pv magazine USA published an interview with BayWa r.e., discussing recent developments they have made in managing the sheep that assist with site upkeep. During the course of that interview, an interesting question arose: “Are sheep Investment Tax Credit (ITC) eligible?”

While BayWa r.e. didn’t share their opinion on the topic (our interview discussed O&M, not finance), they did share important data that pretty clearly shows how using sheep for solar O&M, rather than commercial mowers, is in the best interest of the project.

First, some numbers:

For the 270 MWdc solar project highlighted in the article above, BayWa r.e. estimated a need for approximately 900 sheep, which included 875 ewes, and 25 rams. Assuming that each ewe costs $350, and each ram costs $600, the cost for all the sheep totals $321,250. If we add the additional cost of running water lines to the 1,800-acre facility ($101,673), we arrive at $422,923. Some might argue that these costs should qualify as an expense, which is eligible for the ITC.

Considering the facility is 270 MW, the cost of the sheep is a trivial $0.0015/W, or less than two tenths of a penny per watt. If the project were to claim these costs for the 30% ITC, the financial benefits would total $126,876; a small drop in the bucket for a project worth a quarter of a billion dollars.

On the other hand, that’s a solid base salary for an engineer. And so we had to ask: Are sheep eligible for the ITC? For most tax professionals, the answer was a fairly consistent “no.”

David Burton, a partner at law firm Norton Rose Fulbright, described the logic as follows:

“The same reason a lawn mower is not eligible. Sheep are not “integral” to the generation of electricity in the view of the tax law. Someone does need to cut the grass or else it would grow so tall as to interfere with generation, but land and transmission are also not “integral” in the view of the tax law, and those are both needed for a functioning project; integral has a particular nuance in the tax law.”

We asked Burton if sheep might be considered eligible for an incentive in cases where the sheep were essential to the viability of a project, or to get through local zoning. He suggested that the question is complicated, but he leaned toward “no”, since generally, zoning costs are not eligible.

Amusingly, Burton added, “If the sheep manure was collected and fed into a power plant that converted the manure to electricity, then the power plant would be ITC eligible. This is called open-loop biomass.”

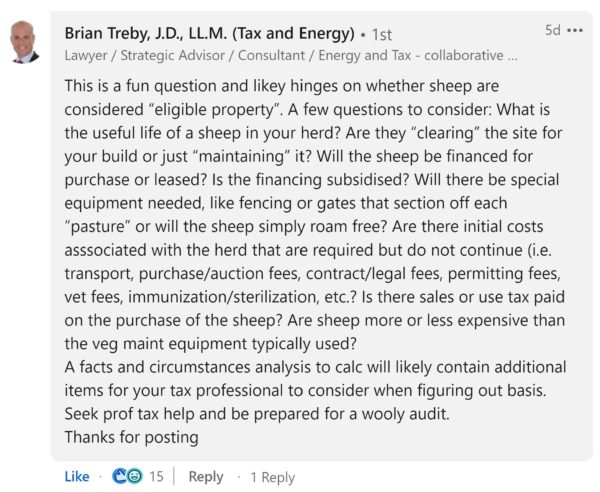

On LinkedIn, Tax & Energy Lawyer Brian Treby gave a broader perspective on the types of questions surrounding the issues. He directly followed up with pv magazine USA to add some nuance to the discussion:

The first point Treby made was that this is a question to leave to the IRS and Treasury, but that a project owner should ask first before jumping out too far.

Then he offered a masterclass in how to approach the situation:

An adage in tax, “pigs get fat and hogs get slaughtered” – unfortunately, somewhere out there a taxpayer will take the position on his/her return to include sheep in the basis calculation for ITC. Your sources seem to say clearly, “no, don’t do it”. My comment supposes they already have and asks questions, the answers depending might soften that precarious position. Having civil tax liability is different than tax fraud and sometimes showing vagaries to the trier of fact can reduce the penalties to a misguided taxpayer, especially where facts and circumstances may be considered.

