Battery storage is the fastest growing segment of the renewable energy sector. It is projected to be a trillion dollar market. Installation of stand-alone battery storage projects is expected to increase fivefold in the next four years. Another substantial portion of the commercial battery storage market, almost one-third, will be installed in combination with solar facilities.

The financial markets for battery storage projects are beginning to catch up with the solar and wind markets. Still, many differences remain.

I spoke with several experts on financing battery storage projects at a recent power finance conference held in New York. The discussion highlighted the growing opportunities for installing storage projects, but also where the storage markets still need to mature to make them more financeable.

Breaking Down the Storage Market by Segment

The energy storage market is not monolithic. According to Josh Prueher, Chief Financial Officer of Broad Reach Power, investors and developers should strategically break down the storage market by its various segments. Prueher explains that “a solar-plus-storage project in Kern County, California, for example, will be built and financed based on a long-term power purchase agreement, which will have a different revenue and risk profile than a front-of-the-meter project built in the Los Angeles basin on a merchant basis with a California Resource Adequacy (RA) capacity contract.” These markets are different from Texas, “where storage projects are being built to provide short-duration products into the market, often with selective hedges.” Prueher therefore recommends that companies strategically first determine how to design, install and operate the storage project to optimize revenues, and in what market, and then find the right financing structure to fit that profile.

Prueher sees the greatest market opportunity in developing “front-of-the-meter” merchant storage projects. These are battery storage projects tied into the wholesale power grid that do not have long-term offtake contracts. They therefore provide less revenue certainty compared to that traditionally required by lenders and tax equity investors.

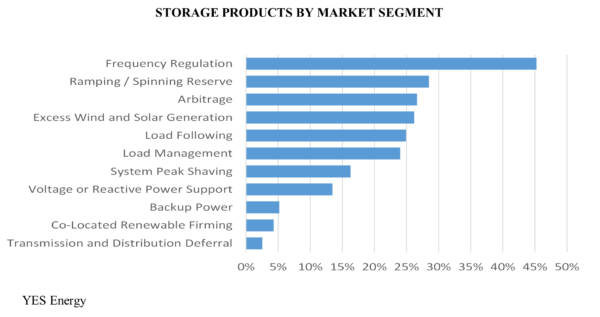

Michael McNair, President of Yes Energy, an energy research and modeling company, agrees. He notes that frequency regulation and other grid support-oriented ancillary services have been the main products sold by storage projects, but that arbitrage has increased significantly over the past 10 years. For storage projects located in ERCOT or California, the product mix provided by storage centers around selling into the wholesale day-ahead and real-time markets in the California ISO, or CAISO. Prueher says that his company participates in these markets through “decisions partially based on algorithms, and partially based on being in the trading loop in the market. That construct drives our storage development business.” Broad Reach’s goal in the California and Texas markets is to seek to optimize a project’s merchant revenue. “Think of a battery storage project as a leapfrog to direct procurement of commodities as part of a disaggregated supply chain, where the battery is long volatility and the customers are short volatility. If I am a load-serving entity in Texas, [I am] likely short that volatility to a large extent. I will therefore want to hedge my exposure, particularly after what happened in ERCOT last February. Similarly, if I am a wind developer, I might have basis risk or other issues that having storage in my portfolio can address.”

Other types of products sold by storage projects into the market include tolling arrangements and straddle, or “high/low” products. For example, a storage project might sell a call option on two or three of the highest priced hours in the day-ahead market; or it might sell the spread between the bottom two and the top two hours to a municipality or co-op that has load and wants to lessen its volatility exposure.

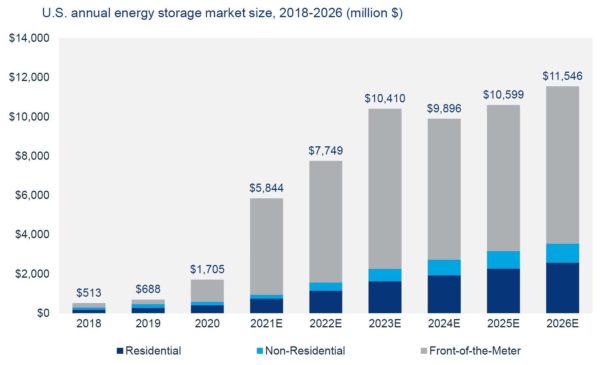

From Wood Mackenzie’s US Energy Storage Market Report

Storage projects also offer more traditional swap products, such as fixed for variable, along with the full suite of ancillary services. McNair identifies the more common projects as responsive reserve, reg-up/down, non-spinning reserves, and energy products.

Greg Randolph, Managing Director of the New York Green Bank, spoke about the New England and New York markets. Randolph notes that banks have a much stronger grasp of the various segments and products supplied by storage projects into the market than they did even a year ago. Randolph says, however, that the markets for merchant storage projects in New York, PJM and New England are quite different from, and less resilient than, the California and Texas markets.

