Sunrun started 2020 relatively unaffected by the Corona virus, but like every other residential solar company, Q2 was where the impact was felt.

Sunrun deployed 78 MW in Q2, down from 97 MW in Q1 2020 and its lowest total since 2018. It’s a significant hit but it appears to be more about process than market demand as Surun adapts and optimizes its “digital sales and streamlined operating model.”

And while Sunrun has been adapting to the new normal in the U.S., it has had an enormously busy summer as the dominant player in the home energy marketplace.

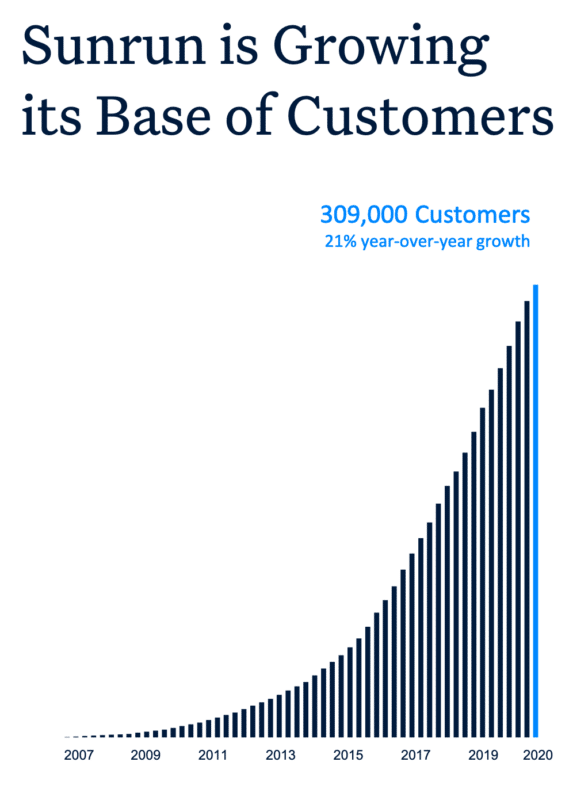

- In July, Sunrun announced that it was to acquire Vivint Solar — creating a residential solar giant with a combined customer base of more than 500,000.

- Also in July, Sunrun and SK E&S co-invested in a new venture with plans to conduct R&D in home electrification and the adoption of renewables.

- Still in July, Sunrun announced exclusive partnerships with three Community Choice Aggregators (CCAs) in California, which collectively provide power for one million homes in the Bay Area, for co-marketing and building virtual power plants.

- In June, Sunrun announced Virtual Power Plant (VPP) awards with Southern California Edison and Orange & Rockland.

Q2 financial highlights and GAAP Results

- Total revenue was $181.3 million in the second quarter of 2020, down $23.3 million from Q2 2019.

- Total operating expenses were $264.8 million, a decrease of 1% year-over-year.

- Net loss attributable to common stockholders was $13.6 million, or $0.11 per share

- Megawatts deployed were 78 MW, compared to 103 MW in Q2 2019, a 24% year-over-year decline.

- Creation cost per watt was $3.72, compared to $3.33 in the same quarter last year, a 12% year-over-year increase.

Outlook

According to the residential energy leader, “Order volumes have increased significantly, now above February levels, and management expects to grow megawatts deployed by over 20% sequentially in the third quarter, at improving unlevered NPV levels. We expect unlevered NPV to increase to above $8,000 per leased customer in the fourth quarter.”

Customer margin was approximately $3,800 in Q2, a decline caused by lower volumes, according to Sunrun. Margins are expected to increase to over $8,000 per customer in Q4.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.