It was projected that 2018 would break $1 billion in total securitizations for residential solar leases, power purchase agreements (PPAs) and loans, and Sunrun just helped that along quite a bit. Also notable in this deal are improved credit terms, even as U.S. interest rates increase.

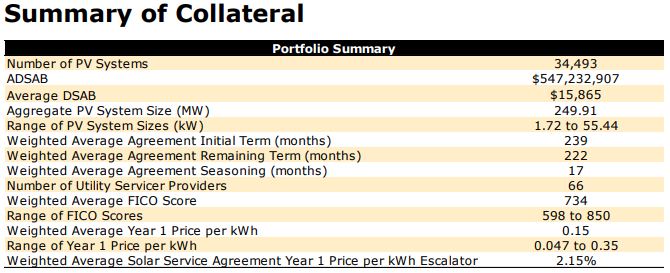

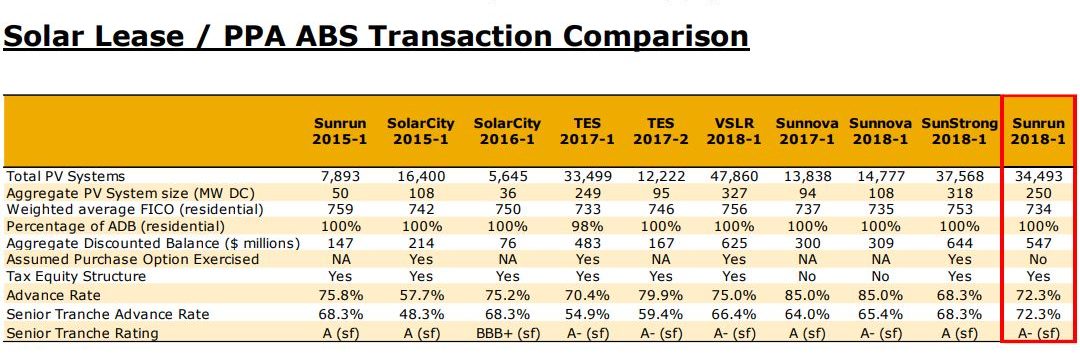

Sunrun has finalized the sale of a $322 million portfolio of solar power assets, which has received an “A” rating from The Kroll Bond Rating Agency (KBRA). It is composed of 34,943 rooftop solar systems, located in 19 states and 66 electric utilities, and this portfolio will generate a yield of 5.55% through its end of life in April 30, 2049. It is projected that the securitization’s share of the future electricity generation is worth $445 million, while the overall portfolio will generate $547.2 million in electricity.

KBRA also noted some interesting dynamics regarding estimates of future electricity rates:

KBRA assumed in years 5, 10, and 15 a portion (5%/10%/15%) of residential customers whose implied lease or PPA rate, on a per kWh basis, is higher than their projected utility rate would default and not make payments for 3 months. After 3 months, the defaulting customers would renegotiate their lease rate to 5% below the prevailing utility rate in their respective states at that time.

Sunrun has suggested that this portfolio’s pricing gave them lower than average cost of capital, matching Dividend Finance’s lower costs of capital.

As of recently, the default rating for residential solar power lease and PPA portfolios is A(-) to A.

The average home owner FICO score was 734, which is actually trending downward over time from the above image.

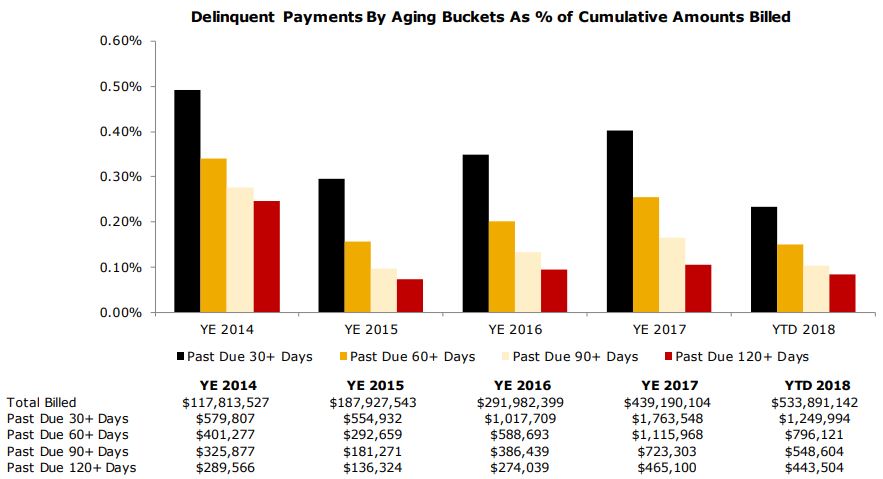

Sunrun’s July 2015 listing for $110 million of 7,893 rooftop solar systems was noted by KBRA as having performed in line with the agencies best case scenario regarding deliquent payments. Going back through 2014, the rating agency has suggested less than 0.5% of all accounts are delinquent in their payments.

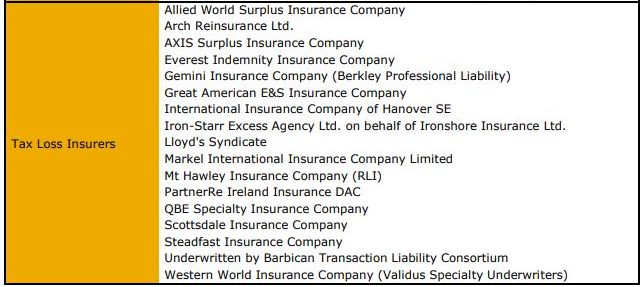

Seventeen individual companies were named as “tax loss insurers”, as it has consistently been deemed that there is a risk in the interpretation of the valuation of the tax equity portion of the portfolio. The bond rating agency considers that with the insurance and other financial structures, the risk rating is “+/-“, meaning it is probable it will end in favor of the investors.

The Athena portfolio follows in a long line of powerful portfolio names – Ukiah in 2015, Delphia in 2016, Juno and Bravo in 2017, and Electra in 2018.

Credit Suisse and Deutsche Bank Securities acted as co-structuring agents, and Credit Suisse, Deutsche Bank Securities and KeyBanc Capital Markets acted as joint bookrunners.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

The roof looks steep, I hope that cat is wearing Cougar Paws.