Very few stand-alone merchant storage projects are being built today in New York. Even fully contracted stand-alone projects are difficult to finance. This is largely due to the federal investment tax credit not being available for standalone storage projects. Even with the ITC, the economic margins for front-of-the-meter merchant storage projects are “just are not there.” Randolph explains that the market has heard predictions for years that fossil fuel generation plants will be shutting down in New York, which has not yet occurred. Once these retirements happen, Randolph says, “the markets and regulators will put much more focus on the need for peaking capacity and using battery storage capacity to improve the reliability of the grid.” Margins for battery storage services will then improve and become more predictable, which in turn will attract debt financing into the market.

Until then, Randolph says, developers will focus on markets like California and ERCOT, where the blackouts and extreme energy prices experienced by consumers last year highlighted the need for battery capacity and improved the margins for investment in battery storage. For New York to get to that place, debt providers will need to get more comfortable with pricing for ancillary services. Until that happens, Randolph says that, to attract financing, battery storage projects will need to contract a larger portion of their revenue stream and pair it with solar to be eligible for the ITC.

There are signs that these changes are coming to the northeastern markets. New York State just increased its targets for solar generation from 6 gigawatts (GW) to 10 GW by 2035. The state is also building out 3.5 GW of offshore wind, expected to come to market around 2027 or 2028. This increased reliance on intermittent resources creates a huge demand for storage, particularly in the southern parts of the state that include the New York metropolitan area and Long Island, where most of the offshore wind will come to ground. The demand for storage will be compounded by the fact that New York’s transmission system is built to bring power from the northern part of the state to the southern part. The only way to manage the constraints created by the additional offshore wind, lack of fossil fuel plants and transmission constraints will be to enhance transmission and storage capabilities in the downstate area.

In the interim, developers are pairing storage projects in the Northeast with solar projects in order to receive the federal ITC. In New York, storage also receives the benefit of Value of Distributed Energy Resources (VDER) pricing, an attractive pricing formula established by the New York Public Service Commission. Mark Repsher, Managing Partner of PA Consulting, noted that certain economic benefits come from pairing storage with solar, such as savings on interconnection costs and construction. Yes Energy’s McNair added to the list the engineering and siting benefits that come from pairing storage and solar. Repsher cautioned however that the concept of siting storage with solar projects in the northeast in order to receive the ITC creates a forced fit that drives decisions as to where storage will get located. He would like to see the pricing and governmental incentives designed in a manner so that locational decisions for storage are made based on where the storage project provides the greatest benefit to the grid and to consumers, such as by alleviating price volatility, eliminating bottlenecks and reducing system constraints.

The Markets for Financing Storage Projects

Bank financing is generally available for storage projects. The cost and terms of bank financing may vary significantly depending on what segment of the storage market the project is participating and its physical location.

For a storage project in New York with committed tax equity, Green Bank’s Randolph says it will loan 90% of construction costs during the construction period, with the expectation that the tax equity will come in upon completion and be used to pay down the construction loan. This will result in around a 70% loan commitment for the term of the project. If a contracted storage project does not have tax equity, the project will likely see a 70-80% loan during the construction phase that will roll into the term period. By contrast, a merchant storage project will only receive around 50% to 60% debt financing and require higher debt coverage. The cost of debt will range between LIBOR plus 275- to LIBOR plus 350, according to Randolph.

The terms for financing a storage project in California are more attractive. A fully contracted stand-alone storage project (e.g., with a fully tolled 15-year offtake contract) can obtain a bank loan for up to 90% of the construction costs, and 100% for term financing. The cost of financing a merchant project is less attractive. A merchant storage project in California, having an RA capacity contract representing 25% to 40% of the project’s dollar per kilowatt month revenue profile, can receive 70-80% debt financing. This is a marked improvement from the past. Mark Repsher of PA Consulting noted that the financial community has gotten increasingly comfortable with storage projects selling products on a day-ahead or real-time basis into the CAISO markets. Says Repsher, “to get that same amount of leverage a few years ago in California, your revenue profile from an RA contract would have had to be 50%.”

The investment case for a storage project in New England, New York and PJM is much different than in Texas and California. The reason, Repsher explained, is that price volatility in the PJM market, for example, currently does not and is unlikely to achieve what exists in California or ERCOT, because of how diverse those markets are geographically and types of energy resources. Repsher states that an investor and lender has to take a longer-term view for valuation of a storage project in New England and PJM. As the Northeast markets move forward with offshore wind and other technologies, the markets will experience increased volatility and the market structure will change to make the case for storage. Repsher adds, however, that the Northeast markets are still unlikely to get to where the markets are in Texas.

