With just under 1.9 GW of utility-scale solar installed in Q3 2022, the industry experienced its slowest quarter since Q3 2020. This was expected to be a landmark year for solar, but global supply challenges have hampered growth, delayed projects, and driven up prices.

Despite this, long-term optimism remains. The American Clean Power Association (ACP) said in its quarterly report that the U.S. may deploy 550 GW of renewable energy by 2030. Solar is expected to lead the charge in this decade of energy transition, representing 59% of active renewable energy projects in queues. Along the way, the U.S. is expected to cut economy-wide emissions by 40% below 2005 levels. This progress will be accomplished by a clean power workforce of 1 million, said ACP.

“President Biden signed the Inflation Reduction Act (IRA) into law on August 16th. This unprecedented national commitment to clean power is the largest policy investment in clean energy on record. The IRA is set to catalyze clean energy growth, ultimately more than tripling annual installations of wind, solar, and battery storage by the end of the decade,” said the report.

Despite a slow quarter, 2022 remains the second highest year for solar deployment in history, falling just behind 2021 totals. Quarterly installs were down 23% compared to the same period next year. This slowdown may persist for some time as solar module supply issues remain, and the U.S. works to inject Inflation Reduction Act funds into a new domestic manufacturing supply chain.

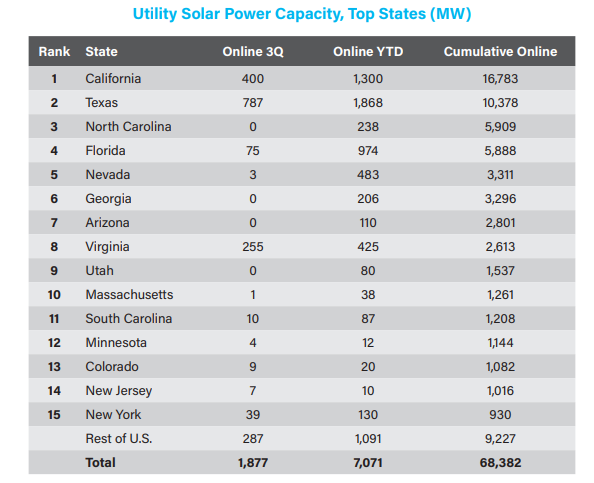

In total, solar installations in 2022 reach just over 7 GW. This brings total utility-scale solar operating capacity to 68 GW. In-quarter, developers activated 41 solar projects, spanning 18 states and totaling 1.87 GW, said ACP. California leads in cumulative installed operating capacity with 16.8 GW active, followed by Texas with 9.9 GW. Iowa increased its solar capacity by nearly 40% this quarter by installing 100 MW.

The largest utility-scale solar project commissioned this quarter was Old 300 Solar, a 430 MW facility in Texas. Developed by Ørsted, the project is selling its capacity to Microsoft via a power purchase agreement.

Utility-scale solar remains dominantly characterized by crystalline-silicon (C-Si) panels, though thin-film panels hold a sizeable foothold in the market. Of the total operational facilities, 69% are C-Si, and 25% are thin-film. Six percent of projects have not reported technology used. Thin-film deployment had landmark years in 2010 and 2014, where it represented more than 50% of installs. It is possible the technology will gain ground on C-Si, as the U.S. domestic manufacturing supply chain ramps up. Thin-film panels are typically provided by U.S. companies, primarily First Solar, which provides thin-film Cadmium Telluride (CdTe) panels.

Single-axis trackers, which rotate panels on one axis to follow the sun, are a rising trend in this sector, said ACP. The technology currently accounts for 61% of operating solar capacity. Fixed-tilt mounts make up 25% of operational capacity, while 2% use a dual-axis tracker. ACP said it is unable to determine the remaining 12% of operating capacity.

Makeup of tracker technologies varies widely by state. In New England, single-axis trackers support only 8% of active capacity, while 86% of capacity in the Plains region are mounted on single-axis trackers.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.