Treby followed with a second comment:

A taxpayer’s patriotic duty and obligation is to pay all the taxes owed but not one cent more. If a taxpayer’s position can be justified because sheep are used at a certain time in a project’s lifecycle or financed one way versus another, and the law is ambiguous on the matter, a taxpayer’s intent to comply with the tax code can help mitigate the specter of fraud and even carry the day in audit or even court.

Professionals like Treby say that they ‘practice’ law or accounting or medicine. This is out of respect for the breadth of their field, and also because these trades are constantly evolving. Oftentimes this evolution results from private parties who follow their duty and push for definitive answers.

One path to supporting the particular position such as ‘sheep are eligible property’ is to request a Private Letter ruling on the matter. Treby notes that these letters can be time consuming, expensive to develop, and stressful when going through the process, but it is sometimes necessary for justice to be served when the Treasury department oversteps its authority.

In one example, commercial solar rooftops using bifacial solar panels that install a highly reflective white roof can claim the portion of the white roof in addition to a standard roof installation under the tax credit.

For what it’s worth, Silicon Ranch does deploy sheep at their facilities – many of which the company owns – and they do not include them in their ITC considerations.

The company notes that the ITC eligibility of the flock is less of a concern than being good land stewards and owners of livestock. Their Regenerative Energy land stewardship program will be covered later by pv magazine USA.

Nick de Vries, senior vice president of technology & asset management at Silicon Ranch, says “We have to think about water sources, predations, animal health, and forage levels. This is critical to get right, and is ultimately what will dictate whether your grazing program is successful or not.”

“On some of our solar farms we staff shepherds, have veterinary bills, breed sheep, and invest in infrastructure to support our land management activities. Though it’s related to our core business of renewable energy generation, we view it as an agribusiness within the company. Similar to projects where we have our own O&M staff who provide services to the entity that owns our solar power projects within Silicon Ranch.”

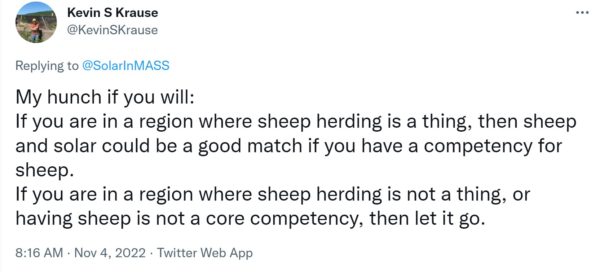

Kevin S. Krause, an auditor in the rates and tariff section of the Michigan Public Service Commission, responded to the ITC question by asking whether it’s actually in the best interest of the electricity rate payers.

In the Twitter thread, Krause noted that before any considerations were made, he would first need to see data. “Show me where sheep have been used, what they cost, what was the control group for comparison, and if all that pencils, why would I expect it to work here. I’d want at least three years of data.”

If there were a shift to this “new technology,” the auditors group would want to see evidence that this tool is both better than existing tools (gas lawn mowers), and better than other new innovative technologies, like robotic electric mowers. At Baywa r.e.’s facility, gas mowers turned their rocky terrain into projectiles, destroying 1035 panels worth $306,000. Their sheep damaged only two.

The regulator also noted that there isn’t really a place to record sheep ownership and operating costs in the Uniform System of Accounts form the Federal Energy Regulatory Commission.

Taking all of these details into consideration, Krause sees sheep as a cost effective agrivoltaic O&M solution, under the right circumstances.

So, while sheep might occupy a very important position in the agrivoltaic niche, they’re not yet considered fundamental to the upkeep of solar power facilities, according to the Internal Revenue Service. However, from a professional perspective using sheep to maintain solar assets is still a fairly new concept and as we were taught by BayWa r.e., there are compelling financial and performance-related benefits that sheep provide.

So… who’s throwing down on the pv magazine USA IRS’ Private Letter, “Sheep for ITC” GoFundme?

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

875 ewes out of 900 would make it a majority on EWEnion workers.

When the IRS comes calling, don’t serve lamb for lunch!