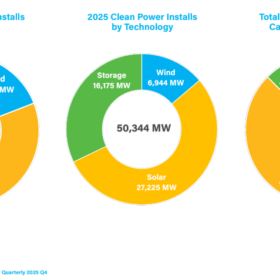

Over 20 GWh of planned energy storage cell capacity for 2028 have been cancelled so far this year, according to the Q2 2025 reports on energy storage supply, technology, policy and pricing from consultancy Clean Energy Associates (CEA).

The cancelled projects include a 9.6 GWh / year factory from KORE Power in Arizona and a 10.2 GWh / year project in Georgia from FREYR. A swath of one-to-five GWh / year projects around the Midwest and the Southeast have also been delayed as policy uncertainty and financing snafus hit small producers hard.

That loss of 21 GWh could strongly negatively impact the industry if the annual demand in 2028 meets its projected 100 GWh target.

Even so, CEA also found that locally integrated systems are becoming a more viable option in the U.S. thanks to growing OEM and domestic integrator capacity. That increased capacity makes it easier for integrators to build local networks and secure spare or replacement parts.

Rather than siting manufacturing in lower-cost countries, the report notes that more integrators are focusing on co-locating their manufacturing capacity with their end market, including a Chinese manufacturer that recently opened a 10 GWh battery manufacturing plant in Texas.

The resulting prices are “fairly reasonable” from a manufacturing cost standpoint. The integrated ESS options do come at a cost premium of 15-20%; but, the report points out, “siting manufacturing in the U.S. is the best choice for minimizing tariff risk, even if costs are higher” due to reduced Chinese content.

Still, regarding cathode and anode materials, CEA notes it will be “possible though difficult” to minimize tariff exposure with a North American supply chain due to tariffs on steel and aluminum, as well as on battery parts.

For manufacturers looking outside the U.S., purchasing cells and systems from South Korea and parts of Southeast Asia could be the best bet to avoiding up to $40/kWh in tariffs. Domestic hardware integrators are thus best positioned to “mix and match” supply sources to attain the lowest costs, per the report’s findings.

While most of the announced manufacturing capacity in Southeast Asia is geared toward EV batteries, CEA pointed out that lithium-ion ESS capacity is likely to follow a similar path to that of offshore solar manufacturing. The consultancy “anticipates many joint ventures, expansions and accelerations of production to be announced over the coming months in the region.”

Though lithium-iron-phosphate (LFP) cell manufacturing outside of China is still in its early days, the report notes there will be more options available by early 2026 in the States, South Korea, Malaysia and Indonesia (though the recent foreign-entities-of-concern rules under the budget bill could complicate the question of least-cost supply).

Stable low lithium prices also play a role, as they bode well for BESS developers in nations not facing significant trade barriers. That said, non-lithium battery technologies and lithium-ion battery recycling could both face a windy road ahead as lithium prices are expected to remain below $10 / kilogram for most of the decade.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.