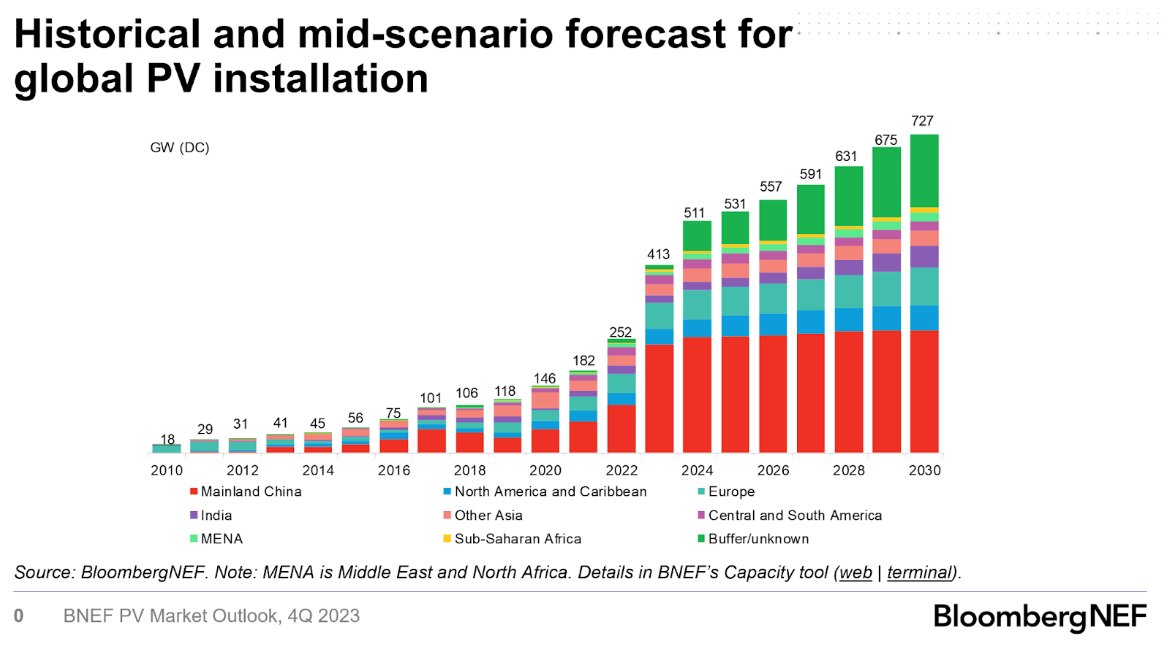

BloombergNEF has released its updated solar market outlook for 2023, projecting that 413 GW of module capacity will be installed this year. This capacity is largely driven by China’s contribution of 240 GW, along with strong growth in many other global regions.

The quarterly update was provided via Bloomberg’s podcast “Switched On” in the episode, Solar supply glut crushes margins but buildout booming.

If the world does install 413 GW of solar, we will have witnessed a growth of over 58% from the 260 GW installed in 2022, which itself marked an almost 42% increase from the 183 GW installed in 2021. During this two year period, the world will have experienced 125% growth – indicating that a doubling of deployed annual capacity occurred in around one and a half years.

This capacity growth is driven by several factors. Foremost is China, which plays a dual role: by being expected to install 240 GW of capacity, and secondly, through its massive scaling of manufacturing capacity, which has driven the price of solar modules toward $0.10/W.

In the ‘Switched On’ podcast, Jenny Chase, a solar analyst at BloombergNEF, shed light on the dichotomy in the solar industry. While solar capacity installation is surging worldwide, she pointed out that the financial side of solar panel manufacturing is still a tough business. According to Chase, even as manufacturing capacity expands significantly, profit margins for manufacturers are under severe pressure, with module assembly lines operating at only a 60% capacity factor.

Clean Energy Associates has projected that there will be 1 TW of new annual solar panel manufacturing capacity, particularly TOPCon solar cells, located in China alone by the end of 2024 – with over 800 GW of capacity in place as of now. This milestone of 1 TW in annual manufacturing capacity follows closely after the global deployment of solar modules surpassed 1 TW in the winter of 2022.

If our deployment pace is maintained, the world will be on track to reach its second terawatt of solar installations by 2024, achieving this in less than three years – a stark contrast to the approximately 40 years it took to reach the first terawatt.

Commenting on the low module pricing, Chase said:

Right now your standard solar module, in a free trade market, costs 12.8¢/watt. That’s below where anyone thought it would be. That’s below where the experience curve says it should be. I’m having real difficulty constructing the experience curve in a way that makes any sense. I am so surprised. I think it’s because I’ve been watching it for seventeen years, eighteen years now, that I am so surprised.

Globally, the low module pricing is facilitating more capacity installations. In 2022, the United States actually saw a slowdown in total volume deployed, partly due to high hardware costs. In China, these low prices have aided in driving wind and solar “megabases”, which boast capacities of up to 20 gigawatts.

Chase mentioned that in the U.S., high trade barriers and interconnection capacity have slowed installation volumes by increasing module pricing and delaying connections. However, the Inflation Reduction Act has provided support and is expected to have a broad market impact.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

Looks like you got your wish. Can you tell us more about these Megabases? It’s a funky name considering they are Giga scale… Megabase would a great name for a metal band.