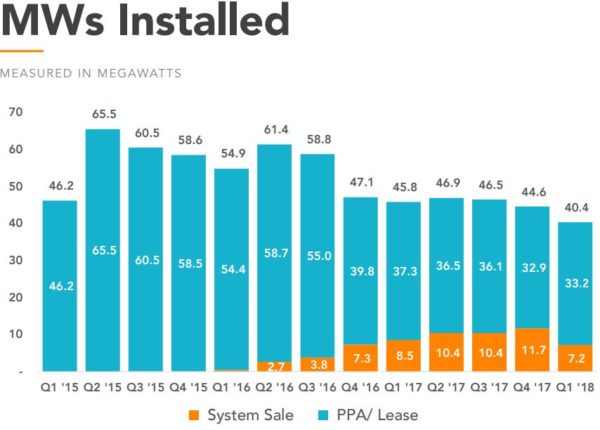

Vivint Solar installed 40 megawatts of solar power in Q1 2018. This is down from 46 MW a year ago, and also down from 45 MW in the fourth quarter of last year. And in contrast to the trend over the last two years, the company’s deployment of third-party solar saw a slight increase, while direct sales of solar fell 38%.

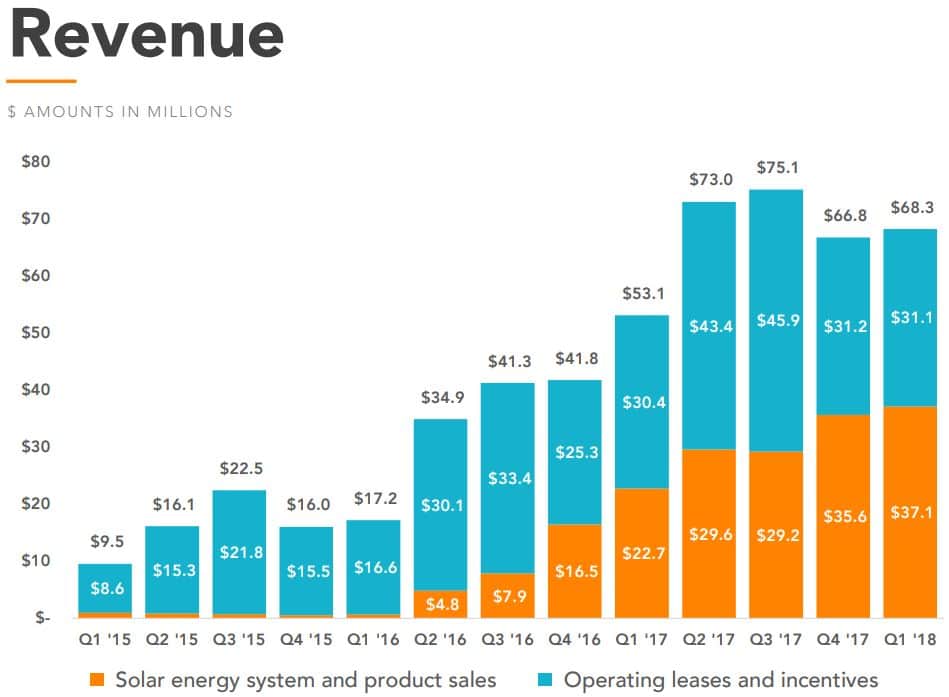

However, the revenue from the solar the company has deployed has increased significantly. Vivint’s $68 million in total revenue for the quarter was 28% higher than Q1 2017, and 2% over Q4 2017. Of the roughly $15 million in growth over the first quarter of last year, almost all of it – over $14 million – was in solar energy system and product sales.

To underscore the profitability of the company’s direct sales, Vivint estimates that its gross margin on that 7.2 MW was around 30%. The company says that the economics of solar that it is deploying through leases and power purchase agreements (PPAs) has also improved, due to being more selective about the projects that it takes on, resulting in more south facing panels, fewer installation services and easier wire runs.

