As a company, SunPower is a study in paradox. It makes the world’s most efficient solar panels that are commercially available for rooftop application, has one of the largest presences in the residential solar sector, and is breaking ground in both grid services and interfaces for its customers.

Profitability is another matter. Sunpower reported a 15% operating margin and $121 million in net income against $436 million in revenue during Q2, but this was the result of $137 million gained from leases that it sold, and SunPower expects to again report a loss during the third quarter.

This is in contrast to promises of “sustainable profitability” in the second half of 2019, goalposts which keep moving as the promise of getting into the black remains elusive. However, what is happening is that SunPower’s losses are continually getting smaller. Even when the gain on divesture is removed SunPower’s margins have consistently improved in recent quarters.

Cash was not as pretty. The $200 million in cash and equivalents that SunPower had online at the end of the quarter was a big drop from the $364 at the beginning of the year. However, this level is far from an emergency, and SunPower expects its businesses units to bring in more cash during the second half of the year. Furthermore, during the quarter the company partnered with Bank of America and Hannon Armstrong on a residential lease financing structure.

Distributed power

SunPower saw a number of positive developments during Q2, and leading the list was the beginning of shipments of its A-Series module into the U.S. market. The module is a powerhouse, clocking in at 415 watts as the first module for the rooftop market to exceed 400 watts.

This is the result of bigger, better everything – bigger wafers and a larger module format, but also 25% efficient cells, setting a new high even for SunPower’s back-contact technology.

This is the result of bigger, better everything – bigger wafers and a larger module format, but also 25% efficient cells, setting a new high even for SunPower’s back-contact technology.

The rollout of A-Series coincided with SunPower’s largest deployment of modules to date at 622 MW, a growth of more than 30% which was supported by new A- and P-Series module lines. SunPower credits the North American residential business with its growth during the quarter, and the 70 MW deployed into the U.S. residential market puts SunPower not far behind Sunrun as the 2nd-largest company in the space.

During the quarter SunPower also deployed 47 MW of solar in the commercial and industrial market, as well as 15 MW of energy storage, and during Q3 expects to roll out a combined solar and battery solution for residential customers through its Equinox solution.

Overall, the scope of services offered by SunPower Energy Services (SPES) division continues to grow. The company has 75,000 customers under residential leases, but is also providing O&M services to 1.3 GW of commercial and residential PV systems.

Furthermore, its EnergyLink monitoring platform has more than 100,000 users, and SunPower has unveiled a new AI-powered design tool for customers that could streamline the design and sales processes. These value-added solutions have the potential to increase what CEO Tom Werner describes as “customer stickiness”.

SunPower’s customers are not only homeowners and businesses with rooftop PV systems. During 2018 the company successfully bid into the ISO New England capacity market, and says that it plans to further expand this activity, as well as providing demand response in California.

Global reach

While it expands its distributed energy services offerings, SunPower is also retooling and expanding its manufacturing. The company is currently installing tools on the second 125 MW line for its A-Series product, and reports that it has fully ramped its P-Series production at the former SolarWorld factory in Oregon.

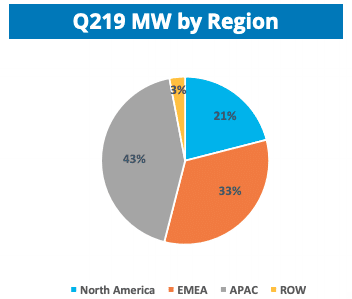

SunPower has a lot more P-Series product through its 2 GW joint venture in China, and the quarter showed that the majority of the company’s deployments are now in the Asia-Pacific region. Due to this strong demand for multiple products across several regions, SunPower reports that it remains fully booked through the end of the year.

SunPower has a lot more P-Series product through its 2 GW joint venture in China, and the quarter showed that the majority of the company’s deployments are now in the Asia-Pacific region. Due to this strong demand for multiple products across several regions, SunPower reports that it remains fully booked through the end of the year.

The next two quarters will see more A-Series coming online, in preparation for a full switch over of SunPower’s back-contact production. And while the company expects ongoing growth in the second half of the year, it is still enduring the costs of legacy polysilicon contracts. Even with $1.8-$2 billion in revenue for this year, CEO Werner expects that the elusive positive operating margins and profit will come in the second half of 2020.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

In another year, their supply contracts will drastically be reduced. Reducing their cost of goods. Margins should also improve dramatically.