The United States has conducted antidumping and countervailing duty (AD/CVD) investigations into solar cells and modules imported from China since 2011 and imposed Section 301 tariffs on Chinese products, and Section 201 tariffs globally in 2018.

As a result, Southeast Asian countries have become the world’s second-largest manufacturing hub outside of China as Chinese suppliers moved production lines to the region.

In 2022, the United States initiated anti-circumvention investigations into solar cells and PV modules from Cambodia, Malaysia, Thailand, and Vietnam, although the products under consideration were exempted from tariffs for two years – to June 6, 2024 – mainly thanks to a lack of solar manufacturing in the United States.

The anti-circumvention ruling stipulated products from those nations could avoid tariffs by using non-Chinese wafers and meeting module bill-of-materials (BOM) conditions, benefiting Chinese funded manufacturers with vertically-integrated, non-Chinese supply chains.

The United States tightened trade restrictions in May 2024, with AD/CVD investigations into cells and modules from the four Southeast Asian nations. The investigation covers modules made in those nations with cells of the same origin and modules from other nations which include cells from the four Southeast Asian countries. Modules assembled in Cambodia, Malaysia, Thailand, and Vietnam from cells made elsewhere are not affected.

Preliminary AD/CVD rates are expected from the US Department of Commerce between September and November 2024. With affected manufacturers susceptible to tariff rises during any subsequent reviews of the duties, manufacturers in the countries concerned reduced factory utilization rates, and even began to shutter factories in the second quarter and third quarter of 2024.

U.S. impact

The U.S. solar market faces a supply crunch as a result, despite efforts to onshore PV manufacturing. InfoLink says the United States had 33 GW of annual module production capacity in the first half of 2024 and less than 1 GW of cell lines. New cell manufacturing is unlikely before the fourth quarter of 2024 because of environmental permit requirements, technical personnel visa processing, equipment import times, and policy uncertainty in an election year. Solar manufacturers in countries such as India and Türkiye lack the technical reserves necessary to fill the U.S. supply gap. Solar trade flows from Southeast Asia to the United States will be restricted after the AD/CVD announcement and, with U.S.-based manufacturers still reliant on cells from the four affected countries, AD/CVD-driven price rises will limit demand and slow US solar.

Global expansion

In response to the increasingly tough trade barriers being thrown up by the United States, Chinese-funded manufacturers are actively pursuing global production capacity expansion. The current trend of overseas expansion is divided into three phases.

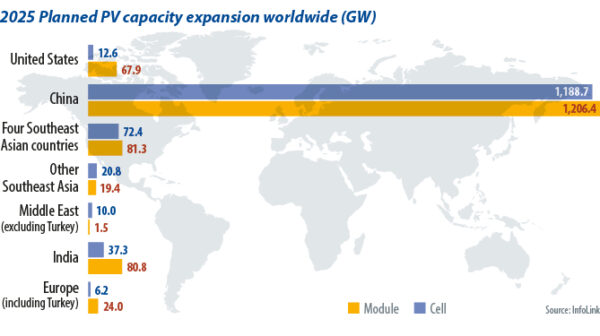

The first regions of interest to Chinese manufacturers are Indonesia and Laos, which are outside the scope of the latest AD/CVD investigations. InfoLink statistics indicate that Indonesia is planning annual cell and module capacities of 9 GW and 14.6 GW by 2025, respectively, with most of those fabs funded by Chinese manufacturers. In Laos, the planned capacities are 9 GW for cells and 3 GW for modules, primarily from Chinese company SolarSpace.

Next are the Middle Eastern countries that have been focusing on the energy transition in recent years. Government investment incentives have successfully attracted PV manufacturers to expand production capacity in the Gulf. Chinese manufacturer Drinda New Energy plans to establish 10 GW of annual cell production capacity in Oman by 2025 and local manufacturers are planning 1.5 GW of module capacity. Although Middle Eastern countries are currently less affected by trade restrictions, in the long term manufacturers must consider the risk that the United States may expand trade restrictions to other regions with concentrated production capacities.

Finally, many Chinese manufacturers have opted to establish production lines in the United States to mitigate the risk associated with trade restrictions. By 2025, annual cell and module production capacities in the United States are expected to reach 13.6 GW and 75.2 GW, respectively, with approximately 30 GW of the module capacity coming from major Chinese manufacturers such as Longi, Jinko, and Trina. Political factors remain a significant variable in PV industry development, however. The 2024 US presidential election will be crucial in determining the policy direction of the Inflation Reduction Act. Whether Chinese manufacturers will face obstacles to subsidy application, or delays in setting up plants due to geopolitical influences, remains to be seen.

Key opportunities

As the United States continues to heighten trade restrictions, planned production capacities are gradually being commissioned in various regional markets. In the future, the PV supply chain may no longer be dominated by China and the four Southeast Asian countries mentioned above. Supply could shift toward a more diversified global layout. Amid a current, sluggish PV industry environment, the ability to interpret policy trends accurately, understand the industrial support measures available in potential overseas expansion countries, build brand value, and enhance technological innovation capability are all critical factors for manufacturers aiming to export to the U.S. market. These are key issues that manufacturers must carefully consider in their global expansion strategies to navigate the opportunities and challenges they may encounter along the way.

About the author: Jonathan Chou is an assistant analyst on the solar research team at InfoLink Consulting. His focus is policy research across the United States, the Asia-Pacific region and Africa. He also monitors projects and helps analysts to compile data on global market movements and demand trends.

About the author: Jonathan Chou is an assistant analyst on the solar research team at InfoLink Consulting. His focus is policy research across the United States, the Asia-Pacific region and Africa. He also monitors projects and helps analysts to compile data on global market movements and demand trends.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.