It’s that time of year again. The U.S. Department of Energy’s Energy Information Administration (EIA) has released its Annual Energy Outlook (AEO), providing a projection for the future of energy to 2050.

Before I get started on the deep problems with this year’s forecast and EIA’s projections in general, I want to note that like any serious energy journalist I rely heavily on the agency’s data collection and analysis in my work.

EIA is the official source for information on the current state of electricity in the United States, including the portion of electricity we are getting from different sources at the national and state level and even what projects are online.

Furthermore, EIA’s short-term forecasts have been generally thoughtful and informative. But when we start to look beyond a few years, EIA’s projections start to lose their credibility, and the assumptions that they make become increasingly problematic.

Getting the numbers right

Energy researchers have identified many problems with EIA’s analysis over the years. Last year when I covered AEO2018, I cited Rice University Professor Daniel Cohan, who noted that the system costs that EIA was using were not in line with those being reported by national laboratories. It was later revealed that EIA was using 2015 data. The agency gave reasons for this, but it still affects their projections.

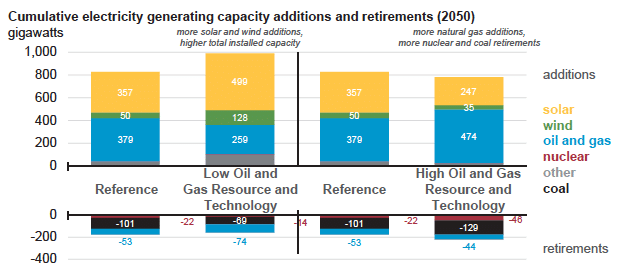

And while Alex Gilbert of the Vermont Law School describes AEO2019 as “much improved” regarding the data underlying its projections for solar, there are assumptions that remain highly problematic. AEO2019’s estimates for solar deployment are much higher than in previous years, but EIA continues to project that very little wind will be built after the expiration of the production tax credit – only 50 GW in total over the next three decades in its reference case.

The net result of this is that AEO projects that renewable energy will represent only 31% of the U.S. electricity supply in 2050.

I take less of an issue with the assumption that electricity demand will rise 1% annually to 2050. It appears that EIA is ignoring the flat electricity demand that we have seen over the last decade; and while increased electrification of transportation and heating is expected to boost demand substantially, EIA’s projections do not show substantial electrification of transportation.

But even with electrification of transportation driving increased demand, this will not happen evenly over the study period. EIA’s unreasonably optimistic view of near-term electricity growth – which it shares with the nation’s utilities – likely masks much more competitive wholesale market dynamics for the next few years, and this would unravel many of its assumptions.

Fossils forever

Along with this, EIA is projecting that the level of electricity generation from coal will soon stabilize, and the reference case shows our nation continuing to get 10-15% of electricity from coal each year through 2050, while exporting coal the whole time.

The first – projecting that coal will hold on – is in direct contrast to market trends, and ignores the terminal tailspin that the industry is in. No new coal plants are being built, and existing coal plants cannot compete with gas or renewables on price. Furthermore, the Trump Administration has been unable to back up its rhetoric that coal plants are essential for reliability with any real evidence.

EIA also projects that crude oil production will continue to set annual records through the mid-2020s and remain above 14 billion barrels per day through 2040. This is despite the growing market share of electric vehicles (EVs), which is already threatening to halt growth in global oil demand. But as it did with renewables in the past, EIA is assuming that EVs will not become a disruptive technology. (For an analysis of vehicle electrification and oil demand dynamics, see the Oil Fall series by Gregor MacDonald)

Along with this, EIA is also projecting ongoing growth in gas extraction in almost all cases, an increase in LNG exports, and the continued construction of large volumes of gas-fired power plants through 2050. The agency projects that natural gas will still represent 39% of electricity generation in 2050 at roughly 2,000 terawatt-hours annually, or 50% higher than 2018 levels.

No escaping climate realities

Unlike the coal predictions, the agency’s projections around gas could be reasonable, but only if man-made climate change were not a factor. Given the IPCC’s statement that we have until 2030 to dramatically reduce emissions or face potentially catastrophic changes, there is simply no way that we can burn the volume of gas that EIA is expecting.

EIA has repeatedly stated that their work is only a projection, not a prediction, and the agency assumes no new policies for climate or anything else. However, EIA also states that AEO2019 represents the agency’s “best assessment of how U.S. and world energy markets will operate through 2050”. And regardless of how EIA attempts to play both sides of this, the agency’s projections are used as predictions, including by many in government agencies and finance.

