Utility rates have a direct bearing on the economics of distributed solar, and utilities are increasingly using rate cases to change their pricing structures to claw back more revenue and stop the growth of customer and third party-owned rooftop solar. One of the more common ways of doing this is to increase monthly fixed charges, even if it means reducing per kilowatt-hour energy charges. And yet the regulators who oversee these cases are often acting as an effective check on this trend.

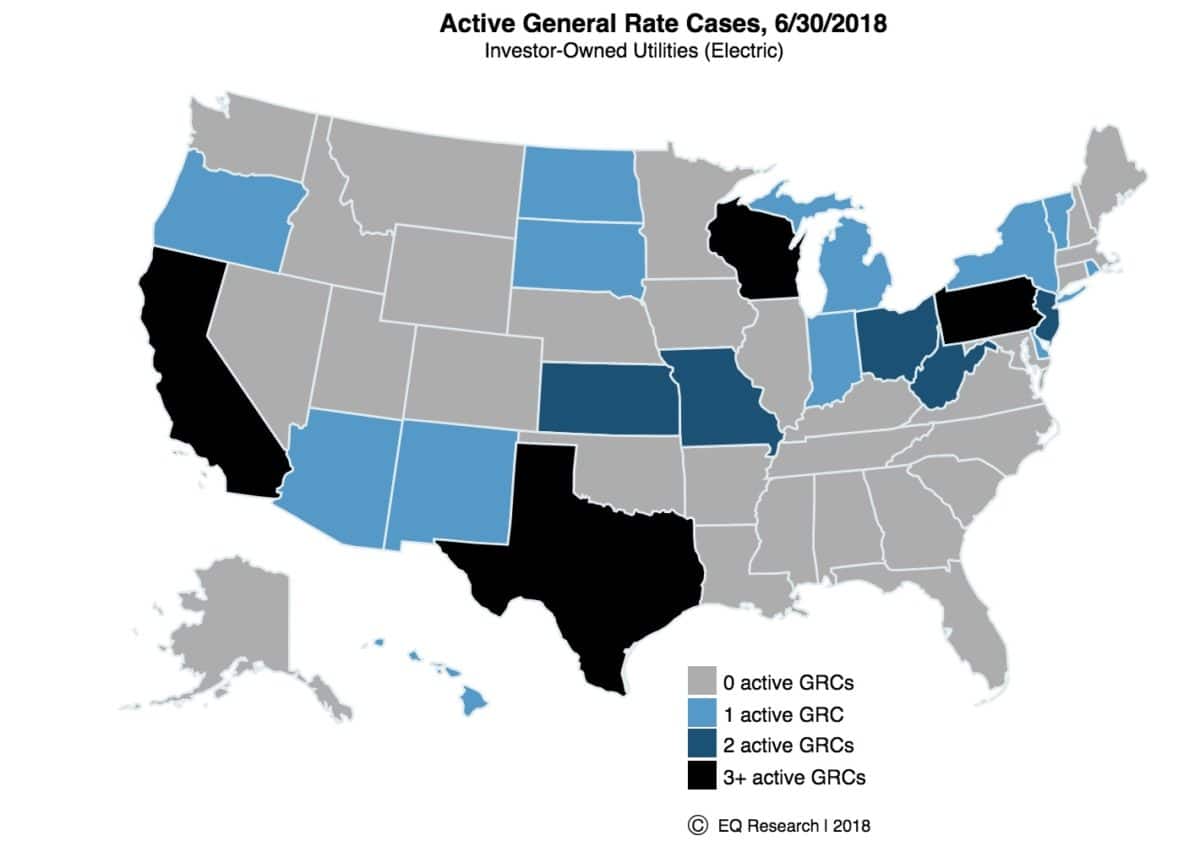

These trends were born out yesterday in analytics firm EQ research’s Q2 2018 General Rate Case Update outlining all of the actions taken in rate cases across the country; conclusions, introductions and cases pending. During the second quarter 14 cases in 10 states were initiated, 17 cases concluded and 39 remained unresolved and pending.

Proposals and Predictions

Of the 14 initiated rate cases this past quarter, 12 included rate-design revisions, with 11 of those being fixed charge increases.

