Yesterday Solar Energy Industries Association (SEIA) announced what it has presented as an “ambitious goal” and an “aggressive target”: For solar to comprise 20% of all electricity generation in 2030, as part of its “Solar+ Decade” plan.

As the only publication we know of that calculates and publishes the annual portion of electricity from solar when the U.S. Department of Energy releases its statistics every year, and as a publication that has looked closely at the historical growth rates of solar, we found this number a reasonable forecast, but neither aggressive nor ambitious.

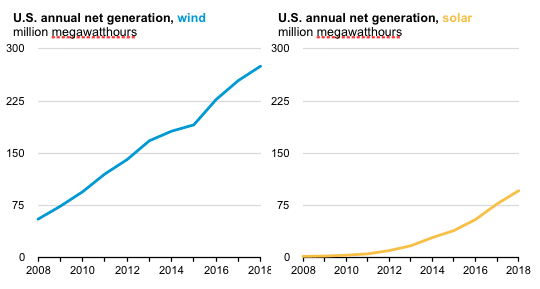

As we’ve reported, the portion of electricity supplied by solar has increase 48x in the 11 years from 2008 through 2018, with a 47% growth rate, meaning doubling every two years. And while that rate slowed in 2017 and 2018 – due to both the “hangover” from the expected end of the Investment Tax Credit (ITC) and the interruption of the market from the Section 201 tariffs – these are short-term, not long-term challenges.

Of course, if the growth rate of electricity from solar were to return to above 40% for the next 12 years, solar would produce enough electricity to supply more than our entire electricity demand by 2030. We don’t expect that, and all major market observers agree that the growth rate of solar will slow. But by how much?

Under SEIA’s proposal, solar installations would still grow to 77 GW annually by 2030 – nearly 8x the amount installed in 2018. While a huge volume, this estimate means that growth rates will average 18% over the next decade. This is not just lower than the average for the past decade, but lower than any given year in a decade or more.

And while such a slowing of growth rates looks reasonable for a forecast, it’s hard to see that as ambitious or aggressive.

Let’s look at the details.

Geography matters

In recent testimony before a U.S. House subcommittee, SEIA CEO Abigail Ross Hopper estimates that in reaching the 20%, some states might have 70% solar, and others might have 5% or 10%.

The geographic distribution of solar is currently very uneven, with three states getting more than 10% of their annual electricity from solar and a number getting only a fraction of a percent. That is unlikely to change going forward, as some states have not only a substantial lead but much greater solar resource, higher electricity prices and most importantly greater political will to deploy solar.

However, currently large-scale solar and wind are either the cheapest form of generation or rapidly becoming cost-competitive across the continental United States and Hawaii. Additionally, solar is out-pacing wind in cost declines, which is unsurprising as it is a semiconductor technology and requires less steel, concrete and other heavy materials per unit of electricity delivered.

Additionally, mandating solar on new homes and commercial buildings – as has been done in California and a few towns – has the potential to dramatically reduce the cost of distributed generation.

As such the 70% figure seems fine for some states that are either in the lead now or have the potential to grow very rapidly – including California and some states in the South. Whereas the 5-10% figure is possible, but seems pessimistic and certainly does not look like ambition.

Declining marginal value meets solar plus storage

One of the arguments against solar reaching these high levels is that as solar levels increase, it sinks the mid-day price of electricity, and thus provides a declining marginal benefit to the grid. This phenomenon has been particularly highlighted in the work of academic Jesse Jenkins, who formerly worked for pro-nuclear think tank The Breakthrough Institute.

This is a real phenomenon and on its own would limit the penetration of solar on the grid. However, in his work that we have seen Jenkins ignored the coming presence of solar plus storage, and this is a damning oversight.

Hawaii has already approved contracts for solar plus storage plants where the capacity of the battery system matches the capacity of the solar project, at a price of 8-10 cents per kilowatt-hour. Given capacity factors in Hawaii, this means that most or all of the electricity output from the PV systems can be stored in batteries, and that these can provide electricity to the grid any time of the day or night.

There is no reason this cannot be replicated on the mainland. In our coverage we are seeing more and more pairing of solar with batteries, both for large-scale solar and distributed applications. With ongoing price declines for lithium-ion batteries, we don’t see this combination stopping any time soon.

The emergence of solar and storage “peakers” removes any concern about declining marginal value, and shows that solar can provide flexible power to meet demand similar to a gas plant.

The climate movement is ahead of SEIA

In understanding why SEIA would put out this forecast-as-a-goal, it helps to understand the politics of the organization. SEIA has worked overtime to court Republican support for solar, including in the South where the organization recently helped to lead a major policy victory that opens up South Carolina’s electricity market to competition.

