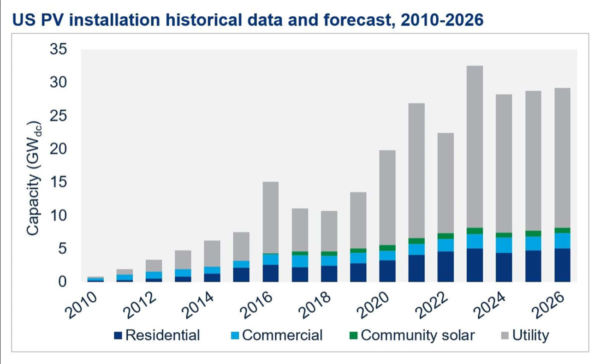

WoodMac Renewables & Power lowered their projections by 25% for solar power capacity to be installed in the United States in 2022, according to the US Solar Market Insight report released by the Solar Energy Industries Association (SEIA) and Wood Mackenzie. They’ve also added a big 44 GW asterisk next to all projections going forward — a projection increase dependent on the passage of the Build Back Better/Reconciliation Bill.

From the hand that takes, WoodMac cited supply chain constraints and logistics challenges as they lowered their quarterly estimates for deployed solar power capacity estimates in the United States. The 25% reduction – of 7.4 GW implies that prior projections were 29.4 GW, and that revised projections are now 22.2 GW of deployed capacity.

This US Solar Market Insight report adds to a bevy of projections suggesting that market projections are getting complicated going forward.

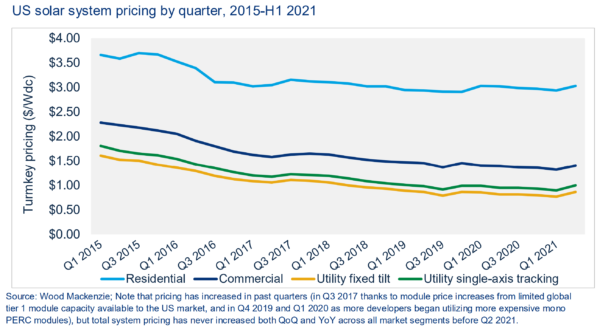

Michelle Davis, the report’s author at WoodMac, says costs have increased across all market segments for the second quarter in a row — and that these increases have undone two years worth of hardware price decreases. Other than the price hikes that hit the residential market in 2015, this year’s supply chain price increases were the highest they’ve been since WoodMac started tracking the data in 2014.

Additionally, solar panel availability and pricing has been affected by anonymous petitioners who sought to add additional tariffs to solar panel imports. Their petitions have since been rejected.

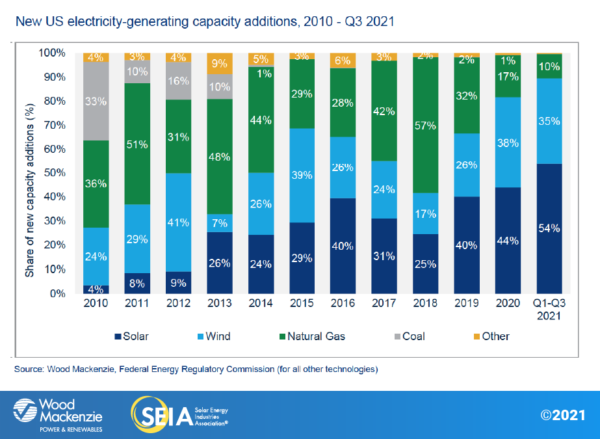

WoodMac suggests that these challenges, in addition to interconnection woes, is at least partially responsible for the commercial and community solar sectors slowing by 10% and 21%, respectively, quarter over quarter.

Amidst these price increases and market complexities, utility scale capacity has continued to set quarterly deployment records, as the sector is likely to be insulated from hardware costs by its long term supply chain choices. However, one might assume the utilities are taking a harder hit on shipping price increases – and delays – due to their large product volumes.

WoodMac also sees that residential installation volume has kept up growth. This may be due to the sector’s higher priced projects and premium product selection, which are better able to absorb subcomponent price increases.

In the end, the growth of two out of three sectors helped solar power to continue increasing its market share of new generation capacity as the USA seeks to extend a nearly two-decade march toward a cleaner grid.

Along with this downward projection, the group suggests that the solar market might increase by 43.5 GW of deployed capacity between 2022 and 2026, if the Build Back Better/Reconciliation Bill is signed with the current solar tax benefits in place.

WoodMac projects that 14 states will see at least a 1 GW of solar capacity increase due to the legislation, with another 14 states adding 500 MW of capacity. Texas alone could add 7 GW of capacity.

The most recent headline on the bill is that the US Senate has released their draft version of the document. The changes in the Senate version versus the House’s version include adding tracking manufacturers to incentivized hardware manufacturers list, as well, pulling the “Direct Pay” version of the 30% tax credit forward to projects installed in 2022 for residential customers — matching business projects.

The 10 year, 30% Tax Credit extension along with the “Production Tax Credit” for large scale projects are expected to greatly increase capacity.

Some projections even suggest that capacity in 2022 might slow a bit because the pressure to complete projects before 2023, when the prior tax credit would have expired, is no longer there.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

How about you put thermoelectric generator on them for the heat

Rrr