An analysis of permitting and Google search reveals that the coronavirus pandemic has had less of an impact on residential solar year-over-year growth than most might expect. The key findings are discussed below with an interactive dashboard available here.

Permitting volume

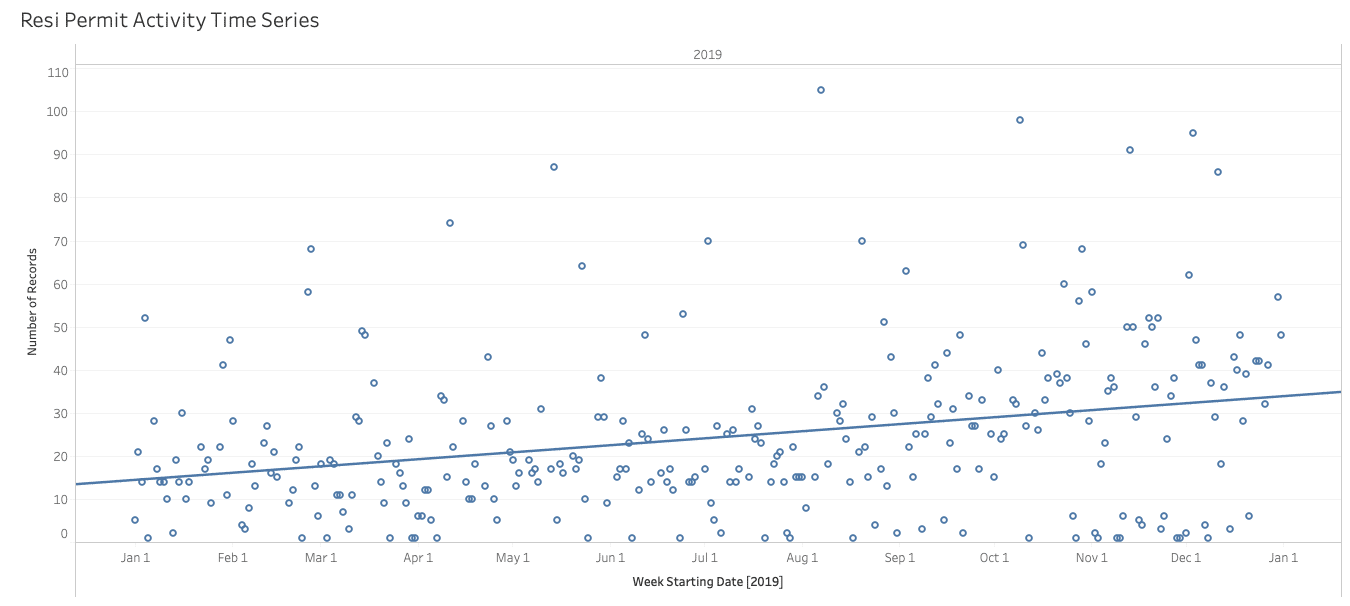

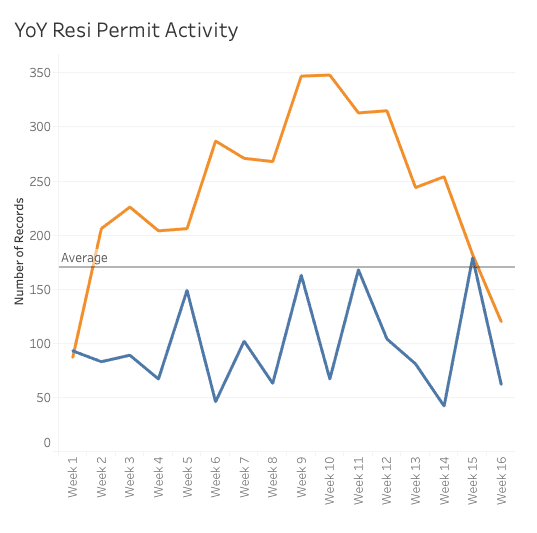

Permitting data from a diverse set of cities across the country reveals a significant increase in solar installs towards the end of 2019, fueled by the rush to take advantage of the full 30% Investment Tax Credit (ITC). This momentum carried on into 2020 and softened the blow of coronavirus in terms of year-over-year growth.

