A year after a collapsing SunEdison pulled out of the acquisition of Vivint Solar, the residential solar installer appears to have stabilized its business operations. And like Tesla/SolarCity, Vivint is moving away from the third party sales model towards more direct sales.

This is in line with larger residential market trends. According to GTM Research, during the fourth quarter of 2016 solar under leases and power purchase agreements fell to less than half of all residential solar deployed in the United States, after two years of declining market share.

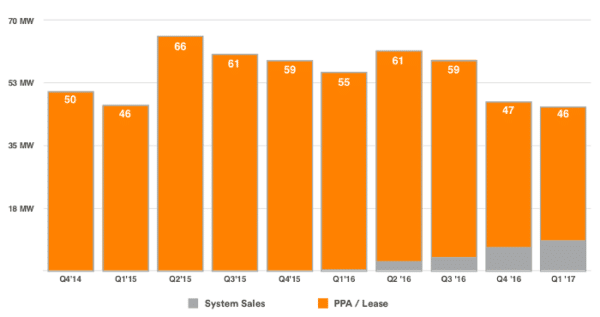

Vivint is moving slowly in this direction, and during the first quarter 19% of its sales were direct, compared to 14% in the previous quarter.

This move strongly affected Vivint’s quarterly results, and the extra cash brought in by the direct sales more than tripled the company’s revenue year-over-year to $53 million.

Like all third-party solar companies, Vivint is still reporting a loss on a quarterly basis. The company’s operating loss was $31 million and its net loss $55 million, only slightly more than the previous quarter.

However, Vivint’s third party sales brought in contracts with lifetime payments of $123 million during the quarter, for an additional $71 million in retained value after financing and other costs are accounted for.

Vivint’s other metrics indicate a steady state at a company which is smaller than it was before the botched acquisition by SunEdison. Vivint booked 52 MW but installed only 46 MW during the quarter, its lowest level since the first quarter of 2015 but only 1 MW less than the fourth quarter.

And while it was not mentioned on the call, some of this may be due to market contraction in the largest residential solar market, California. California suffered torrential rains during Q1, which slowed installations, and additionally the move to net metering 2.0 has impacted markets in the service areas of two of the state’s three largest utilities.

The company also brought down installed costs to $2.98 per watt, which is around the mid-range of the previous three quarters.

“I am more convinced than every that our disciplined approach is what the market needs, what benefits customers and what will eventually reward our shareholders,” stated Vivint CEO David Bywater on the company’s results call. “This is not an overnight solution, but it is a long-term approach to capitalize on a vast market.”

Thanks to hard work raising capital over the past few quarters, Vivint still has plenty of liquidity. While the company has drawn down its working capital facility, it still has $328 million in an aggregation facility.

Tax equity may be a bit more challenging. Vivint has sufficient tax equity funds to deploy another 77 MW of solar, which at the current rate will run out during the third quarter. But as CohnReznick Capital explained in an interview with pv magazine, raising tax equity has already gotten harder due to U.S. President Trump’s plans to slash the corporate tax rate to 15%.

Regardless, Vivint is maintaining its momentum, and in April expanded into the state of Rhode Island. During the second quarter, the company expects to install 44 to 48 MW, with a cost per watt hovering around $3.00.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.