize in the second half of 2026.

Chinese suppliers are also looking beyond the U.S. and China and are moving investments into South and Southeast Asia, Europe, and the Middle East. The goal is to gain market share, even if it means lower profits in the short term, said the report.

2. Grid-forming technology

Grid-forming storage is moving from a voluntary option to a requirement in many markets, said the report. Grid-forming systems use inverters can stabilize voltage and frequency on the grid. This is critical as more coal and gas plants retire and intermittent renewables grow.

The European Commission is expected to set a harmonized framework for grid-forming requirements in 2026. Previously, these systems cost 10% to 15% more than standard storage, but that price gap is disappearing, said the report. Manufacturers are now building these features into their standard products at little to no extra cost.

3. Non-lithium batteries scale up

Lithium-ion is the dominant technology, but alternatives are gaining ground. Sodium-ion, flow batteries, and iron-air systems are scaling up. These technologies are becoming cost-competitive for specific uses.

Sodium-ion is seeing significant activity. Peak Energy is working on a 4.75 GWh supply deal with Jupiter Power in the United States. The first 720 MWh phase is part of this growth. CATL also plans to launch sodium-ion batteries specifically for energy storage in 2026.

In Europe, new policy support is helping long-duration storage. The United Kingdom and Italy are using “cap and floor” mechanisms. These help make non-lithium projects more bankable for investors.

4. Data centers drive demand

Large data centers are turning to batteries to bypass grid bottlenecks. The grid often cannot keep up with the power needs of generative AI. Data center developers are co-locating storage to secure faster utility connections.

Data center batteries handle “training loads.” These loads can jump from 10% to 90% capacity in milliseconds. Storage provides the necessary flexibility. While gas turbines remain the top choice for onsite power, storage is now the second most common choice in the data center pipeline.

5. The rise of hybrid projects

Developers are increasingly pairing storage with solar and wind. Hybrid systems help manage curtailment when renewable energy is wasted because the grid cannot receive the generation.

In Australia and India, more than half of the storage projects announced in 2025 were hybrids. In Europe, the trend is also growing. Some regions now see more than 500 hours of negative power prices per year, said the report. These market conditions make standalone solar less profitable. Developers are using hybrid power purchase agreements (PPAs) to protect their revenue.

Regional outlook

The U.S. market faces a temporary slowdown, as Wood Mackenzie projects a dip in 2026 and 2027. It attributes the slowdown to tariff changes and the time needed to restructure supply chains. Growth is expected to recover by 2028, said the report.

Europe was highlighted as a bright spot. Installations in Europe grew by 160% in 2025. Germany leads the market for small-scale, distributed storage, while the United Kingdom is the leader for large, utility-scale projects.

In Latin America, 2026 will be a year of new auctions. Brazil is planning a national storage tender for early 2026. Chile is also updating its rules to better pay storage for providing grid services.

The global transition is moving forward. Energy storage is no longer just a backup, and it is becoming the primary tool for grid reliability.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.