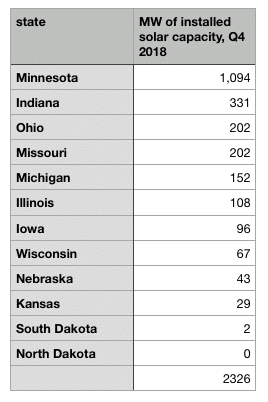

The Midwest isn’t the first region many people think of when it comes to solar in the United States. Though it is home to large, open spaces, farms, former industrial cities and famously friendly people, there is only around 2.3 GWdc of solar deployed across 12 states in the Midwest; or less than 4% of the U.S. total. Nearly half of that is in one state, Minnesota.

Furthermore, the region does not have the sort of aggressive renewable energy mandates found in the West or Northeast. Minnesota’s requirement that utility Xcel Energy source 31.5% of its electricity from renewables by 2020 is by far the strongest in the region, and no other state requires that its utilities source more than 25% of their power from renewables.

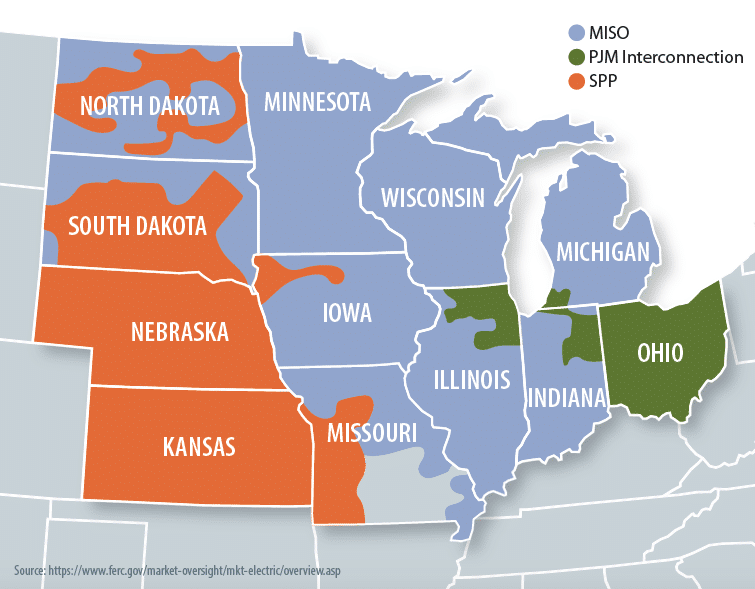

However, indications are that a boom is coming to the Midwest. pv magazine found 44 GW of large solar projects in the queues of the three grid operators that divide up the region: PJM Interconnection, MISO and SPP. Furthermore, at last count 200 MW of community solar projects were in the design and construction phase in Minnesota, and developers have put in applications for 1.8 GW of community solar projects in Illinois’ program – more than 10 times what administrators had originally designed the program for.

These figures do not account for the PV systems planned for the rooftops of homes and businesses. And while not all of this will get built, it is clear that the Midwest is about to see an unprecedented volume of solar development.

Wind, transmission, and solar

While only limited volumes of solar have been installed in the Midwest to date, this does not mean the region has not been important for renewable energy.

Midwestern states, and particularly those in the Great Plains, have been second only to Texas for the largest capacities of wind deployed in the United States to date. This was enabled by the building of long-distance transmission lines, particularly in the MISO grid, to get the electricity from wind farms to cities and towns.

The result is that Midwestern states have some of the highest levels of renewable energy on their grids of any states. North Dakota reached a volume of generation from wind in 2018 equivalent to more than 50% of the state’s electricity demand – a first for the United States.

These high volumes of wind deployed in the Midwest have impacts on the larger power system and for solar in particular. First, they have lowered wholesale electricity prices – but more overnight than during the day. And second, the transmission infrastructure which they have spurred can be utilized by solar.

This should sound familiar to those who have studied Texas, and this is not an accident. Sam Gomberg, a senior energy scientist with the Climate & Energy program at the Union of Concerned Scientists, says that the strategy of large-scale transmission deployment to enable wind was influenced by Texas’ success with its Competitive Renewable Energy Zones.

And like in Texas, both of these characteristics make the region ripe for solar development. “Solar’s ability to generate at least close to peak times makes it attractive to utilities trying to balance load and balance wind power,” notes Gomberg. “It’s a good complement to the wind resources that utilities have built up over decades.”

Wind still dominates in the Midwest, and in the three interconnection queues, pv magazine found more wind capacity than solar. But costs are falling faster for solar than for wind, and this is expected to reverse in the future.

Minnesota’s community PV gambit

The only state that has more than 1 GWdc of solar deployed in the Midwest is Minnesota. In fact, Minnesota held 47% of the total capacity deployed across the entire region at the end of 2018. This is mostly due to the state’s successful community solar program, under which around 500 MW of solar has been deployed in the last three years, making it easily the largest in the nation.