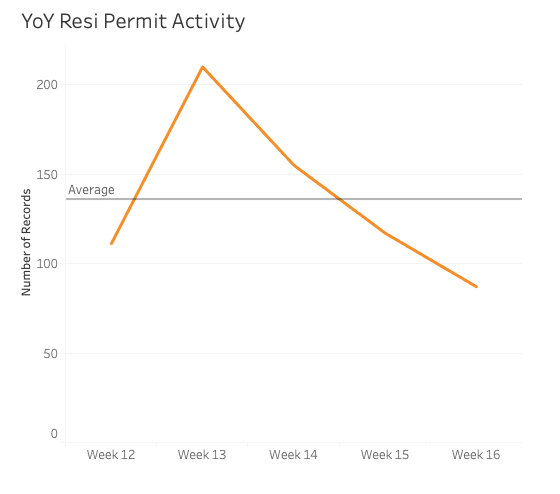

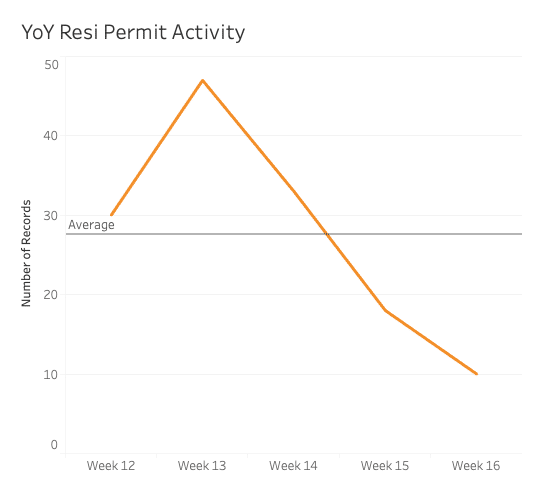

Permitting has decreased since the beginning of the lockdown period, but total installations remained above Q1 2019 numbers until April 6th of this year. That’s three weeks after lockdown began in some places around the country.

Google search data

Door-to-door and in-person sales for residential solar are off the table during the coronavirus lockdown, meaning that the primary sales strategy for many residential solar installers has shifted from conventional outbound channels to one that is predicated upon digital advertising and inbound marketing.

Given this, Google search data shows that consumer interest in solar since the beginning of the crisis in the U.S. has decreased by 43% since the beginning of the lockdown period.

Among the states that have seen the greatest increase in solar interest: Arizona, Georgia, Minnesota, Idaho, and Wisconsin.

And the states with the greatest drop in consumer sentiment: Alabama, Florida, Hawaii, New York, Tennessee.

Local vs. national installers

This analysis also addresses whether coronavirus has impacted national installers differently: Among the national installers, consumer interest fell the least for Vivint with just a 2% drop since lockdowns began. This contrasts with Sunrun and Tesla, companies that experienced respective drops of 55% and 80%.

Crucially, local installers are being hit harder than national ones by the pandemic. Permit volume is down for everyone, but local installers have suffered a decrease that is 45% worse than that faced by the three biggest players in the industry: Sunrun, Vivint, and Tesla. With nationally recognizable brands and large marketing budgets, national installers are better positioned to capture inbound consumer interest amidst the pandemic.

Moving forward

The data confirms what everyone already knows—residential solar has taken a hit both in terms of installations and consumer interest during the pandemic. However, not all installers are affected equally. With a shifting sales game, those already familiar with inbound marketing and digital advertising are best suited to persist the pandemic.

Forcing solar to refine an online sales business model may ultimately prove to be a good thing in the long run. Solar has notoriously suffered from high customer acquisition costs which have only been increasing in recent years. Installers that manage to build out a robust online sales model in 2020 may not just manage to survive coronavirus but could return thriving in future years with healthier margins.

Right now, the big players like Sunrun are best positioned to manage a pivot to digital given their brand recognition and resources. However, there is a silver lining for local installers: digital ads have precipitously dropped in price in recent weeks. A door has opened for them to build brand awareness and build out an effective digital sales game. If companies can pivot quickly enough to adopt tech-enabled sales strategies, 2020 may be an inflection point for residential solar such that the industry bounces back stronger than ever before.

***

Wes and Raymond are cofounders of Civology, a startup leveraging advanced technologies to combat climate change. Contact hello@civology.com for questions or requests for additional analysis.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.