The virtual power plant (VPP) market broadened more than it deepened over the last year, found Wood Mackenzie’s annual North American virtual power plant market report.

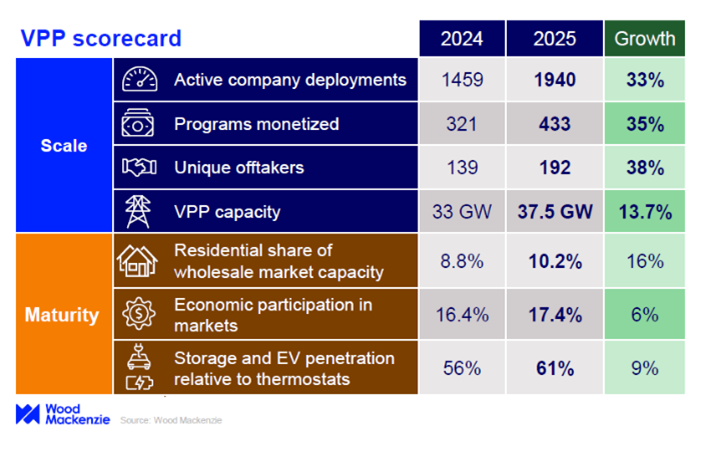

Company deployments, unique offtakers, and programs monetized each grew over 33% year-over-year. This reflects pull from new flexibility buyers as well as push from new VPP players, many who are filling new roles in the value chain.

“An ‘independent distributed power producer’ business model has emerged, whose thesis is that energy arbitrage and grid service revenue can finance an electricity retailer’s third-party-owned storage offering,” Wood Mackenzie said.

At the same time, overall VPP capacity grew 13.7%. This more modest growth indicates a market that is broadening faster than it is deepening, Wood Mackenzie said.

“Utility program caps, capacity accreditation reforms, and market barriers have prevented capacity from growing as fast as market activity,” said Ben Hertz-Shargel, global head of grid edge at Wood Mackenzie.

Enrollment caps on utility programs, capacity accreditation reforms in power markets, such as the migration to effective load carrying capability, and market barriers to small customers have limited capacity growth in existing programs, according to Wood Mackenzie.

Interestingly, Wood Mackenzie found VPP offtakes were the largest where utility data center commitments were the largest. California, Texas, New York and Massachusetts are the leading states, comprising 37% of all VPP deployments. However, the regions with the greatest utility commitments to data center capacity, PJM and ERCOT, were also found to have the greatest disclosed VPP offtake capacity.

“This drives home the opportunity for utilities and even hyperscalers themselves to procure new VPP capacity to offset data center coincident peak demand, enabling faster grid connection,” Wood Mackenzie said. “In this way homeowners and business owners might actually earn revenue from the connection of new data centers, offsetting potential bill increases.”

Wood Mackenzie said that while hardwire providers are understandably enthusiastic about utilities as a new sales channel, the majority of other VPP companies do not support utilities rate basing DER.

But doing so could limit private capital and aggregator access to the DER market, Wood Mackenzie said. “There is far more enthusiasm for utilities integrating DER into system planning and operations, specifying where such resources are needed, but letting the market supply them, via customer programs and competitive solicitations.”

Doing so will enable the market to find the lowest-cost solution and drive innovation across the whole value chain, from program marketing to cross-technology optimization.

VPP critics of utility ownership see a utility monopoly of capital deployment choking off private capital and aggregator access from the DER market. According to Wood Mackenzie, the critics would rather customers and third-parties own assets and utilities procure grid services from them through customer bring-your-own-device programs, procurement contracts and flexibility markets.

“In other words,” Wood Mackenzie said, “they would likely get behind the [distributed capacity procurement] model without utility ownership.”

(Also read: How to leverage virtual power plants for a better grid & After liftoff, DOE looks to accelerate virtual power plants)

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.