When pv magazine spoke to advocates in Minnesota about what made this program so successful, they consistently noted the absence of a cap on deployment, such as other states have.

When pv magazine spoke to advocates in Minnesota about what made this program so successful, they consistently noted the absence of a cap on deployment, such as other states have.

Additionally, in the early days the program didn’t have any regulations that prevented the building of multiple adjacent projects simultaneously. “Next thing you know the program opens up and people are submitting 50 MW next to each other,” notes John Shaffer, the executive director of the Minnesota Solar Energy Industries Association (MNSEIA). He estimates that there were 2 GW of initial applications under unlimited co-location, and that much of the capacity deployed to date is under that initial fleet of projects.

Another factor that made it easier for developers to build community solar has been that most of the capacity in Minnesota’s community solar program has been for businesses, not the homes of individuals. According to an analysis by John Farrell of the Institute for Local Self-Reliance, as of May 2018, 92% of the subscriptions for community solar in Xcel Energy’s service area were residential accounts, but that 88% of the capacity was subscribed by businesses and public entities. This means fewer accounts to sign up and service, and lower costs for developers.

The glory days appear to be over for Minnesota’s community solar program. Not only were the rules tightened years ago to bar the co-location of projects, but new projects under the program have been moved from net metering to value of solar tariff (VOST).

While MNSEIA’s Shaffer says that VOST is a “fair rate”, he also notes that the trend is for VOST to decline. “Since we’ve gotten VOST, it has systematically gone down every year, despite Xcel’s rates going up,” notes Shaffer.

While there is 200 MW still in the design and construction phase, it is not clear that large volumes will be built after this, and Shaffer says that under VOST the market is less than half its previous size.

However, he adds that the state’s C&I market is set to boom, and cites Xcel’s PV Rider program, where systems up to 1 MW are set to receive an extra US$0.03/kWh for the electricity they generate.

Ohio – moving from coal to solar

The next state expecting a significant solar boom is Ohio. While total installed capacity in the state at the end of 2018 was just 202 MW, currently there are six large projects totaling 750 MW, which PJM Interconnection lists as being in the engineering and procurement phase. Wood Mackenzie Power & Renewables says that it has not seen any announcements that any of these projects have yet started construction, but that as they are in a very advanced stage, they are likely to get built.

There is irony in the fact that this boom is happening in Ohio. Coal has traditionally provided the majority of the state’s power, and politicians have made moves to gut its Alternative Energy Portfolio Standard. This policy only requires that utilities source 12.5% of their power from renewables by 2026 – one of the weakest mandates in the United States.

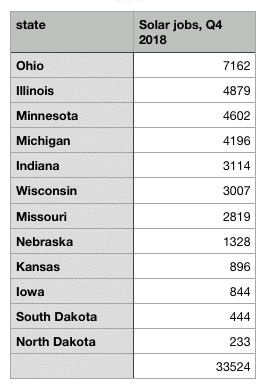

However, Ohio also has the largest number of individuals employed in solar of any Midwestern State, at over 7,000 workers. Some of this is due to the presence of First Solar’s sole U.S. factory, which until earlier this year was the largest solar factory in the United States. This is likely to increase, as First Solar is currently building a second 1.2 GW factory, which will be the second-largest solar factory in the Western Hemisphere when complete. And despite a lack of policy action at the state level, there appears to be an emerging consensus among the state’s business community behind solar.

However, Ohio also has the largest number of individuals employed in solar of any Midwestern State, at over 7,000 workers. Some of this is due to the presence of First Solar’s sole U.S. factory, which until earlier this year was the largest solar factory in the United States. This is likely to increase, as First Solar is currently building a second 1.2 GW factory, which will be the second-largest solar factory in the Western Hemisphere when complete. And despite a lack of policy action at the state level, there appears to be an emerging consensus among the state’s business community behind solar.

A Recent report commissioned by WalMart, Owens Corning, Whirlpool & Gem Energy calls on Ohio to take steps to get its share of the economic opportunity and job creation opportunities that clean energy presents. This jobs angle is particularly important in Ohio, which includes former industrial cities like Cleveland and Toledo which have struggled to re-invent themselves after industry left.

It is also notable that two of the companies commissioning the reports have ties to First Solar; Walmart owners the Walton family have traditionally been the largest shareholder in First Solar, and Rudolph Libbe is building the company’s factory in Lake Township, Ohio.

Perhaps the strangest member of this new consensus is AEP – the utility representing Ohio’s coal country. In 2017 AEP announced that it would invest $1.8 billion in renewables over the next three years, and identified a 1.37 GW solar pipeline to build out.