Beyond the problems already outlined, there are two larger problems with these projections: First, governments and corporations are taking action on greenhouse gas emissions. Second, energy demand is a feature of our civilization, and our civilization itself is threatened by climate change.

While the EIA puts out its projections, climate policies which will affect our energy mix are being implemented. Since last year’s AEO, California mandated a move to 100% zero-carbon generation by 2045, and five new governors were elected who are proposing 100% renewable energy mandates for their states. Meanwhile, a group of 9 governors on the East Coast have agreed to pass carbon taxes to pay for the decarbonization of transportation.

If these moves end up being inconclusive, cynics may say that we could still burn all this coal, gas and oil and simply doom our species. But given the accelerating number of climate-related disasters, our civilization may not even make it to 2050 without a major breakdown, which will reduce electricity usage and undermine the economic basis for building new plants in the first place.

We have already begun to see the first suggestions of this with an increase in blackouts due to severe weather events on the East Coast.

EIA is far from the only body that is putting out forecasts/projections which ignore climate change, persistently underestimate the growth of renewables and/or give an unrealistically long lifetime for the fossil fuel industries. The International Energy Agency has shown the same tendencies, and even DNV GL’s Energy Transition Outlook – while providing a highly sophisticated analysis of decarbonization technologies and pathways – gives an unreasonably large role for fossil fuels to 2050.

In the era of climate change such forecasts are absurd, but they have real-world effects in that they provide an undue degree of certainty for investors in fossil fuel industries, and undermine investment in cleaner alternatives. As such, EIA’s projections can be seen as part of the coal, oil and gas industries’ organized denial that their products must and will be phased out in order for our civilization to survive.

The larger point is that any forecast or projection that does not take climate change into account is divorced from reality, and there is a question as to the value of a “baseline” that ignores this central feature of our world. As such EIA’s Annual Energy Outlook has become at best more an exercise in econometrics than a meaningful look at the future of energy.

Correction: This article previously referred to AEO2019 as a “forecast”, but EIA prefers the term “projections”. We have changed the language in this op-ed to reflect EIA’s preferred term.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

IEEFA has a good article about EIA – The Energy (Dis)Information Administration:

On the retirement projection, EIA’s analysis ignores the existing coal fleet’s already advanced age. According to the agency’s own data, 88% percent of U.S. coal plants were built before 1990. More telling, on a capacity-weighted basis, the average age was 39 in 2017. Assuming that these plants will all be operating in 2050 borders on the ridiculous.

EIA also estimated last year that as the U.S. coal fleet ages, its average capacity factor will inexplicably climb to 70%—a level not seen since the mid-2000s, when the plants were younger and the electric power system operated in a much less coal-dependent fashion than it does today.

—

On their “forecast” of NG continued growth it is already slowing quite visibly. From FERC pipeline data:

Dec 2017: current cap=517.1GW, add=92.708GW, retire=10.803GW

Nov 2018: current cap=525.96GW, add=67.962GW, retire=11.081GW

Notice how planned additions of NG have dropped 25GW/26.7% while less than 9GW were built?

Same in Texas with ERCOT pipeline data (IA = Interconnect Agreement):

Dec 2017: Total: 13.969GW, IA: 10.088GW

Dec 2018: Total: 9.249GW, IA: 2.698GW

Planned additions have dropped 4.72GW/33.8% over a one year period.

Let’s compare this with solar:

FERC:

Solar:

Dec 2017: current cap=30.30GW, add=47.071GW, retire=0.002GW

Nov 2018: current cap=35.05GW, add=64.068GW, retire= 0.002GW

Increase of 17GW/36% while the capacity has grown 5GW.

ERCOT:

Solar:

Dec 2017: Total: 24.123GW, IA: 1.952GW

Dec 2018: Total: 40.732GW, IA: 4.337GW

Interconnect agreement additions are up 2.385GW/122% and total planning is up a whopping 16.6GW/69%.

Existing coal fleet capacity factor is indeed increasing on 2 levels; 1) retirement of old, inefficient & costly operating units (not entire plants); & 2) recent investments in “monopoly” G&T IOU or Cooperative coal plants that are the “backbone” of the respective Balancing Authority where they are located. [This is not my defense of this practice, simply an acknowledgement of its occurrence.]

