If you want the right answer, you need to ask the right question.

We at pv magazine have been among those heaping scorn on the grid study which U.S. Energy Secretary Rick Perry has ordered, given Perry’s public statements which suggest that this inquiry is built upon faulty and politically motivated assumptions. We have not been the only voices. Earlier this week trade group Advanced Energy Economy released a study which debunked the two major assumptions driving the report, showing that low-priced natural gas is mostly responsible for driving coal and nuclear plants off the grid, and that the replacement of such baseload does not necessarily have any significant impact on grid reliability.

However, this does not mean that the recent influx of cheap natural gas, wind and solar is having no impact on power markets. On the contrary, the build-out of gas, wind and solar is driving down wholesale power prices, including periods of negative prices in some markets, and in general is creating grave difficulties for generators.

Earlier today a new study emerged which looks at the way that these forces are threatening the entire model of competitive power markets. The Breakdown of the Merchant Generation Business Model by Power Research Group and law firm Wilkinson Barker Knauer notes that only 20 years after restructuring created a huge market for merchant power, many of the large merchant generators are headed for “a second round of bankruptcies”.

This dire warning is supported by plenty of evidence. While leading gas independent power producer (IPP) Calpine’s profit fell 61% to $92 million in 2016, Dynergy fell from a profit to a staggering $1.24 billion loss during the year. Meanwhile NRG lost $891 million, which led CEO Mauricio Gutierrez to famously proclaim that the IPP model is now “obsolete and unable to create value over the long term”, and NRG subsidiary GenOn Energy filed for bankruptcy earlier this month.

The report’s authors blame the downward price pressure on both gas and renewable energy, as well as flat demand growth for electricity. And while it is certainly true that zero-marginal cost wind and solar depresses prices, particularly in markets with high penetrations of these resources such as California, the AEE study (authored by Analysis Group) found that cheap gas was a far greater influence on depressed wholesale power prices than renewables were.

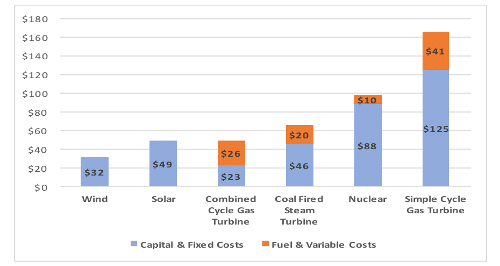

Some of the data presented in Breakdown supports that assessment. The report notes that the fuel costs for combined cycle gas turbines (CCGT), which represent much of the new generating capacity that has come online in the last 15 years, effectively set the price for wholesale electricity, and estimates that this price is currently only $26 per megawatt-hour.

Some of the data presented in Breakdown supports that assessment. The report notes that the fuel costs for combined cycle gas turbines (CCGT), which represent much of the new generating capacity that has come online in the last 15 years, effectively set the price for wholesale electricity, and estimates that this price is currently only $26 per megawatt-hour.

“When power prices settle at this level, not only is the fleet of CCGTs unable to recover its capital and fixed O&M costs, neither can any other resource,” notes the report.

The situation with prices is actually more difficult than this, as during off-peak hours power prices fall to the even lower variable cost of operation of coal, nuclear or renewable energy plants. Solar and wind have effectively zero marginal costs as they have no fuel and very low operations and maintenance costs, so they can bid in at zero. The marginal cost of wind can even be negative, given the impacts of the federal Production Tax Credit (PTC) which pays wind plants to generate.

“These new renewable resources reduce both the hours of operation as well as the prices received by the higher cost conventional generating resources on the system,” notes the report. “The simultaneous loss of output and the erosion of prices (similar to working fewer hours at a lower hourly rate) squeezes the gross margin of exiting conventional generators and potentially accelerates their second trip down a path to ruin.”

And the authors find that this is not a temporary problem, but an enduring weakness of a model that brings low prices to consumers but may not work in the long run. “The key weakness of the merchant generation business model is that generators’ revenues generally do not cover the all-in cost of supply, which includes the cost of capital recovery as well as the variable cost of operation,” warns Breakdown.

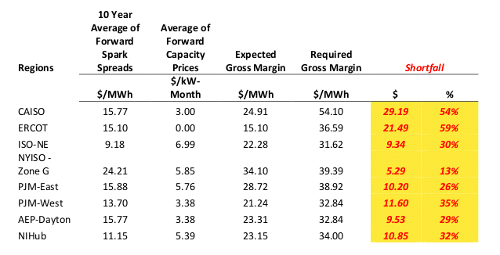

The report finds a 13%-59% shortfall between the required gross margin to keep merchant plants profitable, and the expected gross margins in various areas of the country. The worst region was Texas’ ERCOT grid, which is looking at a 59% shortfall, due to the absence of forward capacity prices, and which earlier this year saw the bankruptcy of a gas plant which had not even been in operation for three years.

The report finds a 13%-59% shortfall between the required gross margin to keep merchant plants profitable, and the expected gross margins in various areas of the country. The worst region was Texas’ ERCOT grid, which is looking at a 59% shortfall, due to the absence of forward capacity prices, and which earlier this year saw the bankruptcy of a gas plant which had not even been in operation for three years.

In a theoretical pure market economy an overabundance of plants would cause some to go offline and thus return power prices, the supply of electricity is a highly regulated market, in part to ensure that consumers have consistent access to power. As such, grid operators are mandated to ensure that they have a sufficient reserve of electricity capacity available to meet peak demand.

And while Breakdown warns that the inability of IPPs to turn a profit could ultimately have impacts on reliability, this is certainly not the case at present. Summer reliability reports from all major grid operators show reserves are still at healthy levels in all areas of the country.

It remains to be seen what will happen in the future as levels of zero or sub-zero marginal cost renewable energy grow. Calpine and NRG are already pushing for market changes in ERCOT, and nuclear generators have succeeded in securing “zero emissions credits” in New York and Illinois, but this has been rejected in other states.

Breakdown does not give a detailed proposal for a market solution, only alluding to ‘around market’ subsidies. But it is clear that something will have to give. “The losers in this scenario are not just the merchant plants with suffering bottom lines,” warns the report. “Customers lose in the form of higher and more volatile prices, decreased reliability, or both, and policy makers and regulators lose because they are left with the mess and no clear remedy.”

It is also not clear what all of this means for solar. Nearly all utility-scale solar projects in the United States hold power purchase agreements (PPAs), and of the few merchant projects which have been built in Chile, Mexico and Texas, several in Chile and the one in Texas are losing money and/or restructuring their loans. But even for solar projects with contracts the length of PPAs has been shortening, often resulting in a “merchant tail”, which means that they will ultimately be subject to these dynamics as well.

Furthermore, contracts acquired under the Public Utilities Regulatory Power Act of 1978 (PURPA) are also set to reflect future estimates of wholesale power prices, which continue to fall. This fall in prices has caused Duke Energy to push for changes to the implementation of PURPA in North Carolina, which is the largest market for PURPA-qualified solar projects in the nation.

More centrally, leading reports indicate that even future electricity systems with very high levels of wind and solar and lithium-ion batteries will need some form of backup, either in the form of hydroelectricity or gas generation where that is not available, particularly during the winter months. These generators will need to be able to afford to keep their plants online, and as such new market mechanisms to reward flexible generation may be needed.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.