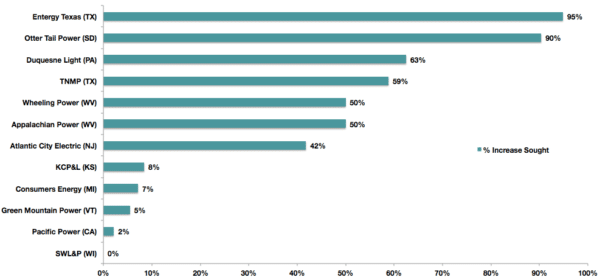

As the above chart shows the highest proposed increase was by Entergy Texas, at 95% which would almost double their monthly charge to $13.64, as compared to the current $7.00 mark. The average proposed rate change was 39%, which is interesting when the EQ’s next figure is taken into consideration.

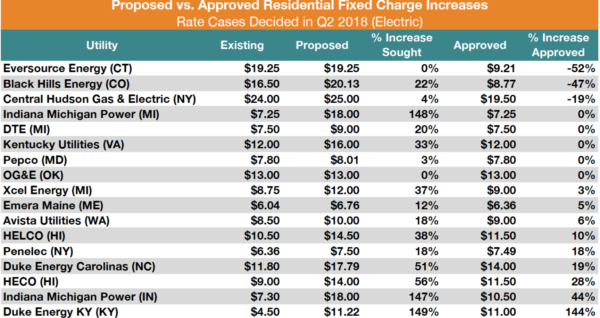

This figure represents all of the rate cases that were decided in Q2. When we look at the average proposed increase, it comes out at 44%, just a tick above the cases left unresolved at the end of Q2, providing some consistency. Another interesting point to note is that higher percentage proposed rate increases do not always correlate into higher increases allotted. This is important to keep in mind when thinking about Entergy Texas 95% increase proposal and Otter Tail Power’s 90% increase proposal.

In figure two, the only correlation between the three highest % increase proposals was that none of them were approved in full. Duke Energy Kentucky was granted 144% of 149% requested while, the two Indiana Michigan Power cases requested identical rates in their respective states at almost identical percentages. However, neither branch of the utility got close to what they were asking for, with Indiana being granted a 44% increase while Michigan got nothing.

While these numbers can provide context as to how utilities have fared in their quests for higher fixed charges nationally, Texas is it’s own beast and it would be naive to expect the decisions of other states to serve as factors in the Entergy or TNMP cases. It will be worth observing if the decision leads to consistent pricing among the two utilities. Of the 17 cases settled in figure two, three states; New York, Hawaii and Michigan, all had multiple cases settled. Hawaii and Michigan both had some level of consistent pricing, with both of Hawaii’s cases settled at $11.50 a month and all of Michigan’s rates being within $1.50 of one another. New York, however, had a $12 difference in the two cases that were settled in Q2, which was actually down from the previous difference of $17.64.

Trends: Q1 versus Q2

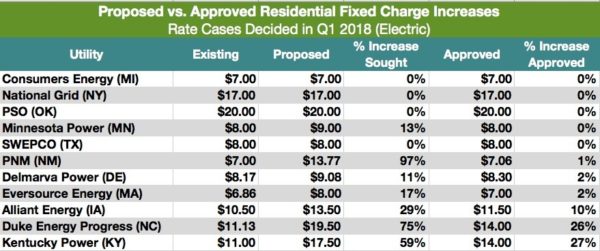

Q2 saw 17 cases settled, as compared to the 12 that were settled in the previous quarter, as shown in the graphic below.

What we see in Q2, as compared to Q1 are higher peaks and lower valleys: while the middle 11 cases are not drastically different, Q2’s three highest increases are all higher than Q1’s highest, while there were also three decreases in Q2, unseen in Q1. The average approved rate in Q1 was $11.08, which decreased to $10.32 in Q2. Meanwhile the average proposals and approvals in Q1 were 27% and 6% respectively, which both increased to 44% and 9% respectively in Q2. One last point of interest is that both quarters had nearly identical numbers of cases that ended as increases as did no change or decrease, at 6 to 5 for Q1 and 9 to 8 in Q2. In Q1 a case was 55% likely to result in an increase, which fell to 53% in Q2.

It is important to remember when reviewing this report that decisions can and do vary greatly from state to state, even when those states are dealing with the same utility.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.