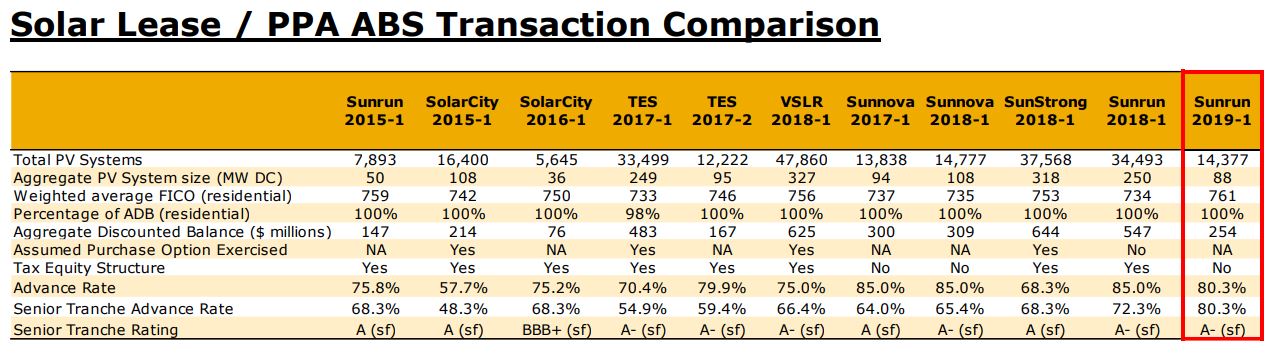

Securitizations of residential solar power leases, power purchase agreements and loans allow the originators and builders of solar arrays – like Sunrun, Vivint, Sunnova, SunPower, Dividend and others – to sell all of the long-term revenue in exchange for more cash to build more solar. Via securitizations, Sunrun now has $1.67 billion in outstanding receivables.

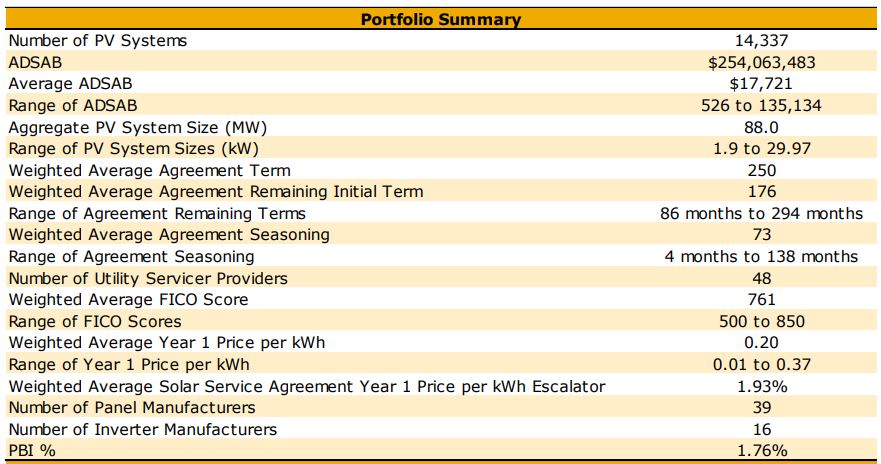

The Kroll Bond Rating Agency (KBRA) has assigned a preliminary rating of “A-” to Sunrun’s most recent bond offering, the $204 million Xanadu Issuer 2019-1 (pdf). The total “aggregate discounted solar asset balance” is approximately $254 million, and it consists of 46% balanced PPAs, 26% lease agreements, and 28% generation PPAs. The weighted average remaining term of the agreements is 176 months, and the weighted average FICO of customers is 761. There are 14,377 individual contracts for solar arrays that total 88 MWdc.

As positives for the portfolio, KBRA noted that Sunrun is an experienced originator/aggregator and servicer (below image), and has been in the space since 2007. Also noted as positives were the credit scores of customers, the inverter replacement account, a $4.8 million liquidity reserve account, portfolio over-collateralization, as well some of the technical structures of the portfolio.

Among the factors listed as portfolio negatives is the general youth of the industry. As the solar industry has weathered no major economic downturns, there is no predictive ability on how consumers will react. KBRA also noted the high geographic concentration – 67% – in California, and 81% in three states (CA, MA, NJ), the longer than standard repossession time frame for defaulted systems, as well the changing net metering policies of the 2.5% of the portfolio based in Guam.

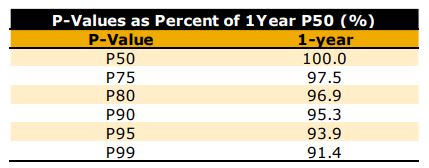

The document noted that system performance relative to expectations after the first year was very strong, with P50 values at 100%, and even P99 ratings greater than 90% of the overall portfolio. KBRA also noted that they used a 1.267% degradation value, which if industry norms closer to 0.5% hold out, mean this portfolio has an over perform opportunity.

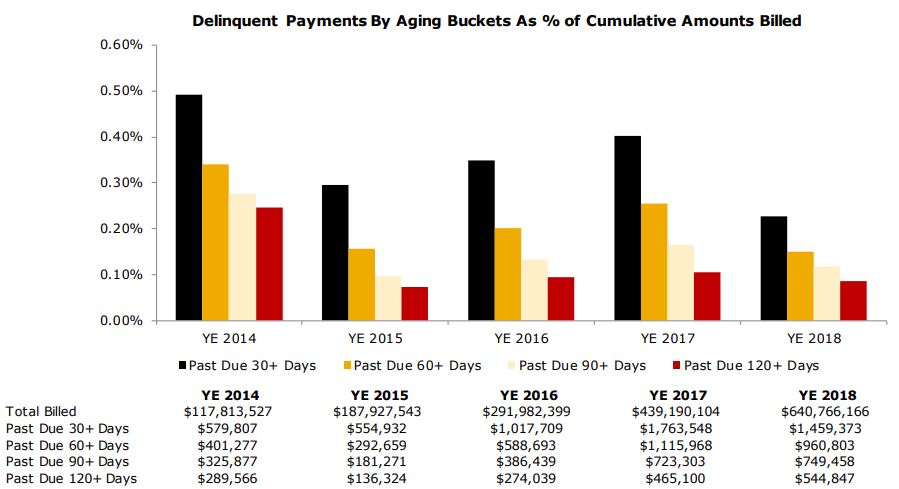

KBRA also noted the collection process used by Sunrun and some of the outcomes. For instance;

As of December 31, 2018, the Company’s portfolio performance has been exceptional with average delinquencies as a percentage of total billings for receivables more than 120 days past due at 0.09%.

The company noted that out of its approximate 242,000 customers, totaling just under 1.6 GW as of end of 2018, 13,823 accounts were transferred from one owner to another – netting 100.2% of the base contract value.

Sunrun’s first securitization was in July of 2015, for $111 million in asset backed notes.

As an aside, it ought be noted that it isn’t only Sunrun that gets high marks for meeting their production projections, as solar in general is highly predictable per Moody’s and other groups.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

We had sunrun put in solar panels two months ago and yet we still have not heard from anyone who can give us some information on when we could turn them on ! We have made phone calls emails and still nothing, melissa Lawrence is sunrun coordinator! Nothing no answer from her or anyone in the company I email her April 24th and no response! So highly disappointed! I am encouraging everyone not to get into sunrun!

If you are in California call the Contractors State License Board for assistance!

http://www.cslb.ca.gov/About_Us/Contact_CSLB.aspx