Mercom Capital has released its Solar Funding and M&A 2019 First Quarter Report, which shows a general increase in investment in the solar industry globally.

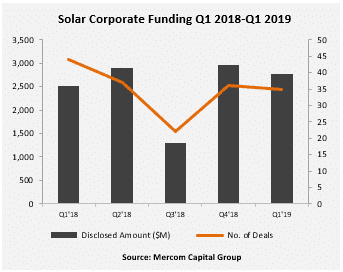

The report notes that total corporate funding – a sum of venture capital, public market, and debt financing – of solar power increased to $2.8 billion last quarter versus $2.5 billion in Q1 2018.

Global VC funding was up a bit to $176 million on 13 deals versus 22 deals totaling $161 million in Q1 2018. Yellow Door Energy received $65 million as the largest deal of the quarter. The Yellow Door deal got 37% of VC money. The 13 deals were spread across seven countries, with five of the deals in the US.

Public market financing increased to $247 million in three deals, from $103 million in four deals in Q1 2018. Additionally, debt financing increased a bit to $2.35 billion for 19 deals in the quarter, versus $2.3 billion last year.

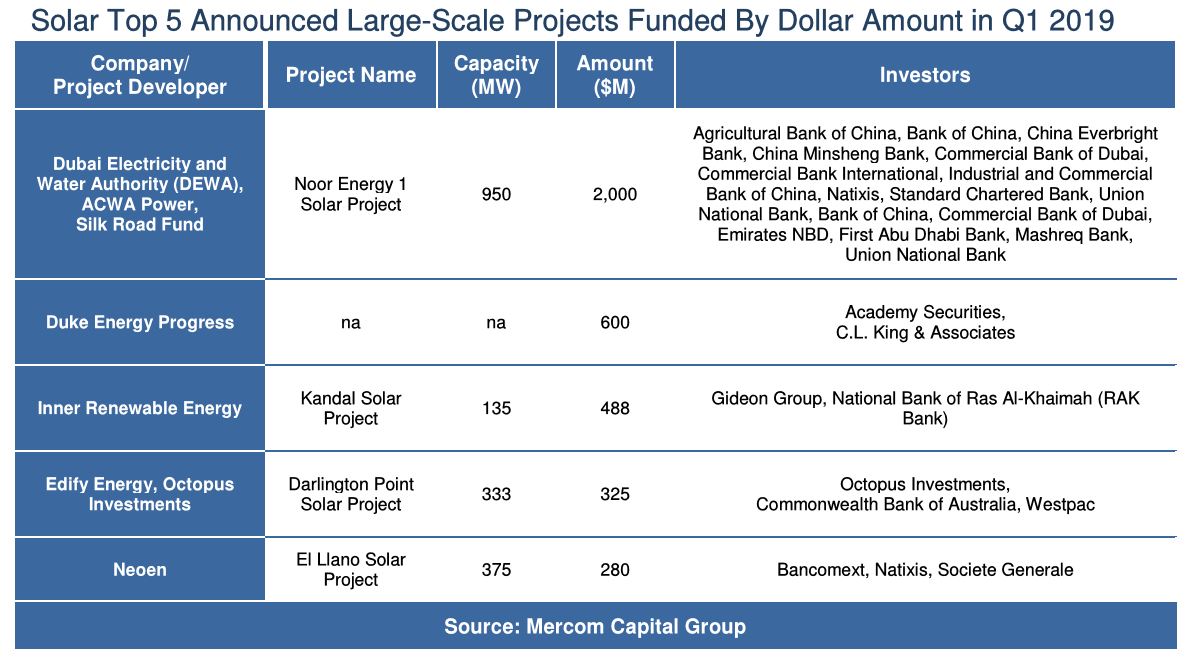

Large scale project financing roughly doubled, with $2 billion in financing for the Noor Energy 1 Solar Project. The 950 MW project received funding from a consortium of banking groups. Unique projects in the United States, like a LONGi and NexTracker project featuring single axis trackers and bifacial solar modules, also got funding.

In addition to large project financing, Mercom also reported 5.9 GW of projects acquired by investment groups at various stages of development. This is only reported deals, and likely did not include Enel flipping a 6 GW solar portfolio from Tradewind to Macquerie in late March, but possibly the National Grid purchase of Geromino Energy’s wind+solar portfolio at a cool $100 million.

The report noted new renewable energy and solar-focused funds raised a total of $3.8 billion in the quarter, for instance Madison Energy Investments – focused on ground-mount, rooftop and carport projects ranging from 500 kw to 20 MW – got $200 million.

