Amid policy uncertainty—and perhaps even because of it—the U.S. is expected to continue its record-setting pace of solar capacity deployments through at least 2027—right up until it hits the dual barriers of “Foreign Entities of Concern” (FEOC) restrictions and the scheduled phase-out of key solar tax credits.

BloombergNEF’s Jenny Chase told pv magazine USA that the group projects U.S. solar photovoltaic installations of 53.1 GW in 2025, rising to 61.1 GW in 2026. In 2027, installations are expected to dip slightly to 59.8 GW before plunging to 32.2 GW in 2028.

These projections assume that FEOC-related regulations will present significant headwinds, limiting developers’ access to qualifying components.

BloombergNEF offers a more optimistic scenario in which the industry navigates FEOC challenges more effectively. Chase and her team suggest that while 2025 and 2026 are likely to proceed as currently projected, 2027 could see a modest boost to 62.6 GW of solar deployed. Most notably, instead of a nearly 50% drop in 2028, capacity additions could remain relatively strong at 56 GW.

From there, installations are expected to rise again, albeit under a revised policy environment.

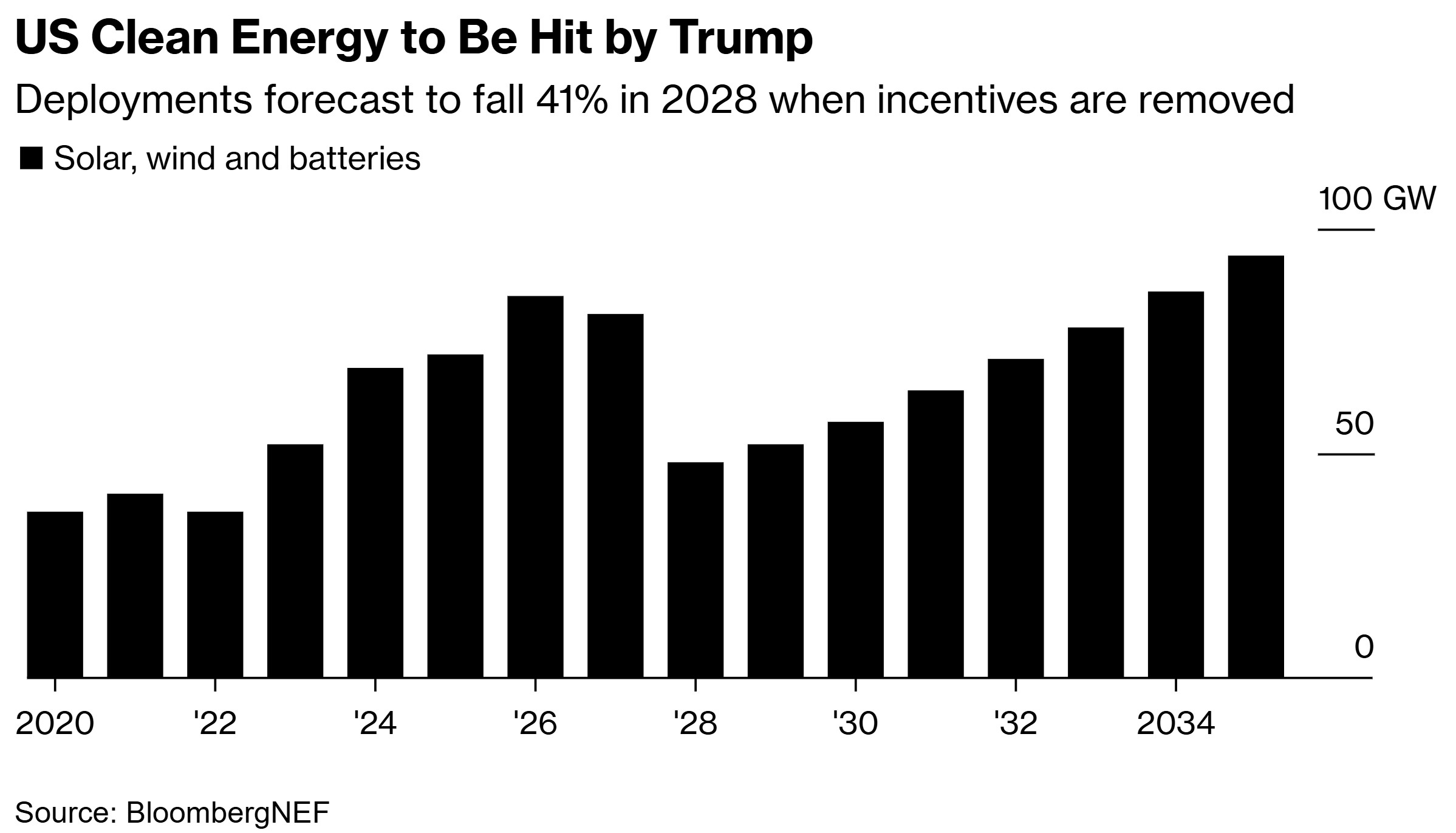

Broadly speaking, BloombergNEF anticipates that in the FEOC-constrained scenario, total wind, solar, and storage deployments will fall by 41% in 2028.

The 41% drop translates to 48 GW deployed in 2028, down from 81 GW in 2027.

Looking through 2030, BNEF now expects cumulative wind, solar, and storage deployments to be 23% lower than in previous forecasts, primarily due to changes to the Inflation Reduction Act. The new analysis projects a 50% reduction in new onshore wind capacity, a 23% decline in solar, and a 7% drop in energy storage installations.

Financial analysis firm Enverus also flagged concerns. It estimates that once the investment tax credit expires, “only 30% of planned solar projects will be able to deliver competitive prices and are ‘expected to survive.’” The firm finds that more than half of planned wind farms will remain competitive by 2027.

Energy storage is expected to weather the changes better than wind and solar. Its projected 7% decline is modest, largely because the tax credit for standalone storage was not only retained but extended an additional year—now expiring at the end of 2033.

The greatest challenge to energy storage will be FEOC restrictions, under which the maximum allowed foreign share (known as the threshold percentage) is set at 45% for projects that begin construction in 2026. That threshold tightens by 5 percentage points each year, reaching 25% for all projects beginning after 2029.

In 2024, only BloombergNEF and the U.S. Energy Information Administration (EIA) correctly projected that the U.S. would install around 50 GW of solar. Other groups initially forecast closer to 40 GW, later revising their estimates upward in early 2025.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

I hope that the sunset on boondoggle projects is not further delayed. If an installation can pay it’s own way, great. In too many cases the main reason a project is “green” is all the greenbacks of subsidies involved. I am tired of paying for someone else’s pipe dream.