The California Solar & Storage Association (CALSSA) has collected and shared data on California’s behind the meter solar+storage activity in the first half of 2019, with data that goes back to the beginning of 2016.

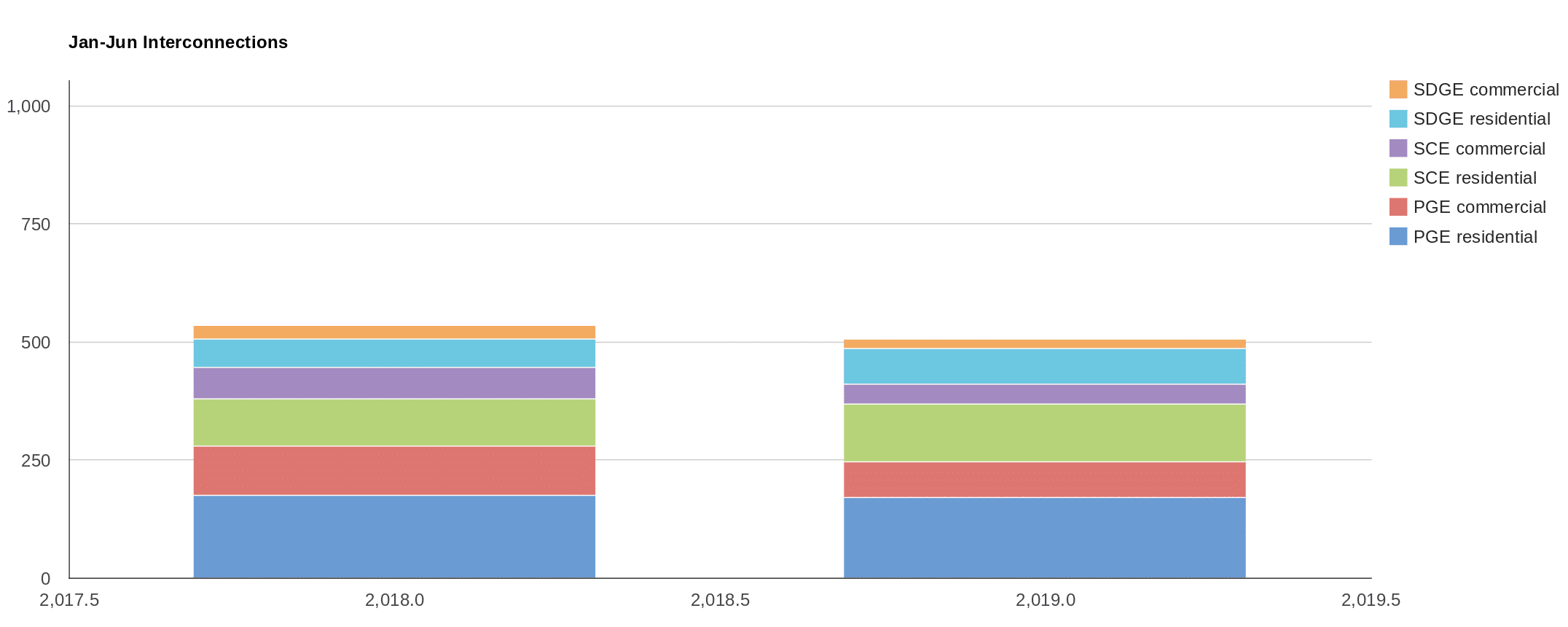

The data suggests that within the three main investor owned utilities – San Diego Gas & Electric, Southern California Edison and Pacific Gas & Electric – commercial interconnections are running slightly behind the 2018 numbers (below image) in terms of projects interconnected. However, residential systems seem to be picking up a bit.

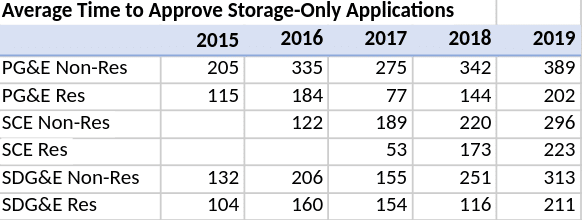

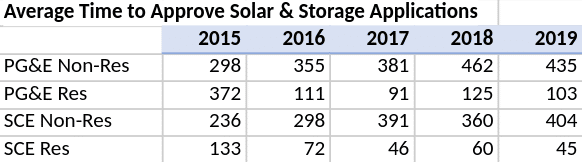

One chart that gives a bit of indigestion is the time for approval for stand alone and solar+storage installations – if only because of the high variance, but also because quite a few larger projects take more than a year to get approved. The projects are divided into residential, commercial, education and industrial with time frames ranging roughly from 30 to 60 days for residential, to two years for industrial systems.

Adding solar power to a storage installation seems to speed up the amount of time for a residential installation, however, it slows a commercial installation.

In Pacific Gas & Electric territory 20% of residential energy storage systems are stand alone, while in the other territories solar is coupled with storage 99-100% of time. Commercial installations had an inverse relationship though – with only 40% of storage projects coupled with solar power, suggesting the market is being driven by other factors like demand charges.

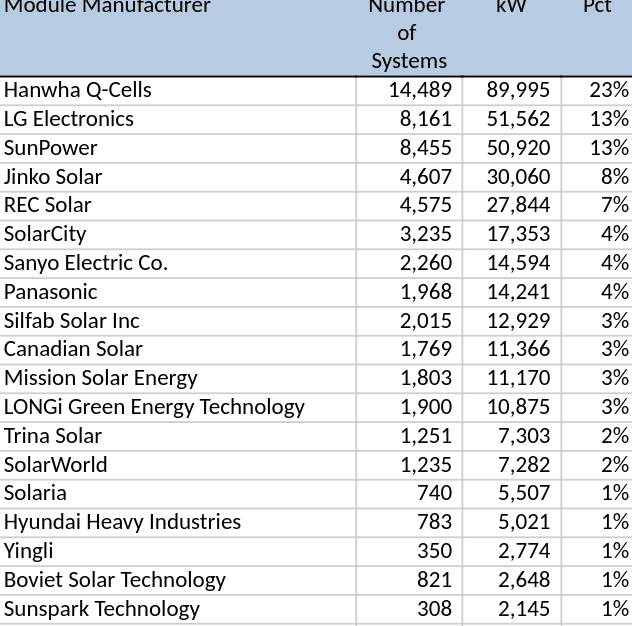

While not broken out on an annual basis, so tougher to see recent trends, we did get insight into the top manufacturers of modules and inverters. Hanwha really has a market hold on residential modules (below chart) at 23% of product deployed, with LG & Sunpower bringing the top three to 49% of market share. The report does note 107 unique solar module brand names since 2016.

Commercial modules have SunPower on top though at 14% of all systems, with LG and Canadian Solar at 10%.

Inverters are a much tighter marketplace – with 56% of residential being SolarEdge product, followed by 20% Enphase and 12% SunPower (some of which are Enphase). The commercial market is 13% SMA, 16% Yaskawa-Solectria and 14% SolarEdge.

Installation companies are to be found aplenty – with the long tail of residential installation companies at just shirt of 1,700, and over 450 commercial installation companies noted. In the residential space, Vivint has installed over 8,000 systems totalling 50 MW and 13% of total capacity. Quickly this falls off to Tesla (SunRun mostly) at 6% of systems, SunRun at 5%, and SunPower at 3% – then a massive number of companies at 2% and less showing that customers who own pick from a variety of sources.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.