The Northeast markets, however, are not monolithic. Prueher explains that in PJM, the New York ISO and the New England ISO, different nodes perform in different ways. The volatility of an energy node in New Jersey, for example, has a very different profile than a PJM node in Western Pennsylvania. Mark Repsher from PA Consulting gave the Delmarva Peninsula as another example. Approximately 10 to 15 GW of offshore wind is expected to be built off the Delaware shore that will be coming in on the same transmission line. Fossil fuel plants in the Delmarva Peninsula are shutting down, which will lead to volatility in those markets. “The Delmarva Peninsula already has a tremendous amount of volatility,” says Repsher. “The commonly-held view is that transmission grid upgrades are needed in that area but are not likely to be delivered quickly. This will therefore increase the importance of storage assets.”

Volatility in the near term can generate high ancillary service revenue opportunities such as we see in ERCOT.

Prueher says that lenders and investors are forming a fundamental view around price volatility and how to lend or invest in these markets. Says Prueher, “Storage feeds on volatility. Volatility in the near term can generate high ancillary service revenue opportunities such as we see in ERCOT. However, lenders and investors also worry about tail volatility. If renewable projects increase as fossil units retire . . . , you will continue to have, call it hour-ending 16 to 22 (i.e., between 4pm and 10pm) volatility as solar generation decreases as the sun sets and wind ramps up as the wind blows.” From a tail volatility perspective, lenders in California and Texas have confidence about the value of storage, not just for ancillary services, but also in the value of the project’s energy product. On the other hand, lenders might question the tail volatility of loads in Zones J and K where 3 GW of wind will be coming in where it is close to relatively stable, long-duration fossil-fired generation. Lenders in New York, says Prueher, “will be more skittish about whether that tail volatility will exist than in California and Texas.”

The Benefits of Storage Portfolio Financing

The financing markets for storage have also evolved to the stage where banks will loan against a diverse portfolio of storage projects. By loaning against a diverse project portfolio, lenders receive the benefits of operational, revenue, and energy volatility diversification. Lenders will therefore provide better terms, and developers with greater leverage, when loaning on a portfolio basis. Greg Randolph confirms that a developer coming to the Green Bank to borrow on a portfolio basis against four-five projects will receive more favorable terms than by borrowing against a single project.

The project portfolio can also be across geographically diverse locations. Repsher says that lenders would loan against a storage portfolio having operating assets in California, ERCOT and New York, in which the projects on an individually basis might be difficult to finance based on their size and risk profile. Prueher agrees with Repsher. Says Prueher “In our case, we went to the market thinking that including CAISO projects in the same package with ERCOT projects would be more difficult to finance since a lender might not be interested in one market or the other, or would not be able to find a consultant to backstop all of the portfolio markets. Instead, we found there is an abundant universe of both consultants and lenders interested in underwriting the entire portfolio.” The added dimension, Prueher says, is that “since we began we better understand our weighted average cost of capital for a project at the company level that can now inform our hedging strategy” which enhances the company’s financing options.

The Market for Merchant Storage Projects

The bank credit markets are strong today for most segments of the storage market, but not everywhere for financing a merchant battery storage project. In Texas and California markets, lenders are generally receptive to financing a merchant front-of-the-meter storage project because of their comfort with nodal pricing and the liquidity of the markets in CAISO. Nodal pricing allows developers to demonstrate a large merchant storage project’s economic benefits in a financeable way, says Prueher. McNair explains that the banks focus on the duration of the margins projected for a particular storage project. “The financing community recognizes that there may be a very attractive scenario today if you’re the only battery in the market. But they want to know what your margins will look like once there are 1.5 GW or 2 GW of additional battery projects deployed, as are expected by the end of this year in California.” McNair says that debt providers have evolved significantly over the last 18 months. Banks want to understand, and get reasonably comfortable, that a project will have a durable ancillary market revenue flow, or will need to enter an RA contract or energy hedge with a counterparty, to produce a predictable revenue stream over the term of the loan.

Merrill Kramer Esq. is a project finance partner in the Washington, D.C. office of Pierce Atwood LLP, a national law firm. He advises energy project developers, investors, lenders and users in the development, financing and acquisition of energy and other infrastructure projects. Merrill has advised clients on over 100 energy and infrastructure projects representing more than $30 billion in invested capital.

Merrill Kramer Esq. is a project finance partner in the Washington, D.C. office of Pierce Atwood LLP, a national law firm. He advises energy project developers, investors, lenders and users in the development, financing and acquisition of energy and other infrastructure projects. Merrill has advised clients on over 100 energy and infrastructure projects representing more than $30 billion in invested capital.

This article was amended on March 4, 2022 to provide an updated chart from the most recent Wood Mackenzie report on the US Energy Storage market.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.