Vivint Solar has now installed just over 1.1 GWdc of residential solar, across more than 161,000 individual arrays. The 1.1 GW has increased relatively consistently from 513 MW in Q1’16, showing a compound annual growth rate of 29% in that period.

The company installed 45.6 MW in the quarter, almost 13% growth over the 40.4 MW installed in Q1’18. Vivint expects its second quarter install volume to be between 52 and 55 MW, and they’re reiterating full-year guidance of 15% growth, from 196 MW to 225 MW.

The company has $288 million in cash and restricted cash available, $305 million in unused aggregation facility capacity, and $30 million in a forward flow loan agreement.

The company’s non-GAAP Estimated Net Retained Value, retained asset value that would remain after repaying all debt, increased to just over $1.1 billion, to a value of $9.48/share. The growth here was just under 30% for absolute dollars created, and just under 24% on a per share level. The Gross Retained Value broke just over $2 billion in the quarter, meaning $908 million in debts exist on the company’s books.

The company says this increasing value created is partially a result of its focus in higher quality installations, and paying sales people better for choosing better sites.

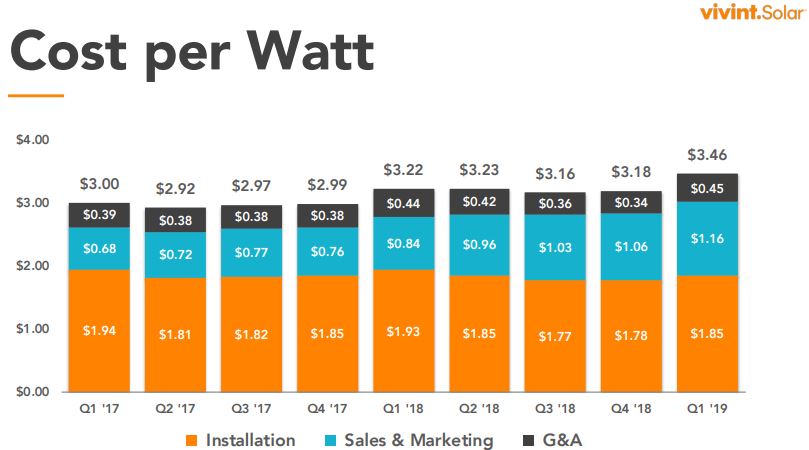

Vivint showed a growing cost per watt, broken down quite nicely in its Estimated Cost per Watt Methodology (pdf), at $3.46 – which was at the low end of Vivint’s guidance. This value increased 7.4% year over year, and a bit more from Q4’18’s value of $3.18/W.

These cost increases are driven by Vivint adjusting programs and compensation to compete with others who are vying for the same customers. This has driven the inflation in customer acquisition costs, where more of the economics are passed on to salespeople and the returns of some markets have decreased. The company expects the trend to continue. There was an uptick in general and administrative costs per watt also, but prior quarters showed such a jump that then returned to lower values.

