Overproduction at levels that far outweigh end demand is unsustainable for any industry, and from 2022 to 2024, the PV industry significantly overproduced, leading to major inventory growth and backing manufacturers into a corner.

At the end of 2024, CRU Group believes global module inventory may have climbed high enough to account for roughly 50% of installations in the same year.

It is important to note that this oversupply did not arise through a decline in end demand. In 2022, 2023 and 2024, there were strong installations in the PV industry, with impressive year-on-year growth rates of 36%, 78% and 29% respectively. This installation growth has since slowed and CRU Group forecasts single-figure growth rates in 2025 and beyond, meaning that the “wiggle room” for excess production in anticipation of future market growth has narrowed even further.

With an excess of supply, manufacturers were left facing an incredibly competitive market. Costs exceeding selling prices means module manufacturers have often had to accept negative profit margins, or risk being forced out of the market altogether.

This meant that in extreme cases, some manufacturers resorted to cutting corners to reduce manufacturing costs wherever they could to preserve profit margins. In turn, the industry in 2024 and 2025 has the added hurdle of quality concerns. Subscribers to CRU and module and reliability testing facility Kiwa PVEL’s jointly authored “Solar Technology and Cost (STAC)” reports will be aware that PV modules failing quality tests have been seen at alarming rates.

Module innovation

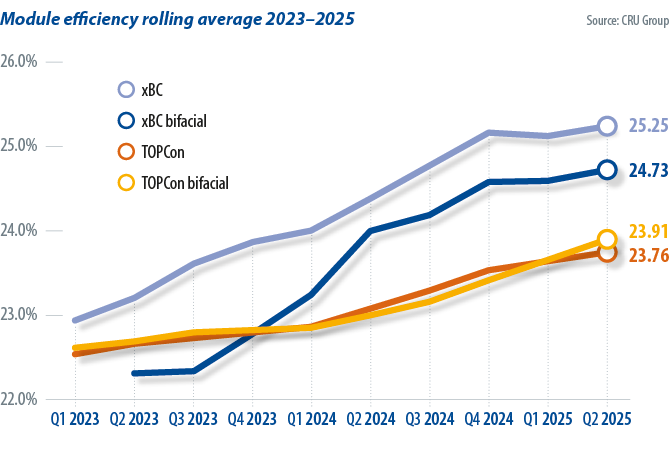

But it’s not all doom and gloom. Despite a challenging market for manufacturers, innovation and improvements to module performance have not stopped. From the beginning of 2023 to the second quarter of 2025, commercial maximum tunnel oxide passivated contact (TOPCon) module efficiency improved by 1.3% (absolute), increasing from 22.76% to 24.06%. In the same time frame, driven largely by Aiko Solar and Longi Solar, commercial back-contact maximum module efficiency improved by a huge 3.0% (abs.), increasing from 22.53% to 25.54% and proving that innovation has by no means come to a halt.

When considering the average efficiencies for the two technology categories, the improvement has been more modest. TOPCon’s average efficiency increased by around 1.0% (abs.) in the same time frame, with back-contact’s improving by 1.2% (abs.).

The most common question we receive from clients and industry contacts today is: When will the downward pressure on prices ease, and when will supply-demand dynamics return to balance?

Broadly, there are two scenarios that would result in the industry returning to supply-demand balance. One would require end-demand to increase to a level where excess inventory was no longer “excess.” But with global demand growth slowing in the coming years, this is an unlikely route back to equilibrium. A more likely scenario depends upon manufacturers scaling back production so that excess inventory will gradually be eliminated.

It was widely believed in 2024 that prices might begin to rebound in mid- to late 2025. This was based on the prediction that a meaningful number of smaller manufacturers would be forced out of production through bankruptcy in 2024. However, bankruptcies and decisions to withdraw from the PV market have come slower than both manufacturers and analysts expected.

Now, in the middle of 2025, unsustainable overproduction has begun to turn a corner. Since the beginning of 2025, “self-discipline” agreements between major Chinese manufacturers have helped to cut production volumes – polysilicon production volumes in January to April were down over 45% year on year, and wafer production volumes were down over 20%. While this has alleviated overproduction, high inventories for polysilicon and, in many regions, modules, have remained.

An opportunity to work through the inventory overhang might be approaching as manufacturing giants announce more conservative targets, at least by PV industry standards, both for capacity expansions and production guidance in 2025. There are rumours of even deeper production cuts being planned by leading players. If manufacturers do adhere to less aggressive production growth in 2025, it seems increasingly likely that downward pressure on prices throughout the PV supply chain may begin to lift in early to mid-2026. If manufacturers don’t enact the necessary production cuts, then a return to widespread profitability might remain “one year away” indefinitely, as it has for the past 18 months.

