Massachusetts issued final regulations for its Solar Massachusetts Renewable Target program, SMART 3.0.

The SMART program provides per-kWh incentives for solar projects up to 5 MW, with some exceptions. These exceptions include up to 10 MW for floating solar in a given program year, and up to 10 MW for individual brownfield projects and up to 7.5 MW for individual dual-use agricultural projects. The program enables the Department of Energy Resources to approve uncapped capacity for projects that are at least 25 kW, and behind-the-meter projects that are at least 25 kW or 250 kW or less.

“SMART 3.0 allows [the Department of Energy Resource] to annually adjust the program size and compensation to match market, economic and energy supply conditions,” Sean Burke, policy director for BlueWave, a Boston-based solar and storage developer, told pv magazine USA. “This will allow the Department to balance the needs of the grid, of ratepayers, and of the climate to deliver a program that promotes clean, affordable energy supply in the Commonwealth.”

SMART 3.0 implements new annual assessment

Among the changes, SMART 3.0 implements an annual assessment that the state will use to set annual program capacity and incentive rates. The assessment will incorporate a survey to program participants that considers:

- Progress toward greenhouse gas emissions limits

- Program participation rates

- Ratepayer impacts

- Regional/national solar costs

- Solar material & development costs

- Land use and environmental protection goals

Unlike the prior SMART programs, these compensation rates will be reviewed and reset annually, providing a built-in mechanism for responding to market shifts.

SMART 3.0’s incentive levels and available capacity

SMART 3.0 sets annual incentive levels based on project size.

| Generation Unit Capacity (AC) |

Program Year 2025 Base Compensation Rate ($/kWh) |

| 25 kW to 250 kW | 0.2821 |

| 250 kW to 500 kW | 0.2482 |

| 500 kW to 1,000 kW | 0.2113 |

| 1,000 kW to 5,000 kW | 0.1729 |

Projects less than 25 kW will have a fixed incentive level of $0.03 per kWh and $0.06 per kWh if they serve low-income customers.

Land Use

Ground-mounted solar projects that are greater than 250 KWac will not be eligible for SMART incentives if their footprint overlaps with any of the following:

- Biomap core habitat

- Top 20% (across MA) potential carbon emissions plus foregone sequestration through 2070

- Other applicable state & nationally protected lands including protected open space, wetland resource areas, and properties included in the state register

Low income adder

SMART 3.0 expands the low-income adder to additional types of housing and facilities, as well as systems that provide 100% of output to qualified affordable housing properties.

Community solar

SMART 3.0 stipulates that all community shared solar projects must enroll a minimum of 40% low-income customers. Alternative community solar projects, such as utility and municipal aggregation community solar projects must enroll 100% low-income customers.

Additionally, community solar projects must guarantee meaningful benefits to community solar customers, with at least a 10% discount for market-rate residents and at least a 20% discount for low-income residents.

Why SMART 3.0

SMART 3.0 came about from concerns that its predecessors needed improvements to improve solar projects’ long-term viability and meet further environmental and community-based policy objectives. The changes are based on the results of a multi-year programmatic review of the SMART program.

In June, the Massachusetts Department of Energy Resources filed emergency regulations for the Solar Massachusetts Renewable Target (SMART) 3.0 Program, which provides kWh incentives to solar installations. The 3.0 program implements annual capacity targets for each project type, while creating new incentives and adders for different types of projects. It also revises the incentive tiers, changing the eligible system sizes for each tier.

The previous versions used a declining rate block structure. Instead of adjusting the rates each year like SMART 3.0 does, the incentive rates dropped each time a new enrollment tier was filled. This model led to sharp drops in compensation, and by 2023, rates had bottomed out, with some customers receiving little or no incentive at all, according to EnergySage.

The revised changes will become effective Sept. 12. The first program year will be short, running from Oct. 15, 2025 to Dec. 31, 2025. Further information on the first program year is available here.

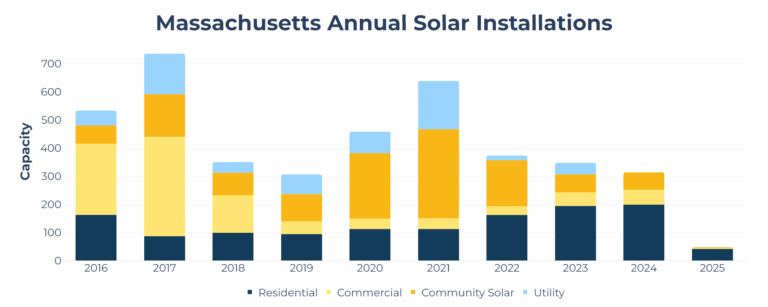

When Massachusetts first implemented the SMART program in 2018, the program filled up fast. The Bay State expanded the program from 1,600 MW to 3,200 MW of solar capacity in 2022.

The SMART 2.0 incentives will remain available in the Eversource and National Grid territories until 2027.

“Given the difficult federal climate, it is more important than ever that states step up to play a leading role in strategically crafting thoughtful, targeted programs to unleash clean energy and address rising energy costs,” Tim Snyder, Alliance for the Climate Transition’s vice president of Public Policy and Government Affairs, said in a statement.

The SMART program has driven significant solar deployment in Massachusetts, according to the Solar Energy Industries Association (SEIA). With nearly 5.48 GW of solar installed through Q1 2025, SEIA said 26.1% of Massachusetts electricity is from solar.

(Also read: States take closer look at value of solar, net metering policies)

This article was amended Sept. 3, 2025 to fix a typo that stated projects less than 25 kW had a fixed incentive level of $0.13 per kWh. The correct incentive is $0.03 per kWh.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

.30/km is no bargain for consumers.

So in other words, we the taxpayers are still going to be funding someone else’s business.

Creating a business model that can only survive with incentives is one step away from bankruptcy.

Take a look at oil subsidies

A program that takes $ from the low and middle income residents and gives it to wealthy financiers. So backwards – like most leftist policies…

You’re discussing all fossil fuel projects. Funding billionaires who destroy our planet, hijack our democracy, and kill any foreign leaders who try to stand up to them. All the polluting they do, we have to clean up after (eg all the empty oil wells that are left untapped). And the climate effects, our children will pay for.