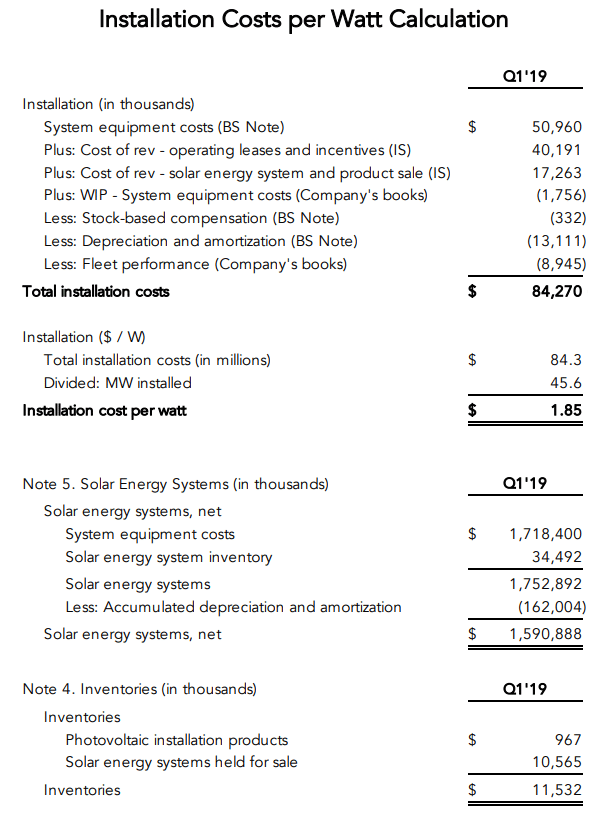

Nationwide, the average for installing residential solar is closer to $3/Wdc (with Tesla pushing lower recently). The costs of actually installing the solar (not counting sales, overhead and profit) have stayed flat over the last two years, this quarter at $1.85/W. It is possible that this higher cost could be sustained for longer periods as portfolio buyers look for the return on investment when buying secularized projects from groups like Vivint, and since a standard solar install can pay back far more than the 7-9% unlevered IRRs investors want, the machine will roll on quite nicely with that 99¢/W of retained value.

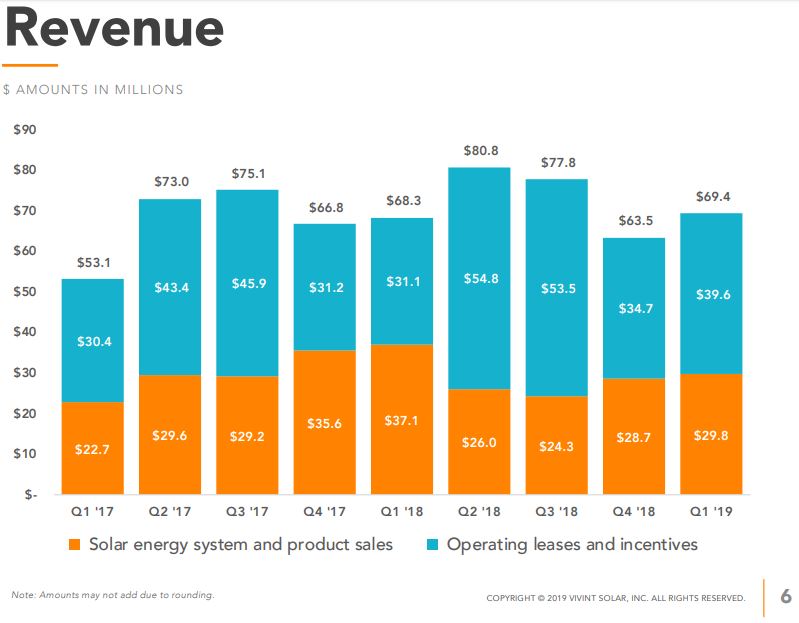

The year over year revenue growth (image below) was about equal to inflation at 1.6%, with a quarterly bump of just over 9%. If Q2-Q3 follows the pattern of the same quarters in 2017 and 2018, there should be healthy jumps in cash, before spending for the Q4 rush starts.

One noted change from Q1’18, and starting with Q2’18, is the significantly lesser volume of revenue coming from system and product sales. This past quarter saw 42% of revenue from such sales, versus 54% in 2018.

The company began to sell solar out of Home Depot stores in Q1, and recently signed agreements to operate in select locations with Costco and BJ’s Wholesale, but significant revenue isn’t expected from those venues until the second half of the year. Vivint says its inside sales closes the leads developed in these retail locations, with this sales channel representing a lower cost route to market, and becoming a larger percentage of its customer acquisitions.

Home builder relationships began to materialize with installs in the first quarter, and though there is a slowing in the California housing market as efficiency mandates kick in, a steady ramp up in this channel is expected. Interestingly, analysts noted that all three of the state’s large investor-owned utilities are working with regulators to increase their return on equity, and rates could go up by 12%. This was suggested by said analyst as a potential growth driver for the company in the state.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.