On Vivint’s results call, the company referenced its innovations in labor. Vivint said this year it has moved to three-person installation teams, after using four in 2017, five in 2016 and six in 2015 and prior.

Much of the investor phone call was spent speaking of the company’s ongoing evolution in “dynamic pricing”, where salespeople are motivated to develop projects that have “improved system attributes”. This technique of aiming salespeople toward higher-attribute systems involves paying them at a higher rate for those attributes, which in turn has pushed up the average system cost to $3.15/watt from a range of $2.88-2.98/watt last year.

Vivint Solar’s Q1 2018 Cost per Watt Derivation

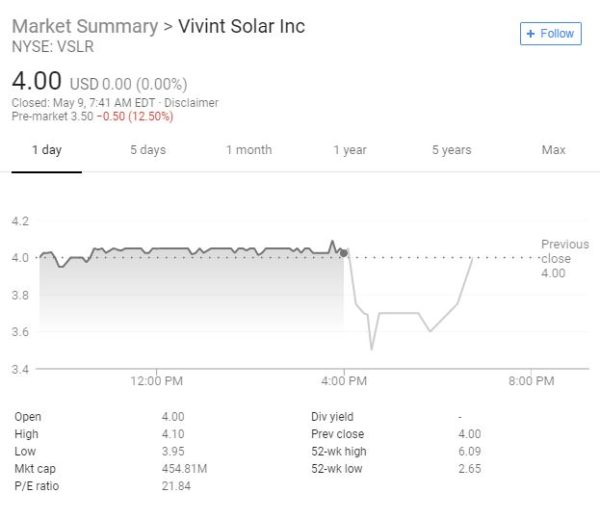

Upon release of data the after market reacted by trading down 10%, however as of this morning the price per share appears to have returned to yesterday’s relatively steady price.

Vivint also talked about significant growth in the California market. Total volume from the state was up 17% in the first quarter, however headcount was up even more at 38%. It is here where the company sees building momentum that will potentially drive sales growth later in the year. However, when pressed by multiple investment banks, Vivint executives were hesitant and declined to put a number on that growth. In the Q4 2017 phone call the company predicted the Q1 2018 40 MW number and suggested growth again in Q2 2018.

Vivint noted that Section 201 hadn’t yet affected their pricing, and a 2nd and 3rd quarter system price increase should be expected. However, the company did suggest that it is pleased to see panel prices already falling and that those price increases might be absorbed by the 3rd and 4th quarters.

No mention was made of the pending lawsuit in New Mexico regarding PPA structuring.

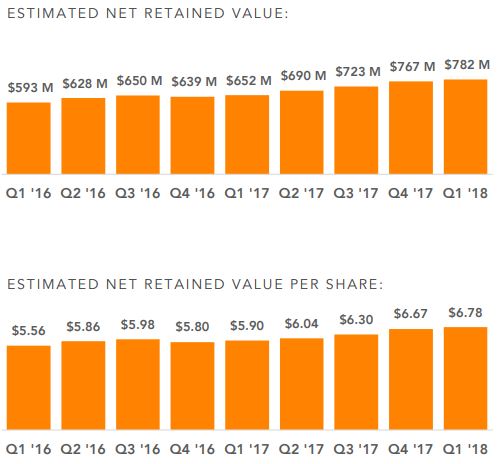

Vivint’s investor presentation also included an updated estimated net retained value chart. The company believes that if expected to fully depreciate all assets it would have a cash value of $6.78 per share. This is a 69% greater than the current share price of around $4.

While an estimate based on permit data by OhmHome suggests that the U.S. residential market increased 17% in Q1 2018, Vivint has yet to show pure MW growth in its sales. However, there is a seemingly sound argument that we are near the back end of this growth shift by the company, and there is a building expectation that not only will revenue grow in Q2 2018, but volume deployed as well.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.