Editor’s note: Tomorrow the International Trade Commission (ITC) will vote on recommended trade action as a remedy for injuries that have been experienced by domestic solar PV cell and module manufacturers as a result of foreign competition. Ahead of this, IHS Markit has produced this exclusive analysis for pv magazine on what market participants should expect.

By IHS Markit

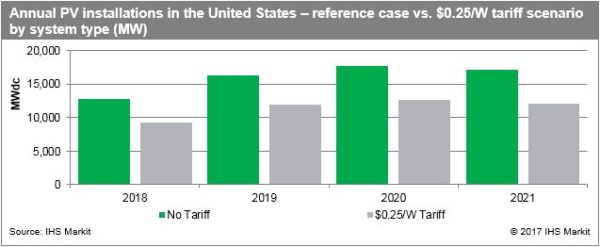

Question 1 – Using one of the more recent proposals from the petitioners, how might import tariffs of $0.25 per watt (W) for cells and $0.32/W for modules impact the U.S. market over the next several years?

IHS Markit modelled the reduced attractiveness of residential, commercial, and utility-scale PV in each U.S. state under the new proposed tariff (modelled as a $0.25/W module price increase). The analysis results in an 18 GW reduction to the forecast for PV deployments from 2018 to 2021 – a 28% reduction in comparison to the forecast reference case (prior to the petition being filed).

The utility-scale segment is projected to experience the majority of the impact, particularly in markets that lack supportive government mandates or incentives to deploy PV or other renewables. While module costs only represent between 10% and 20% of the total cost for smaller rooftop systems, they can represent as much as 30% to 40% of utility-scale PV costs, making any fluctuations in average module pricing much more significant for utility-scale project economics.

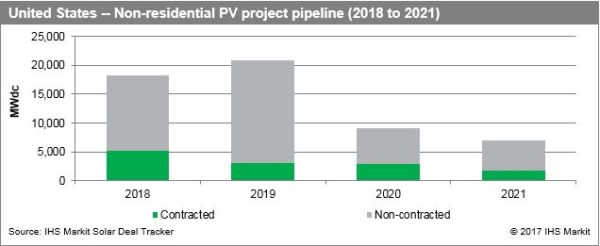

Question 2 – What does the actual pipeline of projects look like that may be impacted by new tariffs? Which state markets are likely to be impacted?

IHS Markit is tracking 55 GW of commercial and utility-scale PV that is planned for development and deployment in the United States between 2018 and 2021, the period for which new import tariffs may be implemented. Approximately 13 GW (23%) of that project pipeline has been identified as contracted with viable off takers. Contracted projects are more mature and likely to be deployed compared to assets that remain uncontracted, but even they remain subject to modification and cancellation if the economic expectations of the planned projects cannot be realized under new tariff regimes.

Utility-scale projects under development in state markets that lack mandated renewable energy policies such as renewable portfolio standards (RPS) are at significant risk of modification or cancellation if new import tariffs are implemented from the Section 201 trade case. In particular, Southern markets such as Georgia, Texas, Florida and Alabama represent a significant portion of the emerging utility-scale PV pipeline in the United States, collectively accounting for nearly 23 GW-DC of PV under development. Of that pipeline, only 15% has been identified by IHS Markit to be contracted with off takers in place.

The overwhelming majority of the pipeline is being driven by voluntary, cost competitive demand from end users such as utilities, municipalities and corporations. Price increases resulting from new tariffs could significantly reduce demand for utility-scale PV in these markets due to the lack of mandated policies to incentivize such deployments in addition to the relatively low levels of contractual obligation for the capacity.

Question 3 – If new import tariffs are implemented, what would the module supply landscape look like for the United States? How might the implementation of an import quota affect the market?