Beyond 2030

Technology transitions within the PV industry can occur rapidly when a rival technology offers improved performance at cost parity to the current mainstream technology. This was evident with the rapid transition from back surface field to passivated emitter rear cell (PERC), and in turn from PERC to TOPCon. In the space of two years, the market share of TOPCon increased from around 20% in 2023 to around 80% in 2025. TOPCon is expected to maintain its current market share dominance for the next two years. Beyond this, new rivals are already emerging, though it is not yet clear which is most likely to dethrone TOPCon in the future.

TOPCon and heterojunction (HJT) technologies have similar theoretical efficiency limits, with neither technology currently looking more likely to establish a sustained and significant efficiency lead. Today, the two technologies offer broadly similar maximum and average efficiencies commercially, with only a slight lead held by HJT in recent quarters. But despite TOPCon and HJT being competitive in terms of efficiency, the two do not currently compete in terms of manufacturing cost.

The low manufacturing cost of TOPCon has been key to the technology dominating in terms of market share and production capacities. As such, CRU Group believes that HJT will struggle to gain meaningful market share from TOPCon with its higher manufacturing costs, unless the technology can establish a meaningful efficiency lead. For HJT to achieve cost-per-watt parity – already accounting for the decreases to manufacturing costs we believe likely from our bottom-up cost modeling – the technology would need to achieve, and sustain, an efficiency lead of at least 2.5% (abs.). It doesn’t appear likely that HJT efficiency will overtake TOPCon at this scale.

A more likely technology transition is from TOPCon to back-contact, with back-contact likely to gain market share throughout the remainder of the decade by offering improved performance, higher efficiencies, and competitive costs. Currently, back-contact – specifically TOPCon-back-contact (TBC) cell architecture – has achieved efficiency leads of around 1.5% (abs.) over TOPCon and HJT. But this is only achieved for the top-performing back-contact modules in the second quarter of 2025, with the difference between the average efficiency of the two technologies being much smaller at 0.5% (abs.). However, back-contact technology offers these higher efficiencies at the expense of higher manufacturing costs in comparison to TOPCon.

As with all the key technologies on the market today, back-contact offers a huge spread of efficiencies within the individual technology category. This means that any sustained lead in efficiency would need to be achieved more widely across manufacturers to enable a widespread technology transition, at least, if manufacturing costs remain above those of TOPCon.

From our internal cost modelling, we currently expect cost of goods sold (COGS) for TBC to come close to parity with COGS for standard (both sides contacted) TOPCon by 2028, before potentially dropping very slightly below standard TOPCon by 2030. This all implies that we could see a significant transition to TOPCon back contact toward the end of the decade. However, there is no clear crossover of costs in our forecast, as we saw in the past with our modelling for TOPCon vs. mono PERC, which makes it unclear whether any shift would be industry-wide or whether the two technologies may coexist. In either scenario, we expect to see back-contact becoming a more common product offering among module manufacturers in the coming years.

The driving force of the PV industry is typically a motivation to improve performance or reduce costs. Since 2017, the industry has been in a “performance improvement” era, meaning absolute cost-reductions became harder to achieve, but module efficiencies improved rapidly. By the end of the decade, it is likely that crystalline silicon technologies will approach realistic efficiency limits. How will the industry continue to strive for further performance improvements?

Another technology transition looms on the horizon. In the early 2030s, CRU Group believes tandem technologies, specifically silicon-perovskite designs, may gain momentum on a large scale due to much higher efficiency potential in comparison to single-junction silicon devices. With some manufacturers already commercially producing perovskite-tandem modules today, albeit on very small scales, the early beginnings of a tandem technology transition are already in motion.

About the authors

Alex Barrows is head of PV at CRU Group. He focuses on when and how new technologies will influence the PV market. He also oversees PV market data analysis for the company.

Alex Barrows is head of PV at CRU Group. He focuses on when and how new technologies will influence the PV market. He also oversees PV market data analysis for the company.

Molly Morgan is a senior research analyst at CRU Group. Her areas of focus include tracking and forecasting evolution in solar module efficiency and architecture. She analyzes solar manufacturing capacity, production figures, and financial data.

Molly Morgan is a senior research analyst at CRU Group. Her areas of focus include tracking and forecasting evolution in solar module efficiency and architecture. She analyzes solar manufacturing capacity, production figures, and financial data.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.