For a long time, electricity demand was seen as relatively inert. Sure, it fluctuated: people got up in the morning, turned on the lights, went to work, turned on machines, and in affluent, consumer societies the biggest peak was often in the evening when millions of consumers got home and fulfill their real societal function of turning on big-screen TVs and throwing frozen food in the microwave. And demand was obviously greater during heat waves when everyone turns on their AC.

But short of wars or disasters there wasn’t anything you could do about those natural cycles, right?

Wrong. Among the many dramatic changes happening in the U.S. electricity sector is entrepreneurs, utilities, policymakers and most importantly consumers waking up to the possibility of flexible demand, through the use of “smart” appliances, electric vehicles (EVs) and batteries.

And this can be a big help to the grid. Wood Mackenzie Power & Renewables (formerly known as GTM Research) defines demand-side flexibility as: “the ability of hardware and software to come together to create load shapes that are desired by utilities and market operators.”

What they don’t say is something that those who have been heavily involved in studying and predicting how high penetrations of renewables will work on the grid have been saying for years: that when you shift demand, you can integrate higher levels of solar and wind without having to revert to more costly solutions such as large-scale battery storage or more transmission to trade power with distant regions.

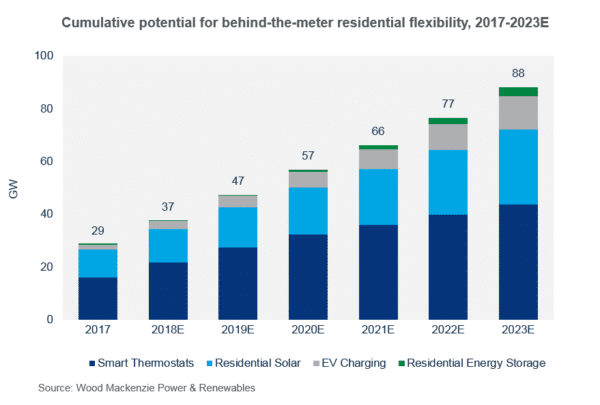

37 GW today, 88 GW by 2023

A new report by Wood Mackenzie puts some numbers on current and future ability of these devices to make the grid more flexible. The company found an estimated 37 GW of demand-side flexibility in the residential sector alone, and has forecast that this will balloon to more than 88 GW in 2023.

To put those numbers in perspective, there were 1,184 gigawatts of operating power plants on the U.S. electric grid as of March. Now some of those are reserves and certainly all of those were not operating all of the time, but this still means that currently residential flexibility is only 3.1% of our current generating capacity. 2023 numbers would be above 7%, if you assume that capacity won’t change much.

It is important to note not only that this is growing, but that much of the action regarding power demand is on the margins. A fair amount of load is static, but it is the peaks that give headaches to utilities and grid operators. These are the times that they have to keep extra, costly generation online, and that they plan for years in advance.

In terms of solar and wind, the biggest problems with mismatch of demand and supply tend to come at certain times, like excess generation on cool but sunny spring days on the weekend when there isn’t as much electric demand, or a lack of generation during still, cloudy winter days. In both cases moving a little bit of demand can have an oversized impact.

So why the rapid growth? Wood Mackenzie says that this is driven by the twin trends of growing customer demand in smart home devices, home energy storage and EVs, but also the progress of regulation to allow flexibility to extend beyond traditional demand response programs.

As examples of what this means, pv magazine USA recently covered a decision by California’s grid operator to allow behind-the-meter batteries to get paid to take electricity at times of negative wholesale prices – a win-win situation for battery owners and owners of big power plants. On the utility side, Arizona Public Service has announced three new residential energy programs to financially motivate customers to use cheaper daytime electricity in their air conditioning, batteries, and hot water heaters.

Policy & technology

Wood Mackenzie notes that residential energy storage systems and EV chargers make up the smallest portion of the current solutions deployed, but says that it expects these two to make up a larger portion towards 2023, in line with the exponential growth in the behind-the-meter battery storage and EV markets.

Policy is playing a role here as well, with the recent extension of California’s Self Generation Incentive Program (SGIP) promising to extend the residential battery boom that the state has seen. But beyond this dramatic example, Wood Mackenzie notes that many regions offer rebates and incentives for various devices that enable flexibility, whether these are utility rebates for smart thermostats or tax credits for buying an electric vehicle.

The report notes that not all of this 37/88 GW is created equal, in terms of impacts.

Different types of devices have varying capacities for grid impact. For example, residential energy storage can ease intermittency and mitigate peak demand for short durations. Residential solar can be paired with distributed energy resource management systems and smart inverters to respond to events on the grid. Grid-connected smart thermostats can be used to adjust HVAC energy consumption. The list goes on.

It is also important to note that it is still early in the age of the smart appliance, and that we will doubtless see many evolutions of these technologies and their role. But while the details and our understanding of them will evolve, one thing is clear: appliances and the grid are both changing, and that there is no going back.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.