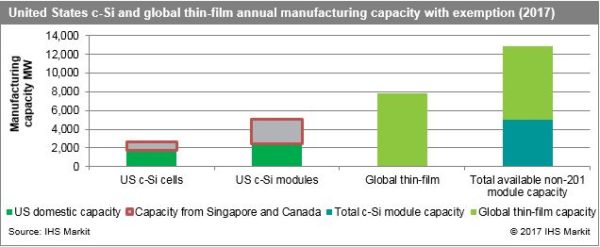

On September 22, the ITC voted unanimously that cheap imported solar equipment (with the exception of equipment from Singapore and Canada) has caused “serious injury” to American manufacturers. Supply will continue to be constrained in the United States even if the final decision might exclude capacity from Singapore and Canada, although new cell lines could surge in these countries.

The chart indicates the additional volume available for the US market with the inclusion of Singapore and Canada. For modules, it would represent and additional volume of 2.6 GW of module capacity between both countries. However, at the cell level, these two countries provide just 880 MW of additional capacity. Of course, the full 2.6 GW of module capacity would not be exempt unless additional cell capacity is built out to match the module capacity in the coming months.

Regarding SolarWorld’s petition to introduce an import quota, it is interesting because the suggestion indirectly assumes that there might be imports to the US market – and under the original petition all countries would be subject to import tariffs without exemption. This could only happen under two scenarios (1) the final tariff is very low allowing international suppliers to viably import modules, generating little to no incentive for building domestic manufacturing or (2) the final tariff is high but there are exempted countries and a small quota for cell and module imports would directly affect companies with existing capacity in those markets and would block movements from other companies to build new capacity in the exempted markets. This would be contrary to what occurred with the trade case in Europe that led to large capacity expansions from Chinese companies in South East Asia. If a small import quota is approved, it would lead to lower levels of installation in the U.S. market since domestic manufacturing is minimal and available global thin-film supply is insufficient for maintaining current growth trajectories in the market.

Question 4 – How might resulting tariffs impact suppliers of thin-film technology?

Our expectation is that thin-film suppliers such as First Solar and Solar Frontier will experience a significant increase in demand in the short to medium term with the introduction of new tariffs on crystalline silicon (c-Si) technology, potentially increasing their market share in the United States. Thin-film is likely to account for a growing number of projects in the U.S. market in the near-term and may become the default technology choice for utility-scale applications. Thin-film suppliers will need to make considerations with regard to increasing capacity and transitioning to new generations of product to meet demand, but they will ultimately be stressed with determining how to optimize the opportunity in front of them rather than mitigating damages and dealing with lower demand due to any new import tariffs.

As shown in the chart above, the global capacity of thin-film this year is less than 8 GW, clearly insufficient to supply the entire U.S. market in addition to other international markets if the approval of a high-tariff on international c-Si cell and module imports is finally approved.

Question 5 – How will the U.S. module trade case impact global solar demand?

To answer this question, it is important to understand that, in addition to the Section 201 case, there are important pending trade cases and policy announcements affecting the global supply chain in other key markets, which is generating uncertainty and a lack of visibility across the module supply chain for downstream players through 2018. So the actual impact of the U.S. module trade case on global solar demand will depend not only on the final decision in the U.S. market – low tariff or high tariff, quota or no quota – but also on the decisions regarding the local content case in India and upcoming feed-in tariff, or policy changes in China. If the U.S. and Indian markets close themselves to Chinese companies, who dominate most of the module supply-chain, this would undoubtedly affect module availability in these two markets, limit the number of installations and generally lead to oversupply in the rest of the world.

Having said that, IHS Markit is, at this moment, cautiously optimistic about global solar demand next year. The market is indicating a strong demand for modules for the first quarter of 2018 – despite very low demand coming from the U.S. market due to inventory build-up. Markets such as India, Mexico, Australia and regions such as South America and Europe that had serious difficulties procuring modules for H2 2017 thanks to strong demand from China and the United States are booking orders at this moment, and we have yet to see an indication of an upcoming collapse of global prices due to oversupply.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.