The Kroll Bond Rating Agency (KBRA) has assigned a Vivint Solar bond offering a rating of A- as the company seeks $305 million from the market. A second batch of bonds, aiming to be worth $50 million, were rated BB-.

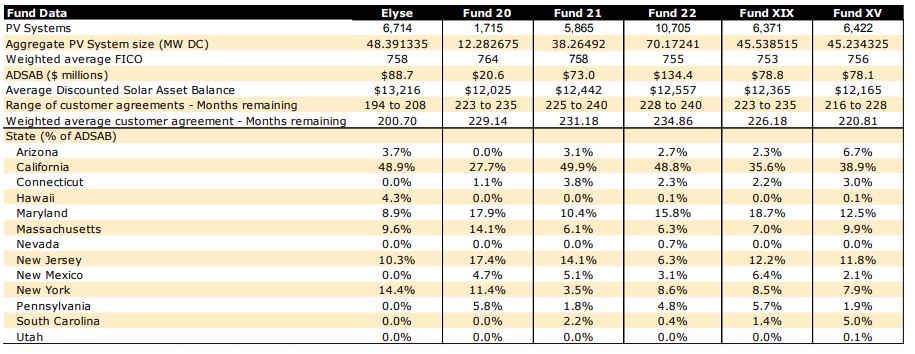

The portfolio is composed of 37,792 solar power purchase agreements (PPAs) and leases. PPAs make up 95% of the total value, and the rest are leases. The ‘total aggregate discounted solar asset balance’ (ADSAB) was approximately $494 million. This value is composed of “discounted payments of the leases, power purchase agreements (“PPA”), and hedged solar renewable energy credit agreements (“SRECs”)”.

The average agreement length, when it was signed, was 240 months, with the remaining time being 224 months. The weighted average FICO scores were 756.

The pre-sale report gives a logic for key credit considerations. Vivint Solar was rated an experienced originator and servicer, with the customers having a strong credit profile and relatively low delinquency rates. The transaction structure and the continuity plan of the manager, bankruptcy-remote subsidiary Vivint Solar Servicing, LLC (“VSS”) – also got positive marks.

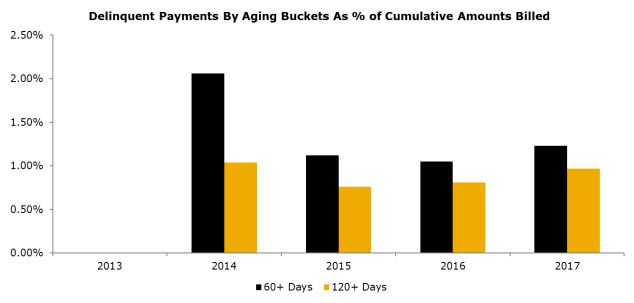

The negatives on the portfolio include a lack of historical data as Vivint is relatively new, as well as the potential for economic calamities. Whether or not solar leases can weather the storm of events such as the Great Recession is an unknown as of yet. Performance guarantees and tight geographical distribution (65.5% in CA, MD and NJ) were also identified as long-term revenue risks.

There is also an analysis on tax risk if it is later determined that Vivint overvalued the portfolios for tax equity investors relative to future fair market values. KBRA rates this a +/- since Vivint has protected investors via insuring the risk at LLoyd’s of London’s, among others, with tax loss insurance policies.

The company, per a third party engineering firm, showed production rates at 97.5% of the company’s original P50 production estimate. Conservatively, KBRA uses an annual degradation rate of just over 1% per year for its analysis, while nothing that the engineering firm projects a 0.75% rate over the lifetime of systems.

String inverters are projected to be replaced in years 10-12 at $1,000 each, while 11.7% of microinverters are expected to be replaced with string inverters in the same time frame at the same price.

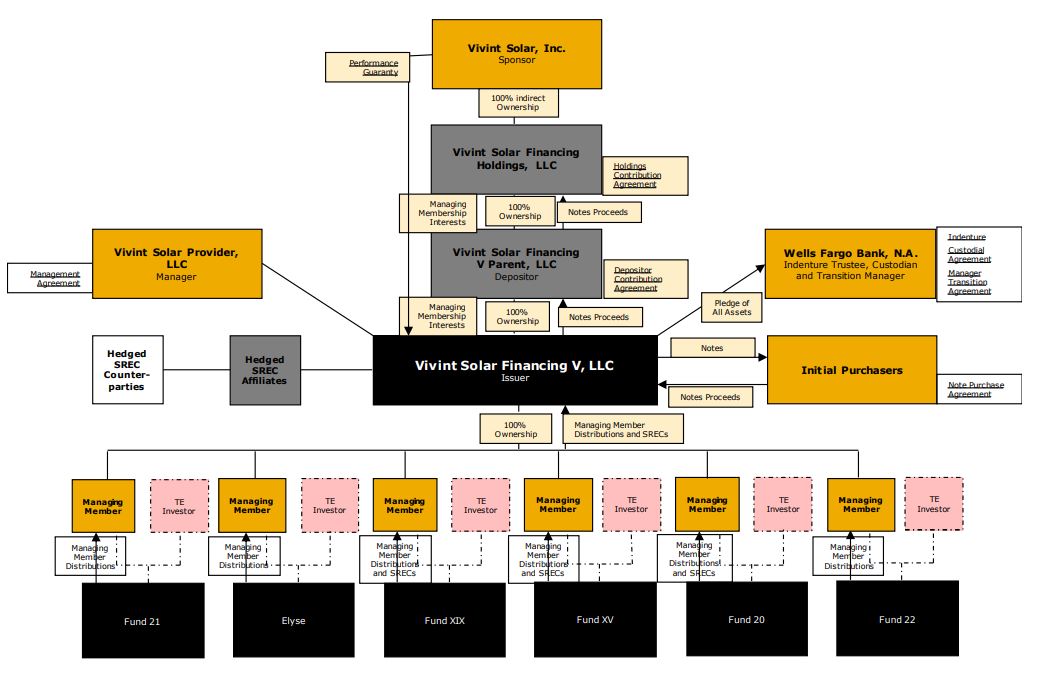

And in case you’re wondering what some of the magic sauce is, KBRA included a model of the transaction structure, and the many parties involved.

While Vivint Solar didn’t reach the AA rating KBRA gave to Dividend Solar recently, this is a continuation of the monetization of solar power portfolios. As these monetizations continue, and grow, various market actors gain experience with solar portfolios as assets, and liquidity increases. Liquidity increases give institutional investors, who control trillions of investable capital, perceptions of safety. And safety drives investment.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.