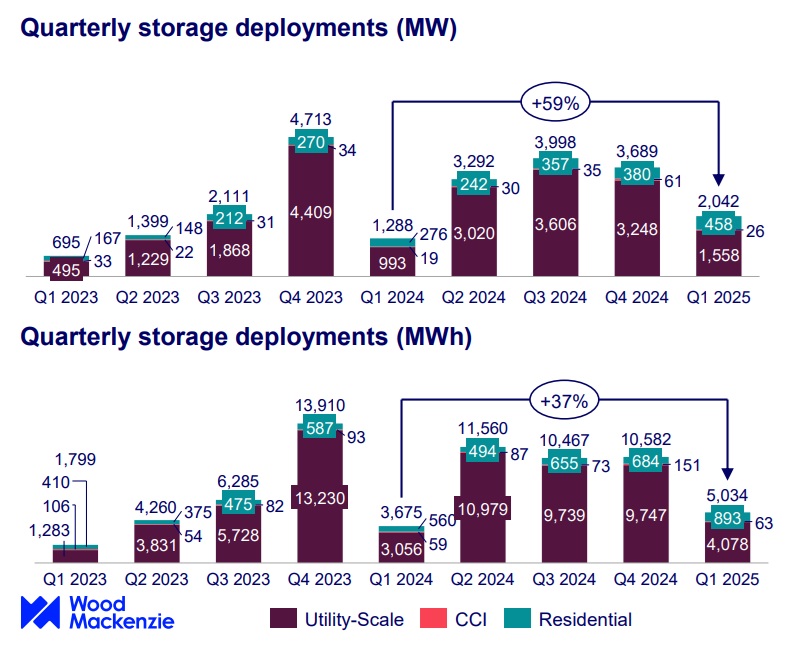

The U.S. energy storage market added more than 2 GW, according to the new U.S. Energy Storage Monitor by Wood Mackenzie and the American Clean Power Association (ACP). Despite much policy uncertainty, this was the highest Q1 on record.

The U.S. utility-scale energy storage market led the way, adding 1.5 GW/4 GWh of capacity in Q1 2025 for a 57% increase over the same period last year.

The residential storage market also saw the highest Q1 on record with more than 450 MW installed. California and Puerto Rico are the leading residential storage markets, contributing to 74% of the overall growth.

The commercial & industrial sector installed 26 MW in Q1.

Historically, California and Texas have been the energy storage leaders, but other states are embracing storage as five states accounted for 91% of the installations. California installed 457 MW, followed by Indiana with 256 MW, Arizona and Texas each added 255 MW and Nevada added 200 MW.

“We’re now seeing significant deployment of energy storage resources in emerging markets like Indiana, while states across the Southwest like Nevada and Arizona continue to expand their energy storage portfolio,” said Noah Roberts, ACP vice president of energy storage. “Energy storage was the second most deployed resource in Q1 2025, demonstrating its unique ability to be quickly built to address critical reliability needs.”

Indiana’s emergence as a leader was noted to be due to land availability and clear state permitting guidelines. The Hoosier State added 256 MW of new storage to the grid in Q1 2025, effectively quadrupling its operational storage capacity. Its progress is expected to continue, as the report finds that the state has more than 10 GW of new storage in the interconnection queue, which is the fifth largest storage queue in the country.

Into the future

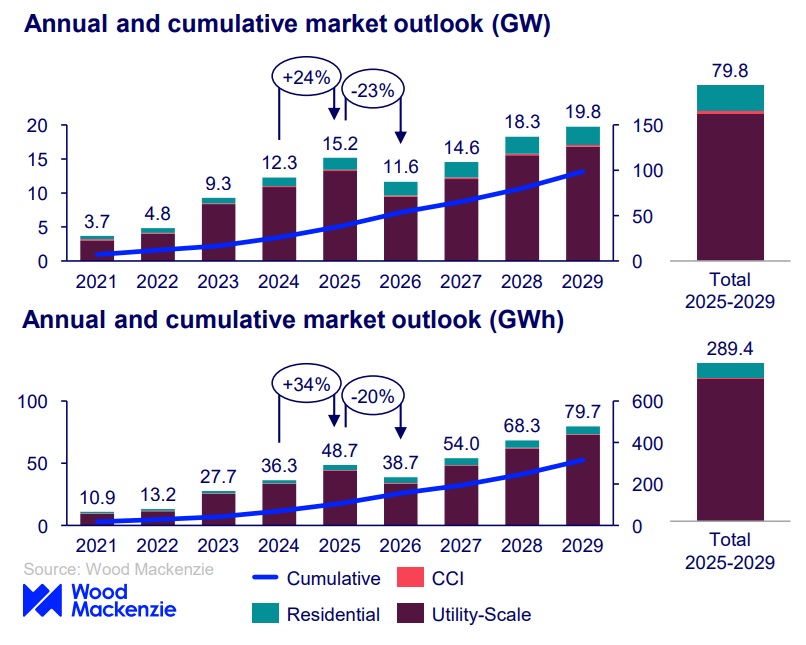

One main driver of utility-scale storage, according to the report, is the integration of storage into resource planning by utilities, regulators and communities. While utility-scale will continue to grow, it will fluctuate about 78% over the next five years dropping, at first, due to tariff challenges and then rising again when it scales up to meet load demand.

The residential storage sees nearly 15 GW installed by 2029, growing at a pace similar to Q1 2025. California’s NEM 3.0 implementation is the main driver in the residential market, as ratepayers seek to storage excess energy rather than sending it to the grid.

The C&I market will decline 42% over the five-year outlook, according to the report’s base case scenario. Here tariff uncertainty and the slow transition to NEM 3.0 in California are constricting growth.

The report findings account for uncertainty around the final version of the One Big Beautiful Bill, but the report was developed before the U.S. Senate Finance Committee version was released.

The latest version would spare energy storage-related investment tax credits (ITC) the same cuts proposed for solar generation and manufacturing sites.

On the manufacturing side, battery component fabs would retain full tax credits through 2029, falling by 25% increments in 2030, 2031, and 2032, as introduced by the Inflation Reduction Act of 2022. On the production side, the updated bill fares well for energy storage sites as they would continue to enjoy the full ITC through 2033, falling to 75% in 2034, and to 50% in 2035, before expiring in 2036, as envisioned in the IRA.

If the Senate version’s proposals for energy storage stay intact, then the report authors expect storage to rebound in 2028 and 2029.

“The Q1 2025 results demonstrate the demand for energy storage in the US to serve a grid with both growing renewables and growing load. However, the industry stands at a crossroads, with potential policy changes threatening to disrupt this momentum,” said Allison Weis, global head of energy storage at Wood Mackenzie. “It’s crucial that policymakers understand the importance of stable, supportive policies for the continued expansion of energy storage.”

In addition to clear, supportive policy, the main drivers of long-term demand of energy storage include load growth, capacity constrained independent system operators and state-level goals. Other factors driving demand include the transition to net billing, and lower costs of energy storage.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.