Vivint Solar faces the same fundamental problem that other large third-party solar companies like Sunrun are dealing with: that while it is able to grow, containing costs are another matter.

By many metrics, Vivint had an outstanding second quarter. The 56 MW that it installed is its largest volume since the third quarter of 2016, and the company’s $91 million in revenue is not only 12% growth year-over-year, but a new quarterly record.

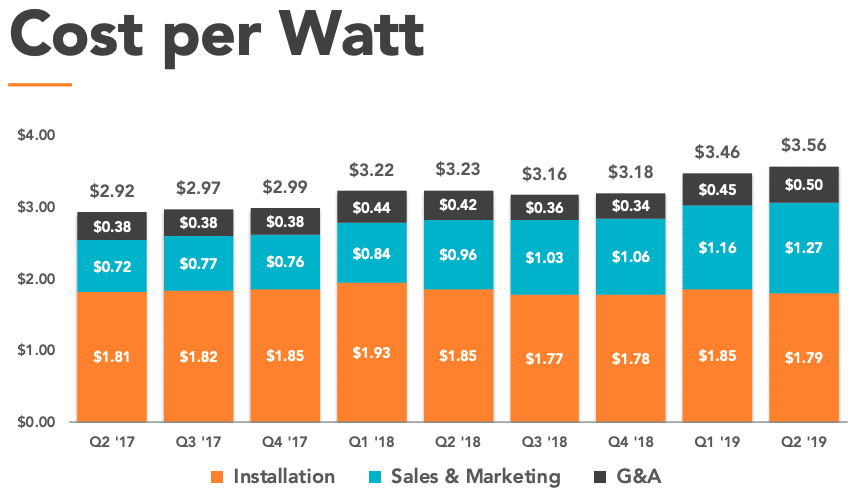

However, Vivint also reported a $37 million loss from operations, which appears to be largely the result of ballooning sales and general and administrative (G&A) costs. These are even more apparent when looked at on a cost-per watt basis.

Vivint’s sales and marketing costs jumped a third from a year ago to a whopping $1.27 per watt – more than the total system cost of a utility-scale solar plant. G&A also rose to $0.50 per watt – its highest level in at least two years, despite the economies of scale that should be gained by Vivint’s high level of installations.

During the quarterly results call, CEO David Bywater blamed these largely on a tight labor market and the high cost of attracting talent, describing “intense” competition for direct sales teams.

There is also the question of whether or not Vivint is making, or losing money. On a quarter-to-quarter basis Vivint reports losses like every other third-party solar company, but it retains long-term value. However, the company only grew its gross retained value by $68 million during the quarter and this was exceeded by its $88 million net loss.

Avenues to bring down costs

This is not to say that all is hopeless. Vivint is actively pursuing other ways to reduce its sales costs, including the sale of solar through big-box retailers. This includes a recent deal with Sam’s Club, which follows on a similar arrangement with Home Depot earlier this year.

CEO Bywater notes that the company is “still early in the ramping of these channels”, but in terms of reducing costs California’s mandate to require solar on all new homes is even more promising; as revealed in a pv magazine analysis this has the potential to eviscerate soft costs.

Like its competitors Sunrun and SunPower, Vivint is positioning itself in advance of the mandate. Bywater says that the company is working with eight of the top 10 homebuilders in California, and nine months ago the company unveiled a new fixed-rate lease product specifically for the new home market.

And like its third-party competitors, Vivint is getting more sophisticated with its financing. Just two days before its results, the company closed on a new $325 million warehouse facility which it says will decrease the cost of its debt by 87.5 basis points while “materially increasing” up-front cash to deploy more solar, which is merely the latest in the company’s financing successes.

It is not clear if the worst is over for the company or not. Vivint expects further growth in the third quarter, and to install 62-65 MW at a cost of only $3.36-$3.44 per watt, but it remains to be seen if this will be merely a quarterly deviation from a path of increasing costs, or if the company really has turned the corner.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

Interesting chart of installation costs per watt. I ran across this same thing when Solar City held the solar PV installation king title a few years ago. I got their installation quote and one from a local solar PV installer, it was 10K less than Solar City. I liked the panels better, the inverters and the warranty of the units better than the Solar City offer. Soon after, Solar City pulled out of the area.

On my first solar home, one day a Vivint salesman knocked on the door and asked if I had heard about the “investment opportunity” of a residential solar PV system. I walked him back to the edge of the property and showed him the solar PV panels that I had installed at least five years earlier. That was the shortest sales pitch I have ever had.

The proposition is one could find installation kits from wholesale solar or blue pacific solar and find a local installer to do the job for you at around $2.75 a watt installed. Like Solar City, Vivint may or may not be there when the system needs repair. I have worked with the manufacturers directly and the troubleshooting, RMA and exchange under warranty process I found very easy.