Once a niche and expensive tech, a new report by the U.S. Energy Information Administration (EIA): Battery Storage in the United States: An Update on Market Trends, analyzes how large-scale battery storage capacity increased exponentially in the latter half of the 2010’s and what drove this rapid adjustment.

In 2010, the United States was home to just seven large-scale battery storage systems, which accounted for a total of 59 MW of power capacity. By 2015, the amount of projects squared to 49 systems, now accounting for 351 MW of power capacity. It was at this point that adoption really shifted into high gear, as just three years later, at the end of 2018, the total number of operational battery storage systems increased by more than 150% to 125, as did power capacity, clocking in at a total of 869 MW installed. In less than a decade, the amount of installed battery capacity increased more than tenfold.

So how did this happen?

The exponential gains in batter capacity came first and foremost in the country’s regulated markets, as independent system operators (ISOs) an regional transmission organizations (RTOs) accounted for 73% of large‐scale battery storage power capacity in the Unites States and 70% of energy capacity.

Of course, these additions, for the longest time, came from PJM Interconnection and California Independent System Operator (CAISO) territories, which hold the majority of the country’s power capacity and energy capacity. PJM Interconnection is home to the most power capacity, at 282 MW, while CAISO follows closely behind at 180 MW.

Notably, Alaska and Hawaii, states with electrical systems that account for 1% of the country’s total grid capacity, accounted for 12% of all battery power capacity in 2018 (107 MW) and 14% of battery energy capacity.

In 2018, the battery storage market saw a shift from the norm, as over 58% (130 MW) of power capacity additions, representing 69% (337 MWh) of energy capacity additions, were installed in states outside of PJM Interconnection and CAISO territories. One of the areas leading this diversification of capacity additions is Texas, which is the largest single market after PJM Interconnection and CAISO (94 MW). The Texas market is only expected to grow further, with the Electric Reliability Council of Texas’ battery interconnection queue sitting at 7,214 MW, as of the end of 2019.

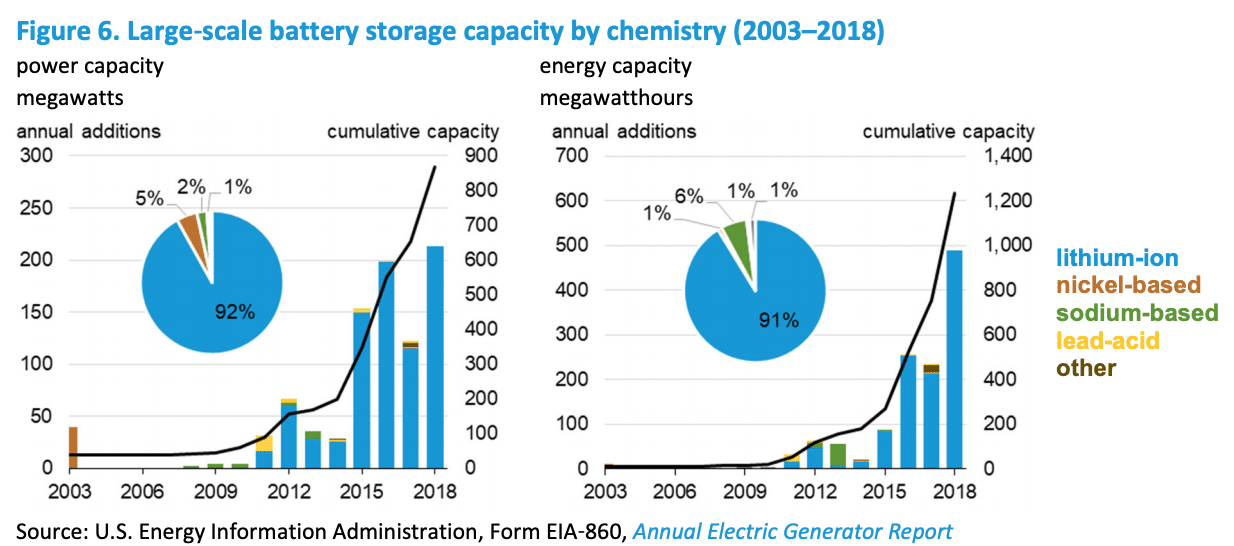

Lithium-ion runs the game

As of 2018, over 90% of large‐scale battery storage power capacity in the United States was provided by batteries based on lithium‐ion chemistries. Outside of lithium-ion, Sodium‐based battery storage technologies accounted for 2% of the installed large‐scale power capacity and 6% of the installed large‐scale energy capacity in the United States at the end of 2018. Lead acid and flow batteries both represent around 1% of the installed power and energy capacity of large‐scale battery storage in the country, while the most niche of all the commercial tech, nickel‐based batteries, represent even less capacity.

While flow batteries started to catch on in the later half of the decade, with three projects completed between 2016 and 2017, this has done little to alleviate lithium-ions’ stranglehold on the market. It is a hold that’s only tightening, as many legacy lead acid and nickel battery systems are being retrofitted and replaced with lithium-ion batteries. In 2016, Duke Energy replaced 36 MW of lead‐acid batteries at the company’s Notrees wind power facility with lithium-ion systems.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.