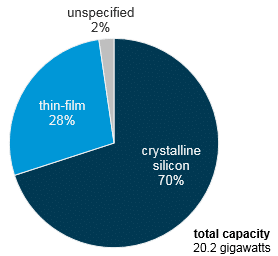

The U.S. Department of Energy’s Energy Information Administration (EIA) has released a new analysis of thin-film vs. crystalline silicon deployment in the U.S. utility-scale sector. EIA notes that while thin film comprises 28% of the 20 GW of large-scale solar deployed to date, that it was outpaced by crystalline silicon in 2016.

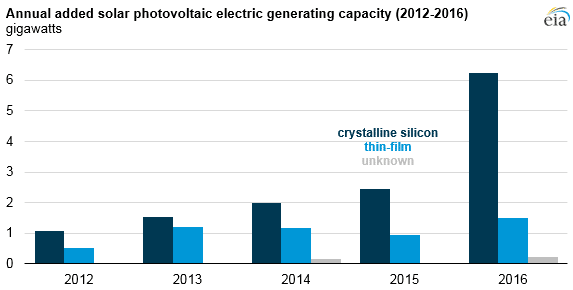

EIA estimates that of the roughly 8 GW of utility-scale solar deployed during that boom year in advance of the scheduled drop-down of the U.S. Investment Tax Credit, more than 6 GW was crystalline silicon. EIA reports that only around 1.5 GW of thin-film was deployed.

EIA estimates that of the roughly 8 GW of utility-scale solar deployed during that boom year in advance of the scheduled drop-down of the U.S. Investment Tax Credit, more than 6 GW was crystalline silicon. EIA reports that only around 1.5 GW of thin-film was deployed.

This could be the long-term result of the severe shake-out of the sector in previous years. When global solar prices began to collapse in 2012 due to massive volumes of crystalline silicon being exported from China, the thin-film sector was decimated. Thin-film company after thin-film company went belly up, eventually leaving only two manufacturers that reached gigawatt-scale: First Solar and Solar Frontier.

Japan’s Solar Frontier has largely prioritized its domestic market and has seen significant difficulties in breaking into the U.S. market, and as a result First Solar has dominated U.S. thin-film deployment. This can be seen in the technology breakdown. Cadmium telluride, which First Solar produces, makes up 97% of the thin-film deployed in the United States. Cadmium indium gallium diselenide (CIGS or CIS), such as is produced by Solar Frontier, barely registers.

First Solar: Constrained by capacity

And while First Solar has been able to overcome the main previous disadvantage of thin-film technologies – lower conversion efficiency – the company’s ability to supply the U.S. market is constrained by its manufacturing capacities. First Solar had reached around 3 GW of annual capacity in late 2016, but shut down lines to re-tool for its larger-format Series 6 product, meaning that it will only produce an estimated 2 GW this year, to be shared between U.S. and global supply.

Though First Solar has plans to expand manufacturing and is in the process of constructing two new 1.2 GW lines in Vietnam, it expects to only reach 3 GW of capacity between Series 4 and Series 6 in 2018 – which again will be shared between the U.S. and global markets. The company further reports that it is sold out of Series 4 into 2020, as well as most of its new Series 6.

Such limitations on thin-film supply will have ramifications for the U.S. market, particularly if U.S. president Donald Trump adopts the combination of tariff and quota proposed by SolarWorld. This would mean not only tariffs on imported solar, but a hard stop on the volume of modules and cells that could be imported into the United States. This in turn could further drive up prices, as well as limiting total deployment.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.