Like many aspects of the IRA, the Inflation Reduction Act’s (IRA) “Energy Community” clause – and its 10% incentive adder – is still under review, with the U.S. Department of Treasury to offer guidance to the market.

The Department released partial Prevailing Wage & Apprenticeship guidance last week.

pv magazine USA covered various groups defining which geographic regions are expected to benefit from the Energy Community’ clause. All groups noted that these maps are still developing, and that interpretations are evolving.

One of the groups, Charles River Associates, recently updated its maps and submitted them to the U.S. Senate with commentary on the changes that were made. They also presented some of the items they are seeking further clarification on.

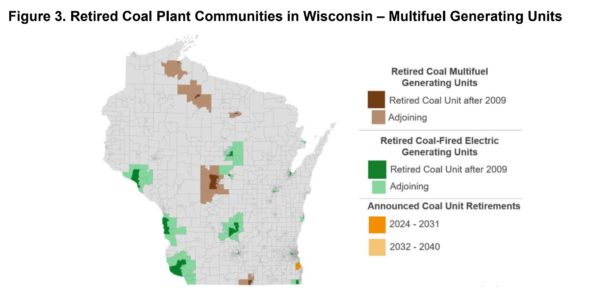

Charles River has requested clarification on two questions: whether a coal plant that was converted to gas would qualify, and whether a retiring power plant that is powered by multiple fuel sources – including coal – would qualify. The group suggested that if the latter were considered eligible, then roughly 5% of Wisconsin’s land area would be eligible.

Charles River also noted that the currently available datasets must be refined before they can be fully put to use. They found that the data recording the latitude and longitude of sites in the Mine Safety and Health Administration’s database was frequently incorrect. Some mines had been improperly attributed to areas where mining hadn’t occurred for decades, and some active mines were marked as abandoned, or closed.

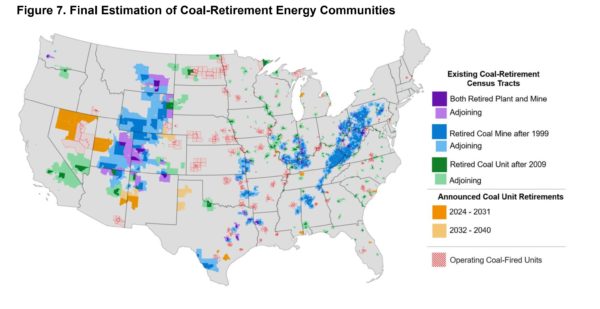

This led Charles River to check the sites manually, resulting in the removal of 15% of the potentially qualifying facilities from its database. In its August update, the group suggested that 18% of the nation might qualify as a coal energy community. In their latest update, that number was scaled back to 16%.

So far, there have been no indications as to how solar asset owners will verify to the IRS that their facility is located in a coal energy community. Since these taxes will be filed in the 2024 calendar year, the wait for these procedures to be introduced may continue.

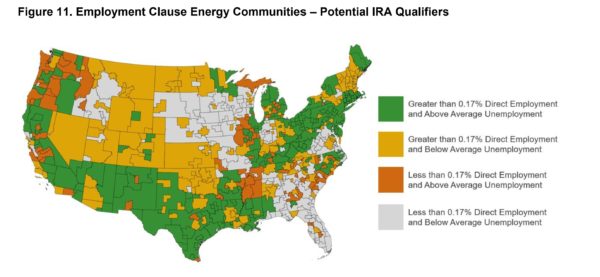

A second path to getting the 10% Energy Community adder is through fossil industry employment. The IRA notes any region that “has (or at any time during the period beginning after December 31, 2009, had)”:

- “0.17 percent or greater direct employment or 25 percent or greater local tax revenues related to the extraction, processing, transport, or storage of coal, oil, or natural gas,” and

- “has an unemployment rate at or above the national average unemployment rate for the previous year.”

Charles River says that this clause of the Energy Community section will be the most challenging to manage. They note that maps will need to be agreed upon, and that there are many granular, localized calculations to make regarding unemployment, fossil employment, and tax revenue.

The group notes that the challenges to data calculation are compounded by the fact that the maps and data must be updated annually. However, Charles River finds that using their current data and calculations, 34% of the nation could be eligible for the 10% adder due to the fossil employment clause, (shown in green in the map above).

Brownfields also have a 10% adder opportunity, however, similar challenges can be found within its dataset as well. Charles River says that brownfield data will become available in limited quantities and will vary heavily from state to state in terms of collecting, defining, and reporting. Furthermore, the definitions of a brownfield in the IRA don’t exactly line up with the definitions in existing datasets.

The group suggests that a unique database will have to be created.

Charles River is closely monitoring the Treasury’s clarification and implementation of the rules surrounding Energy Communities. They estimate that 10% to 20% of the hundreds of gigawatts of solar installed under the IRA could be affected.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.