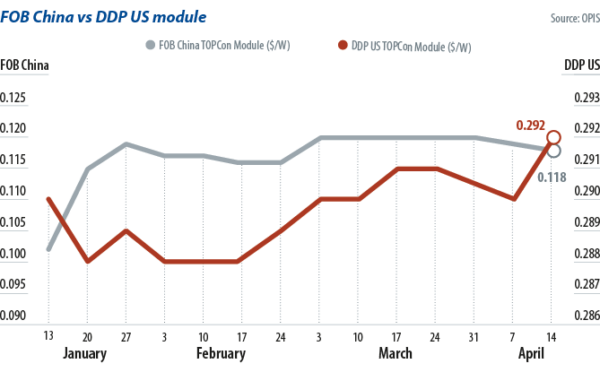

The Global Polysilicon Marker (GPM) has hardly moved since the latest outbreak of war in the Middle East. The OPIS benchmark for polysilicon produced outside China was assessed at $19.138/kg, or $0.040/W, as of April 14, only up 1% from Feb. 24, the week the war in Iran started. Over the same period, the China Mono Premium – OPIS’ assessment for mono-grade polysilicon used in n-type ingot production – fell by 33% to CNY 34.071 ($4.99)/kg, or CNY 0.072/W; FOB China TOPCon M10 cell fell by 11% to $0.05/W; FOB China TOPCon module rose by near 2% to $0.118/W.

Such price movements pale in comparison to the wild swings seen in oil markets, particularly in Asia. Prices of jet fuel and diesel, the transport fuels most affected by the Iran war, have more than doubled from $92.72/barrel (bl) to $210.73/bl and $92.68/bl to $185.75/bl, respectively, on a free-on-board Singapore basis over the same period, according to OPIS data.

Traffic through the Strait of Hormuz, a key oil and gas trade artery, has been restricted since the start of the war. But its effects barely apply to the solar industry where China remains the dominant manufacturing hub, far removed enough, albeit not completely, from the chaos in the Middle East. Instead, the bearish factors that have been weighing on the solar market since the start of the year remain in play.

Polysilicon oversupply

Inventory accumulation continued in the Chinese polysilicon segment, with no clear signs of a reversal to come. Order volumes per transaction from major ingot and wafer manufacturers continued to be extremely limited, a producer said, reflecting downstream efforts to minimize inventory losses.

In response to market conditions, manufacturers have adopted measures such as initiating maintenance activities and reducing operating rates. Several manufacturers in northwest regions have already implemented varying degrees of production cuts. China’s April polysilicon output is expected to fall about 8% from March, according to the Silicon Branch of the China Nonferrous Metals Industry Association.

Such a strategy might be reaching its limits. Some manufacturers were said to already be operating just a single production line, and even then at utilization rates of just 50% to 70%. Further significant operating rate cuts under such conditions would be increasingly difficult.

Major polysilicon manufacturers also have their backs against the wall in terms of production costs, where they need at least CNY 31/kg to CNY 32/kg just to cover raw material and electricity costs, according to industry sources.

Module uplift

In the meantime, module prices have seen modest uplift as a result of China’s removal of its 9% export tax rebates on PV products, which took effect on April 1. On paper, Chinese manufacturers could make up for the lost rebates by charging more for exports. But one producer told OPIS it may need to absorb a chunk of the rebate loss given the weak overseas demand in the second quarter of 2026. While China’s module market is grappling with the effects of the rebate removal, the US market is facing a different set of dynamics, as buyers await clearer direction on multiple trade and policy fronts that would affect solar module availability in the country.

A Section 337 petition for the US International Trade Commission is in its early stages – initiated following a complaint by thin-film manufacturer First Solar to block tunnel oxide passivated contact (TOPCon) solar imports that allegedly infringe its patent rights. Also, some Foreign Entity of Concern (FEOC) guidance around solar modules remains outstanding.

The price of US TOPCon modules reached $0.292/W, delivered duty paid, on April 14, eking out a 1% gain from end-February but nonetheless reaching its highest since the first week of January.

Given the divergent market and price dynamics, it is not surprising that while countries dependent on Middle Eastern exports have been trying to secure replacement fossil fuels to ensure energy continuity, the Iran crisis has also accelerated policy support for renewable energy deployment across the globe.

China, South Korea, Malaysia, Singapore and Thailand are just some of the countries in Asia that have announced solar initiatives since the start of the conflict. But with grid and financing issues still widespread in Asia’s renewable energy industry, rapid solar deployment remains challenging. Hanwei Wu

Hanwei Wu

About the author

Hanwei Wu, the editorial director of OPIS, leads the Asia-Pacific team in producing price assessments, proprietary data, and news analysis for the solar, carbon, oil, and petrochemical markets. In recent years, he has launched data products for the oil and renewables markets, including solar.

Hanwei Wu, the editorial director of OPIS, leads the Asia-Pacific team in producing price assessments, proprietary data, and news analysis for the solar, carbon, oil, and petrochemical markets. In recent years, he has launched data products for the oil and renewables markets, including solar.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.