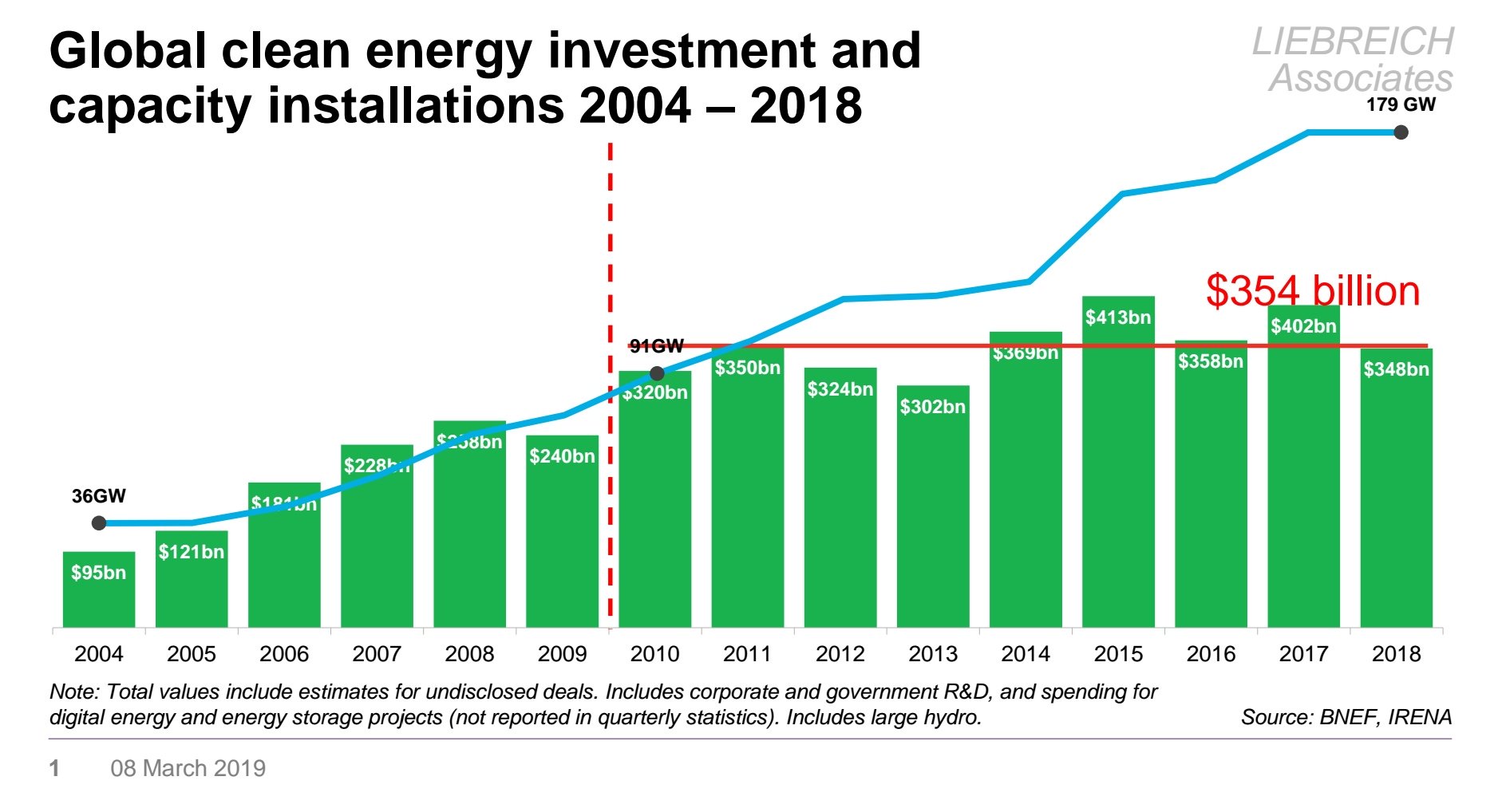

An interesting nuance of the solar market, and the renewable energy industry as a whole, is that total money spent has mostly stayed flat at ~$354 billion since 2010. While, as noted below, in 2010 we installed 91 GW of capacity and spent $320 billion, in 2018 we spent $348 billion but got 179 GW of capacity – an extra 8% in money spent, but a doubling of the capacity delivered. And this new capacity is performing at higher capacity factors – meaning we’re generating more than double the amount of electricity for about the same investment.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.