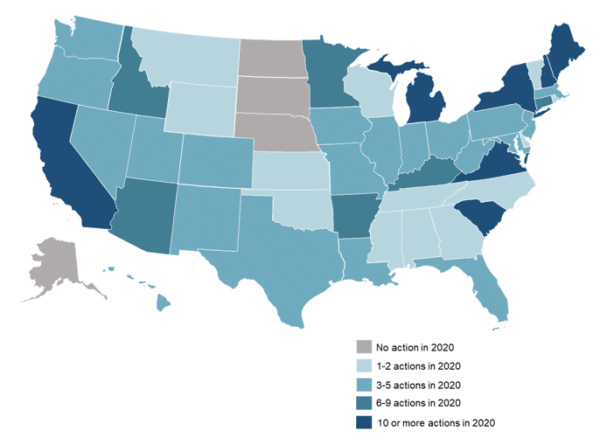

Forty-six U.S. states and the District of Columbia took some form of action on distributed solar policy and rate design changes during 2020, according to a new report from the N.C. Clean Energy Technology Center (NCCETC).

A total of 257 state- and utility-level changes were proposed, pending, or enacted by year’s end. The states taking the greatest number of actions included Virginia, California, New York, Maine, and South Carolina.

In the latest edition of its quarterly “The 50 States of Solar” report, NCCETC highlighted the top 10 distributed solar policy trends of 2020:

1. Utilities proposing additional fees based on system capacity

For distributed generation (DG) rate design, attention has shifted from demand charges to charges based on a customer’s DG system capacity. The New York Public Service Commission approved a net energy metering (NEM) successor tariff including a monthly customer benefit contribution based on DG system capacity. Both Evergy in Kansas and Dominion Energy in South Carolina proposed new fees based on DG system capacity during 2020.

2. States adopting unique NEM successor policies

NCCETC said states continue to operate as laboratories of innovation, adopting a wide array of NEM successor policy designs. In 2020, Arkansas and New York regulators opted to maintain retail-rate NEM for certain customers and approve new monthly fees. The Utah Public Service Commission established net billing credit rates compensating customer-generators at a rate between retail and avoided cost for exported energy. Iowa lawmakers chose to move forward with a value-of-solar approach, with rate changes not occurring until at least 2027.

3. States facing challenges with low-income community solar participation

Although the majority of state community solar policies include special provisions to encourage participation by low- and moderate-income customers, NCCETC found many states are still having trouble achieving this goal. In New Jersey, regulators are considering rule changes to streamline the income verification process, and in Oregon, regulators delayed the requirement for community solar project managers to reach the state’s low-income subscription target.

4. NEM successor tariffs being considered on a utility-by-utility basis

In Kentucky, three utilities filed tariff design proposals in 2020 as part of general rate cases, and in Michigan, regulators approved DG tariffs for Indiana Michigan Power and Consumers Energy. In South Carolina, Duke Energy and Dominion Energy have both filed successor tariff proposals, which are significantly different. Arkansas regulators are allowing utilities to propose NEM alternatives beginning in 2023.

5. States and utilities increasingly considering time-of-use crediting for NEM customers

In Utah, Rocky Mountain Power requested approval for time-varying credit rates for its net billing tariff, although the commission did not approve the proposal. Both Duke Energy and Dominion Energy filed NEM successor tariff proposals that include time-varying crediting in South Carolina.

6. Utilities continue proposing fewer and smaller residential fixed charge increases

In 2020, NCCETC found that 19 utilities proposed residential fixed charge increases. That compared to 31 in 2019, 34 in 2018, 41 in 2017, and 47 in 2016. The proposed increases were also smaller than in past years. The median increase proposed in 2020 was $2.47. That compared to $3.00 in 2019, $3.87 in 2018, $4.00 in 2017, and $4.07 in 2016.

7. Interest growing in minimum bills

NCCETC said utilities and other parties are increasingly interested in minimum bills as a DG rate design element, particularly as an alternative to demand charges, capacity-based charges, and fixed fees. In South Carolina, Duke Energy and solar stakeholders filed an NEM successor tariff proposal including a monthly minimum bill, while Virginia regulators authorized a minimum bill for shared solar customers. In Kansas, Evergy proposed a minimum bill as an alternative to a DG capacity-based charge.

8. States considering expansion of existing community solar programs

In 2020, South Carolina regulators reviewed existing community solar programs and directed utilities to make filings for new programs. In Virginia, lawmakers enacted bills establishing a shared solar program and a multi-family shared solar program, building on the state’s utility-led community solar program. New Jersey legislators also considered a bill making the state’s pilot community solar program a permanent program, with the Senate passing the bill during the year.

9. Strong movement away from mandatory residential demand charges

NCCETC said no investor-owned utility proposed a mandatory residential demand charge in 2019 or 2020, indicating a shift away from demand charges as a rate design feature for residential DG customers. The Kansas Supreme Court also ruled in April 2020 that Evergy’s mandatory DG customer demand charge was in conflict with state law. Evergy was the only investor-owned utility with a mandatory DG customer demand charge in effect, according to NCCETC.

10. States establishing timelines for NEM successor transitions

Many states are setting specific dates or aggregate capacity thresholds for the consideration or implementation of NEM successor tariffs. Virginia lawmakers enacted a bill increasing the NEM aggregate cap and directing regulators to develop a NEM successor when a certain installed capacity threshold is reached. In Arkansas, regulators authorized utilities and other stakeholders to file NEM alternatives beginning in 2023, and Iowa legislators enacted a bill directing regulators to develop a value-of-solar methodology for future tariffs in 2027.

“As states consider changes to the mechanisms by which customer-generators are credited for their exports, the stage is set for further evolution in the future,” said Brian Lips, senior policy project manager at NCCETC. “In 2020, policymakers in a number of states opted to retain their current net metering policies while opening the door to new rules in the future.”

NEM reforms led distributed solar policy activity in 2020. Autumn Proudlove, lead author of the report and senior manager of policy research, said NCCETC expects to see this trend continue in 2021.

More info on the report, which also includes fourth-quarter 2020 stats and the Top 10 most active states of the year, can be found here.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.