The move to increase adoption of zero-emission vehicles requires an accelerated build-out of electric-vehicle (EV) charging stations. Wood Mackenzie corroborates, noting in its report, Commercial landscape of EV charging networks in North America, that the market for public charging networks in North America is forecast to grow rapidly by 2050.

President Biden set a goal of building out a national network of 500,000 EV chargers, which got a boost with the announced funding to accelerate the creation of zero-emission vehicle (ZEV) corridors that expand the nation’s EV charging infrastructure.

Pointing to the necessity of these chargers as EV adoption grows, Nick Esch, research analyst for Grid Edge at Wood Mackenzie, noted that public EV charging networks are crucial. “We are seeing collaboration and integrations among EV charging networks both old and new, as well as significant local and federal policy support, and investment across the public charging market,” said Esch.

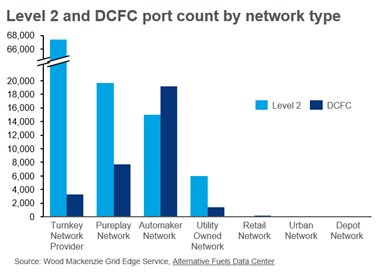

There are currently 73 active EV public charging networks in the United States and Canada made up of different network types. As demand is growing, many more entrants are expected to join the market, according to Wood Mackenzie’s findings.

“Gas stations, quick service restaurants, and convenience stores with existing locations are in the early stages of deploying public charging infrastructure as they look to capitalize on their existing retail footprint, as well as EV adoption,” said Amaiya Khardenavis, analyst with EV Charging Infrastructure at Wood Mackenzie.

The Subway quick service restaurant chain is one example, having recently announced a partnership with GenZ EV Solutions, an EV charging development company, to pilot Subway EV Charging Oasis parks at new and existing restaurants.

“The growth strategy of charging networks is focused on building their footprint in high-traffic locations, setting up roaming agreements with other networks, and installing high-power charging infrastructure to future-proof their sites,” said Khardenavis.

DC fast chargers

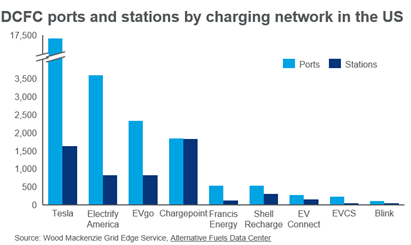

DC fast chargers (DCFC) are EV chargers that can achieve a charge rate between 50 kW and 350 kW. The report finds that Tesla is the DCFC leader with its ‘Supercharger’ network. It has 17, 408 total DCFC ports and ports per station ratio of 10.5, making it the largest fast-charging network in North America. The next three largest include ChargePoint, EVgo and Electrify America, which have fast charging networks near population centers or highway corridors across the U.S.

“A few networks with established footprints dominate the fast-charging landscape in the U.S. and Canada, such as Tesla. They are followed by emerging networks that are established in regional markets with intentions to grow their reach to new markets,” Esch added.

Level 2 chargers

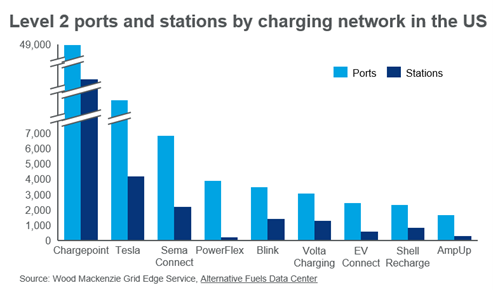

Level 2 EV chargers have a charge rate between 3 kW and 19 kW of AC power, and ChargePoint leads this category with over 48,000 charging ports in nearly every major metropolitan area across the United States. The Tesla Destination is the second largest Level 2 network with more than 12,500 ports. SemaConnect is the third, which was acquired by Blink in Q2 2022, and now has a combined network of over 10,000 ports. PowerFlex is the fourth largest, but is primarily in California.

Utilities and automakers are showing signs of understanding the needs of this burgeoning market. There currently are 19 utility-owned EV charging networks operating in North America, according to the report, and these are led by Canadian utilities, which account for 69% of DCFC ports and 55% of level 2 ports.

“While US utilities have initiated investments in public charging, their scope is restricted in size and locations where chargers can be installed is limited by regulators. Canadian utilities have launched province-wide networks that outsize their private competitors,” Khardenavis added.

Automakers understand that in order to sell the electric vehicles that they’re manufacturing at an increasing pace, charging networks are required. Several have announced partnerships with charging infrastructure developers or through direct investments in the deployment of chargers. One example is General Motors’ partnership with EVgo through which they plan to install 3,250 DCFCs in cities and suburbs. The company also announced plans to deploy 2,000 EVgo charging ports along Pilot and Flying J travel centers.

In collaboration with ChargePoint and MN8 Energy, Mercedes has committed to installing over 2,500 charging ports at over 400 locations in North America.

“Since the public EV charging space is highly fractionalized, EV automakers are aiming to own the customer relationship after the point of sale and play a larger role in public EV charging. Many are taking on the e-mobility service provider role, facilitating payments and navigation to chargers while also curating charging networks for their customers through integrations with public charging networks,” Khardenavis said.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.