As part of its strategy of courting Republican support to widen the base of support for solar, SEIA does not talk about climate change. And if you ignore the catastrophic danger that scientists are telling us that climate change poses, then there is no urgency for renewable energy to transform the electric grid.

But while the Republican politicians that SEIA is funding and wooing are mostly not concerned about climate change, much of the nation is. Climate activists and their allies in a newly emergent Left wing of the Democratic Party are now calling for the nation to transition to 100% renewable energy by 2030, as part of the Green New Deal. Policies carrying this branding are not only being enacted at the city and state level, and Washington Governor Jay Inslee is calling for 100% clean energy by 2035 in his presidential campaign.

SEIA has publicly distanced itself from the Green New Deal, with VP of Public Affairs Dan Whitten telling Reuters that the organization needs to “operate in political reality”.

There is no doubt that the 100% renewable energy proposal that is part of the Green New Deal lacks technical details, and many of us have critiqued aggressive 100% proposals as less practical than 80% targets, noting that the integration challenges grow exponentially as you get closer to 100%. Additionally, there is a substantial debate as to whether the ambitious social and economic proposals in the Green New Deal support or detract from the 100% renewable energy goal.

But by proposing a bold goal for decarbonization Member of Congress Alexandria Ocasio-Cortez (D-New York) and her allies provided vision, took the initiative, and transformed the debate. SEIA has provided no such vision, and by following this with a much less ambitious proposal for solar penetrations, the organization has further ceded leadership on this issue to the American Left.

A lot of work to be done

Where SEIA is correct is that for the rubber to hit the road, there is a lot of hard work to be done, and CEO Abigail Hopper outlined much of this in her testimony before the U.S. House. This includes work to open electricity markets, both at the state level and with grid operators and before the Federal Energy Regulatory Commission (FERC).

It also includes setting bold targets, with the renewable energy mandates at state level and the 100% clean energy targets set by cities and states providing a predictable environment for investing in solar and other forms of renewable energy. And of course there is the ongoing battle to keep utilities from undermining the economics of customer-sited solar by changing rates and dismantling net metering policies.

But while getting into the weeds and fighting out the details of policy is essential, there is still a need for vision. And if SEIA won’t lead with an ambitious timeline to decarbonize the electricity grid, others will.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

It is definitely strange. I looked at the SEIA’s projections for Texas (because it is easy to see ERCOT’s pipeline data) and they are projecting 7GW of new solar in Texas in the next 5 years. ERCOT already has 7.1GW with Interconnect Agreements to be built in 3 years. In 5 years Texas will have north of 10GW built and probably closer to 15GW.

Or Ohio which PV Mag had an article about projects that will take them to 1.2GW already approved, but again SEIA has them adding 1GW in 5 years.

So, it kind of looks like SEIA just takes the current queue, adds 2 years to the timeline and assumes that no new projects will be added.

Kind of like EIA’s coal projections in reverse.

I’d like to mention making your own clean power for less is about as fiscally conservative as you can get. As is not polluting, destroying things.

The majority of repubs are for RE because it conserves money and very reliable no one can shut off and doesn’t pollute our country.

It is the bought and paid for repub leaders that is holding it back. But economics is driving it now as the invisible hand takes over with solar getting so cheap it’ll sell for $1/wt retail in 3 yrs.

With NGOs putting installer, customers and banks together in mass buys it won’t cost the customer anything more than their present bill for 2 yrs, then near free for 20+ yrs.

That is 50% ROI/yr for 20+ yrs. Where else can you make that much reliable return for that long?

On storage li-ion works at retail pricing. At wholesale, not so much.

For instant the Hawaii example hides batteries real cost by averaging it with 5 kwh x $.04 solar generation cost though only storing 1kwh of generation.

But home, business, EV battery, generation, heat and cold storage is the low cost storage adding under $.04/kwh vs $.13/kwh for Powerpacks, $.23/kwh for Powerwalls, Tesla’s numbers.

EVs are the key with so much extra capacity barely used. It is this barely used for 200 mile EVs packs it’s been found out on Tesla, Volt/LG the more they are used, the more they like it and less degradation.

With 100 million by 2030 EVs will likely be the largest storage, on demand generation type.

So the EV won’t cost to charge and get a check instead. That along with 10% of an ICE to run, is hard to ignore.

Business is going all in for RE in the next 10 yrs as a fiduciary duty as costs less.

So solar, RE is coming and likely faster than thought because economics is now compelling.