A downward trend in polysilicon prices is expected this year, and inventory levels across the entire solar value chain are expected to begin building through the first half of 2022, said Corrine Lin, chief analyst and Dora Zhao, senior analyst, PV Infolink in a recent webinar held by Philip Shen managing director, ROTH Capital Partners. Click here to register and view the recorded webinar session.

PV Infolink’s analysis shows that polysilicon ex-VAT (pre-tax) prices should improve from the current levels of $26-$30/kg to as low as $19/kg by the end of the year. Prices have recently ticked back up to about $30/kg, largely due to decreased polysilicon inventories driven by seasonality ahead of Chinese New Year and a rebound in utilization levels from the end of 2021, said Dora Zhao.

Inventory levels are expected to build across the value chain, said the report. Currently, value chain inventory levels are well below healthy levels, sitting at about a month to a six weeks across all segments, said PV InfoLink. Polysilicon inventory is about two weeks, and wafers hold a less than one week inventory. The report projects an increase in production to 318 GW of polysilicon and 322 GW of wafers globally in 2022. It said that an inventory build of about 30 GW above forecast production for modules may result in pricing support for polysilicon and wafers through 2022.

Capacity expansions are on the way across the value chain, drive by “just-in-case” inventory considerations due to ongoing Covid logistics. Lin and Zhao noted many new entrants are expected to continue through 2023, including Shangji Automation, Gaojing Solar, Shuangliang Group, and Fuxing New Energy (n-type wafers.)

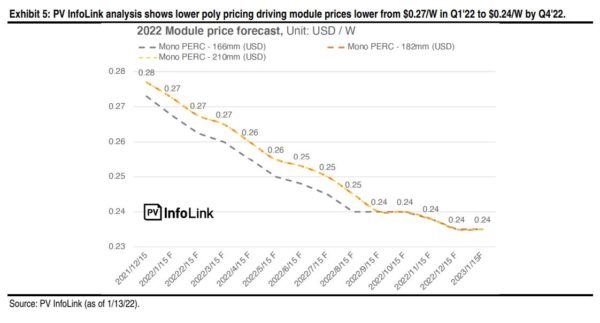

Lowered polysilicon pricing will send a ripple effect through the supply chain, and PV InfoLink projected module prices will drop from $0.27/W in Q1 to $.24/W by Q4.

N-type modules are expected to increase to about 7-8% market share this year, while PERC modules will likely retain their dominance with about 90% market share. Corrine Lin said there has been a rise in companies taking interest in TOPCon expansion over heterojunction. She commented that perovskite technology likely needs five or more years to take a meaningful share of the market.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.