We have all been asking ourselves for some time now: How far can photovoltaic module prices go down before the bottom is finally reached? Apparently, there is still room for further drops, as all prices have fallen again this month.

On average, prices in all module categories have been corrected downwards by around 10%. Never before in the history of photovoltaics have panel prices plummeted so significantly in such a short space of time. For a month or two now, the values have been below the previous all-time low of 2020 and even more so below the production costs of most manufacturers. Generating profit margins seems to be a thing of the past for the time being and for many of them it is now just a matter of minimizing damage or even survival.

How could we come to this, and what are the causes of this self-destructive trend?

First of all, it must be noted that module prices rose by more than 50% between October 2020 and October 2022, which is not due to technological developments, but primarily due to the pandemic-related supply shortage coupled with a simultaneous increase in demand. Ultimately, many players in the photovoltaic market made very good money – at the expense of the end consumers. Until recently, photovoltaic system prices were higher than they had been for a long time. Now things have completely changed, which inevitably leads to a drop in prices. The speed and intensity of this change, however, surprise even experienced market participants.

After the shortage issues of the past two years, many installers and wholesalers made generous forecasts and ordered new goods as if there was no tomorrow. The producers, predominantly from Asia, reacted and increased their capacities. Global production capacity usually exceeds the actual expected demand by 30% to 50%, so that fluctuations can be quickly compensated for. The production lines are then ramped up or down as needed. Recently, however, this mechanism has gotten a bit out of hand as many manufacturers have had to switch their cell and module production very quickly from p-type PERC technology to n-type TOPCon, due to patent rights problems in individual regions. However, since the sales restrictions did not apply worldwide, new capacities were built up for TOPCon without replacing the old capacities and without consistently shutting them down.

The prospects appeared to be good in the long term thanks to the supposedly permanently high costs of conventional energy sources. Unfortunately, European politicians were very good at replacing old fossil fuel sources with new ones at short notice, so the suffering from skyrocketing energy costs quickly fell. The pandemic also seems to have finally been overcome and the average European can travel without restrictions again. Not least due to high inflation, many people who recently wanted to invest in photovoltaic systems are now becoming more reluctant. The fact that interest rates on loans continue to rise doesn’t make the decision any easier. The consequence of all the factors listed is a collapse in demand so that the photovoltaics industry has not yet emerged from the summer slump even in mid-September.

The quickly dwindling interest in solar power generation inevitably means that the order books of installers and project planners run empty and pre-ordered modules and inverters cannot be delivered on time. The goods are increasingly piling up at wholesalers and in the manufacturers’ warehouses. There are now said to be 40 GW to 100 GW of unsold modules in European stores, primarily in the Rotterdam area. Determining an exact amount is almost impossible. However, it is enough to know that there is already about a year’s supply of modules in Europe to understand the dimensions and scope of the matter. Storing these goods costs a lot of space and therefore money; losses are increasing day by day, while sales opportunities are decreasing. The pressure increases until the avalanche finally starts to slide and the first ones will begin offering their modules below purchasing or production costs. Competitors are forced to follow suit and the downward spiral is set in motion.

Now one might think that falling prices would have to increase demand. In many cases, the current price level for materials has not yet reached end customers or investors. For many providers, the old inventory, which was purchased at higher prices, is still too large. The wave of devaluation is also just beginning, which is why the price drop is becoming more severe from month to month. Many still hope to get away with a black eye. But the risk of being stuck with the old goods is very high. Those interested in photovoltaics also monitor prices very closely and compare offers. Accordingly, many end customers are now waiting for the offered prices to fall further and are hesitating to place an order.

So everything now depends on where the journey takes you. How low do prices have to fall before demand increases again and a balance is achieved?

The production lines in China are already being shut down, and up to 50 GW are to be built in the country this year – in addition to the 80 GW to 90 GW already installed this year. But even if not a single new module came to Europe from China, we would need many months until the module backlog is cleared. The stored modules are also predominantly products with PERC cells, whose efficiencies are lower than those of modules with the latest technology. I doubt that these are suitable for increasing domestic demand strongly. These products are more likely to be used in markets outside of Europe, where people are happy about inexpensive solar modules. In my opinion, only when the existing glut of modules can be reduced will a healthy price level be able to be established in the market again. By then, however, a market shakeout will probably be seen in and some market participants will fall by the wayside.

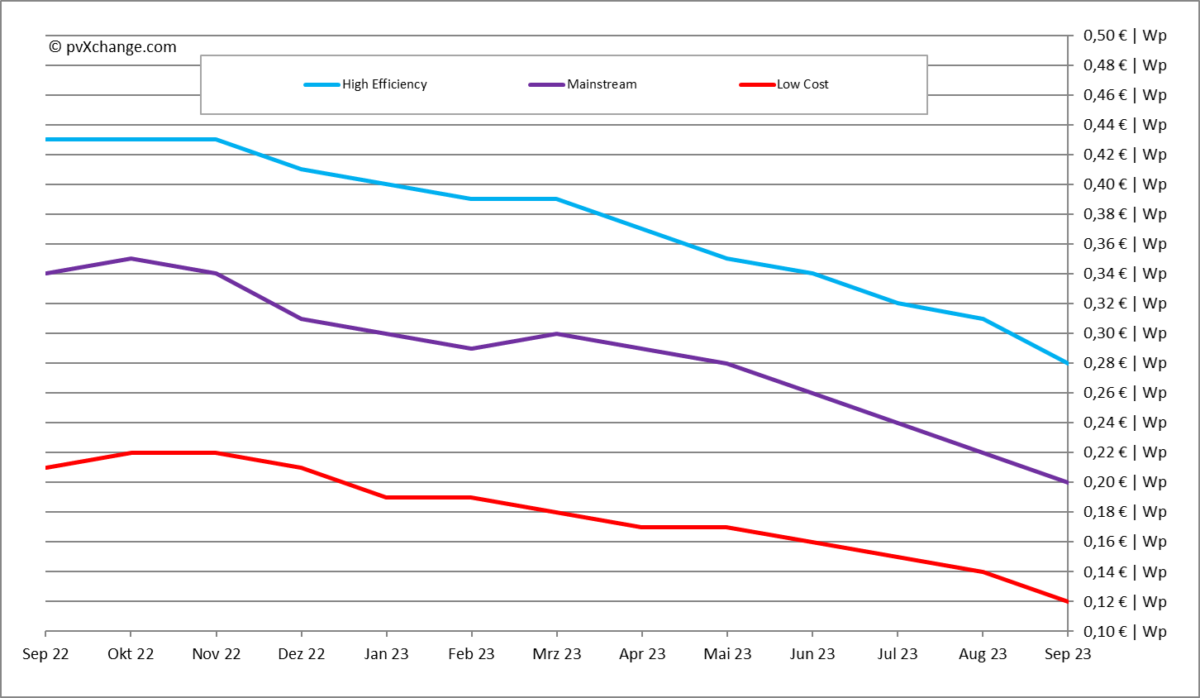

Overview of the price points differentiated by technology in September 2023 including the changes compared to the previous month (as of Sept. 18, 2023):

About the author: Martin Schachinger studied electrical engineering and has been active in renewables for more than 20 years. In 2004, he set up pvXchange.com. The online platform allows wholesalers, installers, and service companies to purchase a range of components, including out-of-production PV modules and inverters.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

“How far can photovoltaic module prices go down before the bottom is finally reached? ”

Well, look at computer memory prices.

In 1970, a GByte of memory cost $1 billion USD in 1970 dollars.

Today, a GB costs $2 in 2023 dollars.