After a challenging 2024, marked by high inventory levels and declining residential demand, the inverter market is set to recover in 2025. Global inverter shipments are expected to increase 7% to reach 570 gigawatts alternating current (GWac), with an uptick in inverter shipments to the European market as inventory levels slowly rebalance, according to the latest forecast for the global inverter market from S&P Global Commodity Insights, the leading independent provider of information, data, analysis, benchmark prices and workflow solutions for the commodities and energy transition markets. Competition will remain intense as more players enter the industry, pushing suppliers to innovate and update their portfolios. See highlights of the S&P Global Commodity Insights forecasts below:

- Global inverter market revenue to grow by 8% in 2025

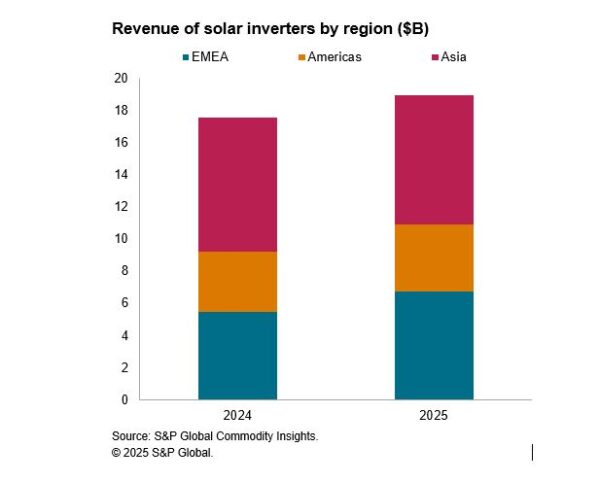

Following a challenging 2024, the global inverter market is expected to return to revenue growth, with total revenue estimated to reach just under $20 billion in 2025. A key driver of this revenue growth will be the recovery of the European residential market in 2025, which is typically a profit center for Western and Chinese inverter manufacturers, alike. Revenue in Europe is forecast to rise by 27% in 2025, driven by increased shipments to the residential segment, which suffered with consistently high inventory and reduced residential installations in 2024. However, European inverter revenue in 2025 will remain below 2023 levels as high levels of competition forces price reductions in the market. Elsewhere, revenue in the United States is forecast to rise by 16% in 2025 as the residential market recovers from a slowdown in demand and inventory oversupply. However, this will be offset by a revenue drop of 13% to China, as installations struggle to grow and high levels of competition drive down price and revenue in 2025.

Weak-grid markets are expected to be a growing revenue source for inverter manufacturers in 2025. Spurred on by success in South Africa in 2023 and Pakistan in 2024, an increasing number of manufacturers are seeking emerging markets and releasing cost-competitive products to meet local demands. Expect fast-growing markets to emerge in regions such as in Africa, the Middle East and Southeast Asia in 2025, as manufacturers have honed their products for weak-grid markets over the past few years.

- New suppliers add to overcapacity woes

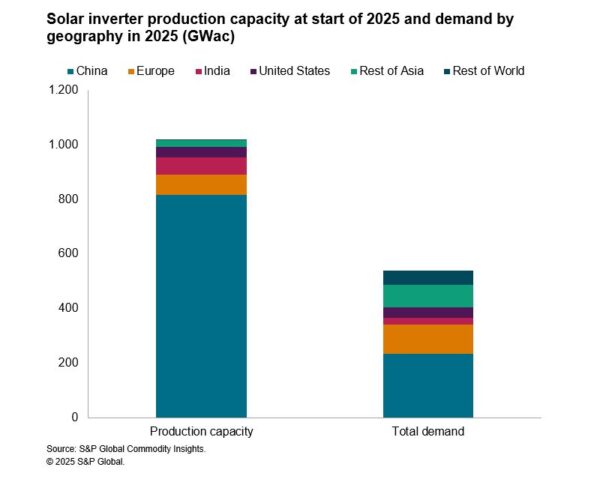

Manufacturers rushed to expand capacity through 2022 and 2023, as semiconductor shortages and booming demand for solar drove exuberance in the market. New entrants, mostly from China, flocked into the market lured by growing revenues and strong profit margins, while established players expanded their manufacturing base. However, by the end of 2023, the market had swung from a constrained to oversupplied market, with several expansion plans stranded. S&P Global Commodity Insights estimates that global inverter manufacturing capacity topped 1 TW at the start of 2025, far ahead of forecasts for 2025 demand at 538 GWac.

Overcapacity woes are added to by new entrants emerging from adjacent industries such as the white goods and portable electronics industries. New entrants and structural oversupply will force manufacturers to compete heavily on price and continue to update their inverter portfolio. With global solar installations forecast to grow at a CAGR (2024-27) of only 3.4% for the next 3 years, according to S&P Global Commodity Insights, manufacturers can expect tough market conditions to continue in 2025, with gradual price declines and pressure on ‘normal’ profit margins expected.

- Cybersecurity concerns will ramp up pressure on manufacturers

Cybersecurity announcements and requirements in various countries and regions increased in 2024, with this trend expected to intensify in 2025. Last year, Lithuania adopted legislation to prohibit Chinese manufacturers remotely accessing inverters at sites exceeding 100 kW, while in Germany, the Federal Office for Information Security has recently warned that the risk of foreign powers gaining control over parts of the country’s electricity system is growing. The growing requirements stem from the consequences of cybersecurity attacks. These can be significant; resulting in operational disruptions for consumers, a loss of trust in manufacturers, penalties from grid operators and even blackouts on the grid if the breach affects a large enough installed base.

