The U.S. Department of Energy’s Energy Information Administration (EIA) has released new data on PV module shipments during the first half of 2018, which suggest that module imports have collapsed this year and which provides some insights into the level of hoarding that developers and contractors were engaging in before the final Section 201 ruling even came out.

EIA does not supply enough monthly data to actually compare import volumes, given irregularities in its Monthly Solar Photovoltaic Module Shipments Report. On the EIA site no reports are available for February and March and the latest edition provides import data for only the prior six months. Furthermore previous editions present the data in an inconsistent manner, so that no import numbers are available for November or December 2017.

Perhaps no one will be surprised that tracking solar data isn’t a top priority for EIA, which is more focused on oil and gas and which has consistently under-forecast solar market growth for a decade.

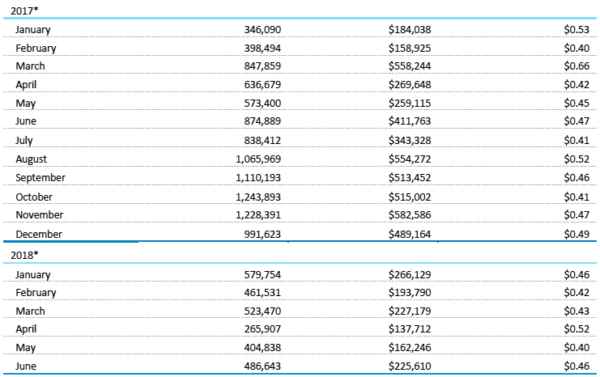

And while import data is incomplete, shipment data is clearly presented. And since at pv magazine‘s latest count U.S. module manufacturing was somewhere around 3 GW annually, (even with the optimistic assumption that the Tesla/Panasonic solar gigafactory is fully ramped) this reflects the imports which make up the large majority of modules installed in the United States. Total shipments fell by 2/3 in the second quarter of this year to only 383 MW per month from a peak in the fourth quarter of 2018, when an average of 1.15 GW of modules were being shipped each month.

Given that around 2.5 GW of solar was installed in the United States during the second quarter, it is inevitable that many of the modules installed this year had been sitting in U.S. warehouses. The shipment numbers in late 2017 confirm that solar developers and construction contractors were stockpiling modules to ensure an adequate supply of tariff-free product to at least build all the projects for which power contracts had already been signed.

Shipment volumes had already collapsed in January, confirming that even before the tariffs took effect manufacturers had sold out. The overall volume of shipments in the first six months of this year – around 454 MW per month – is 46% lower than average monthly shipment volume for the whole of 2017, which despite hoarding was lower than 2016 levels.

The report’s price data also provides insights into market conditions. During the first six months of 2018 pre-tariff prices averaged around $0.45 per watt, which is not much different from the final quarter of 2017. In contrast to reports by GTM Research, EIA does not show module prices changing much over the past 15 months (although the Section 201 tariff is not considered), with monthly average prices vacillating in the $0.40-$0.52 per watt range after falling in the second quarter of 2017.

Nor does EIA’s data show any impact of the recent global module price collapse due to Chinese policy changes. As these changes were announced at the end of May, June would be the only month covered by the report to show this. However average June prices are shown at $0.46 per watt, around the mid-range of the previous 12 months.

It is possible that these price declines had simply not hit the U.S. market yet. We will be watching these reports to provide you with updated snapshots on future developments.

Update: This article was updated at 9:30 AM on August 29, to reflect that EIA’s confirmation that their price figures are pre-tariff.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.