Discussions of NG declining growth rates are overrated, whether within the midstream or at the new CCGT deployment level. The CCGT fleet was not deployed for high capacity factors, excess operational capacity is substantial, and something I argue here is nearly sufficient to shutter coal & natural gas steam turbine fleet in its entirety. Economics will drive this trend in the near term, whereas a national carbon policy would facilitate its immediate carbon reductions potential as RE deployments go through regional “boom & bust” cycles that are delaying carbon reductions during the “transition”. https://www.linkedin.com/pulse/could-us-shutter-coal-its-combined-cycle-natural-gas-fleet-hans-hyde/

There is no evidence from the EIA data that coal capacity factors are going up substantially although it does look like they have flattened somewhat in the last two years.

2013: 59.80%

2014: 61.10%

2015: 54.70%

2016: 53.30%

2017: 53.70%

2018 is running close to the same CF as 2017. I didn’t do a weighted average to account for varying monthly days just a straight average and came up with 53.79%.

Excellent assessment Christian Roselund and I agree, as well as share your acknowledgement that EIA is the clearing house of data for all our assessments, and we’d be blind without it.

Their other main failing, as you know, is their stubbornness to move beyond oil-based (BOE) energy accounting of our energy production and consumption realities… the Primary Energy “Sankey” diagrams… which bias favorably legacy Steam & ICE technologies at the expense of advanced 21st Century technology advancements.

It’s no wonder they can’t get projections “fine tuned” and consistent with developments across the energy sector… they are hell bent on maintaining apples to apples comparisons, when current realities dictate they look at an entire fruit basket and account accordingly

Thanks Hans.

Well written!!

Thank you.

Absolutely excellent article succinctly reporting the new reality. PV/Wind/Batteries are going to BOOM and the EIA just doesn’t get it … it is as simple as that. It is a very explainable when one realizes forecasting is based on the past record — a valid approach EXCEPT when crossing an Inflection Point. The new reality is that once PV/Wind became the nominally least expensive source of energy or anywhere near that, the whole world of predictive analysis changed. This is even further true as the real “Life” in LCC of these technologies is yet to be accounted for! Also, DOE SETO’s own SunShot program is now working to reduce the cost of PV by 50% again — it is the beginning of a new age for sure.

We are past the Inflection Point and there is no looking back … except by those who long for the glory days of coal and oil’s rule and will do all they can to keep their myth going.

EIA, like so many federal agencies (EPA, DHS, ICE) have all been changed into the arms of Trump’s twisted, greedy brain. Obviously there is a reason that they bend and break their own rules and (SEC) selectively enforce them. Trump’s fossil-fuel backed campaign now must pay the hands that fed him.

I don’t know; EIA has had issues with their forecasts since well before Trump took office. And they’ve actually gotten better about recording solar generation. This is a slow-moving part of DOE, and I don’t think they are as influenced by any given administration as other parts of the federal government.

Forecasts out to 2050 are mostly for entertainment purposes. Strong declarations made by the EIA, this author, or other prognosticators only show a lack of understanding of a 20+ year forecast. One variable, like declining reliance on coal, is difficult enough to predict. But compounding that by adding climate change, renewables, storage and its impact on the energy industry will almost certainly result in an inaccurate forecast.

Simply look at recent history… Just 15 years ago it seemed quite logical that natural gas would play an ever increasing role in power generation. It was the fuel of choice for nearly all new generating assets and the demand picture was quite rosy. It was so obvious to some that the industry built several LNG import terminals on US coasts. Most know the rest of the story… Billions were spent on assets pointed in the wrong direction. And billions more to retrofit them and turn them around. The best and brightest in the industry (energy companies, banks, PE) were all wrapped up in this.

This is not novel to the energy business. It happens all the time. I would guess that ‘unknowable variables’ have a greater impact beyond 2-3 three years than any other type.

Happy forecasting!

While I agree that forecasting out to 2050 is by its very nature a bit absurd, that does not excuse that projections like those produced by EIA have real-world consequences.

Furthermore, the EIA’s pretense that these are neutral scientific analyses is laughable. One need only look at the assumptions that coal’s decline will slow, or that electricity demand will magically rise again without the mass electrification of transportation, or that wind will not be deployed after the PTC is phased out to see that this is a political document and, as I stated in this article, part of the organized denial of the fossil fuel industries.

Oh yes, and they ignore climate change. Which makes this even more absurd.