Illinois

But the state which holds the greatest promise for the region is Illinois. Illinois has the largest population of any Midwestern state, which doesn’t hurt. But while the state lagged on renewable energy deployment for a long time, the passage of the Future Energy Jobs Act at the end of 2016 has re-energized its market.

Colin Smith, a solar energy analyst at Wood Mackenzie Power & Renewables, says that FEJA will have the biggest impacts on the state’s community solar and distributed generation segments. In fact, the recent solicitation for community solar projects to qualify for incentives in Illinois attracted 1.8 GW of projects, more than 10 times what program designers had planned for.

Similar to Ohio, Illinois has long been a center for conventional energy. In this case, the headquarters of Exelon, the nation’s largest operator of nuclear power plants, is in downtown Chicago, and the state is home to no less than 11 nuclear reactors. This is a constant consideration in energy policy in the state, and the Future Energy Jobs Act included a compromise with nuclear power.

Pipelines and bubbles

While community solar is taking off in certain states, by far the largest capacity of projects being planned in the Midwest is large-scale solar in front of the meter. This has been demonstrated by the 44 GW of solar projects in interconnection queues across the region.

However, this number needs to be taken with more than a few grains of salt. Only a small portion of the projects in any interconnection queue actually get built, with ISO New England estimating that only 30% of the projects in its queue ever reach completion.

In the Midwest, it will likely be even less. All of the developers and analysts who pv magazine spoke with have stressed that even more than in other grids, the GI queues in the Midwest are clogged with speculative projects. In the MISO grid, the flood of project applications has led to a re-evaluation of the process for approving projects.

There are currently two proposals for reforming the process of project approval in MISO. One is a fast-track for “shovel-ready” projects that have approvals and a power contract, and the other is a process for shortening the overall time for project approval. UCS’ Gomberg notes significant push-back against the shortening of approval timelines; but says the fast-track proposal could move more quickly. However, it is still very early in the process, and Gomberg estimates that any motion to reform the process for getting interconnection approval will take at least six to eight months.

100% renewable energy

Despite the obvious bubble in the MISO queue, there is a lot of reason to be optimistic about solar in the Midwest. And this goes well beyond the community solar programs in Minnesota and Illinois.

Much of this comes down to raw economics, the falling prices for solar versus wind, and the need for midday power. However, there is another factor, and that is the increase in aggressive renewable energy mandates. Illinois Governor J.B. Pritzker stated during the campaign that he will put the state on a path to 100% renewable energy, and there is currently a bill to do just that.

Chicago Mayor Rahm Emanuel has beaten him to the punch, and his Resilient Chicago plan mandates 100% “clean, renewable” electricity in the city by 2035. This is particularly notable not only because Chicago is the headquarters of Exelon, but also because Rahm Emanuel brokered the deal that created Exelon and was a staunch ally of the nuclear industry, at least in the past.

And while Minnesota Governor Tim Walz has also put forward a plan to take his state to 100% zero-carbon electricity by 2050, the state’s largest utility, Xcel Energy, is already planning to decarbonize its electricity fleet by that date.

Nor is 100% the only target that counts here. As a compromise to end a ballot initiative to move the state to 30% renewable energy by 2030, Michigan’s two large investor-owned utilities have agreed to increase their renewable energy targets, with DTE Energy setting a 25% by 2030 goal and Consumers, 40% by 2040. Solar will inevitably play a role in the plans of both.

Wood Mackenzie senior analyst Colin Smith anticipates a higher level of growth in utility-scale solar in the Midwest than any other region. “There are a lot of dynamics at play, that make it a complex region to navigate,” states Smith. “The Midwest is the region I’m most bullish on in terms of there being potential for more solar than I’m looking at.”

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

For the first time in my 10 year long solar career, I am seeing opportunities and doing designs for parcels in Kansas, Nebraska and Wisconsin. Now that solar can deliver clean power under 4 cents per kWH with only the ITC as subsidy, we have passed the coal/oil/gas cost thresholds at scale and only need to turn our R&D efforts to improving storage costs and efficiencies to truly take on fossil fuel baseload costs. I think in 2-3 years energy storage will be dramatically cheaper as more manufacturing and lithium mines come online. We haven’t WON the war yet, but we’ve reached the Midway Point (pun intended).

https://www.solarenergymaps.com/ Has a lot more data to share on locations.

It would be nice that some of the wind states also start installing large amounts of solar. Since Nebraska has just now discovered that wind can make electricity I wonder if they will quickly figure out the sun can too. Missouri I don’t have much hope for. Not sure about the Dakotas.

Just moved to Wisconsin. Discover winter is mostly gloomy not sunny. So how is that going to affect the production on most days with no sun? Isn’t that a waste?

In Madison WI you can normally count on 1320 kWH per 1 kW DC per year. Not AZ but not AK either.

Check it out for yourself:

https://pvwatts.nrel.gov/