Continued geopolitical tensions increase the risk of cybersecurity bursting onto the scene in 2025. Manufacturers are expected to face more scrutiny from regulators over the coming 12 months as record levels of solar continue to connect to the electricity grid, with the probability of barriers or even bans on certain foreign inverters due to rising national security concerns. This may have a secondary benefit of assisting local manufacturers to compete in their home market, given stiff global competition.

4. Sophisticated customer needs drive product evolution and digitalization in the behind-the-meter segment

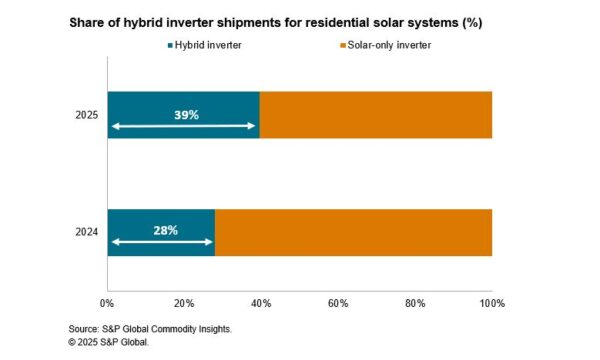

2025 will be a record year for hybrid inverters in terms of shipments. With the decline in financial incentives for solar power exporting to the grid and increasing awareness of self-consumption in key residential markets including Europe, California, and Australia, hybrid inverters, which combine solar and energy storage conversion, are becoming the standard for residential solar PV systems in many markets. In weak-grid areas, being able to pair with lead-acid batteries and switch between off-grid and grid-connected modes within seconds, will allow low-voltage hybrid inverters to continue to gain traction. In addition, more manufacturers are expected to release hybrid inverters with higher power ratings in 2025 to tackle commercial and industrial (C&I) scenarios.

Speed and ease of installation will be a key theme for the residential segment in 2025, particularly in Europe. Any efforts to alleviate installation time will reduce labour and total installation costs and will likely assist with increasing installation volumes. Integrated solutions that have batteries and power conversion systems (PCS) or as we call it at S&P Global Commodity Insights – ‘energy storage inverter’ combined as a complete device simplify installation to under 30 minutes and are expected to gain market share in 2025.

In 2025, with the introduction of dynamic tariffs in more markets and the maturing of virtual power plant (VPP) business models, behind-the-meter consumers will increasingly require their energy assets to respond to electricity tariffs to minimize bills and participate in power market trading and grid service provision for extra revenues. Inverter manufacturers are expected to make more efforts in the software area to meet customer needs and stay competitive— either by enhancing their own software offerings or by partnering with third-party software providers. The use of AI, both to assist consumer understanding and to act as an optimization agent, will also be a key differentiator for inverter suppliers.

- Innovation continues for front-of-the-meter products to reduce cost, increase efficiency and support grid stability

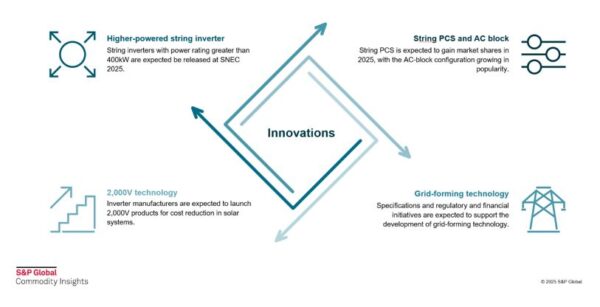

Inverter manufacturers are expected to release new products in 2025 to drive costs down further. String inverters with power rating greater than 400 kW are likely to be released at major trade shows in 2025. With higher power ratings, these string inverters will offer lower price per watt and save balance of system spend for solar systems due to lower cabling, installation, and operation and maintenance (O&M) costs due to fewer inverters used.

The other technology to watch in 2025 is 2,000 volts (V). Pushing from 1,500 V to 2,000 V allows the creation of longer strings of modules, leading to fewer strings for solar systems, which will help to reduce electrical balance of system spend by 10%–15%. The 2,000 V transition in 2025 will focus on central inverters, as string inverters require extra cooling techniques and subcomponents to advance to 2,000 V.

For energy storage, the share of PCS in front-of-the-meter applications is expected to grow in 2025, as the rack-level control it offers will provide higher efficiency and cycle life, easier maintenance, and increased uptime. AC-block configurations, which integrate battery racks and string PCS into one container, will continue to grow in popularity, due to its easier installation and land saving features.

In 2025, PCS manufacturers will continue to focus on grid-forming capabilities, which have become increasingly valuable to grid operators as renewable assets penetrate the grid. Additional specifications are expected to be released, along with regulatory and financial initiatives to bolster the development of grid-forming technology.

S&P Global Commodity Insights delivers comprehensive market data, benchmarks and insights for global energy and commodities markets, powered by a global team of specialists dedicated to delivering essential market intelligence. We enable customers to make decisions with conviction and create long-term, sustainable value.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.