Editor’s note: This is the second in the #Solar100 Interview Series conducted by KWh Analytics and syndicated by pv magazine USA. The first interview with Danny Kennedy can be read here.

Even before his meteoric jump within weeks, starting at #40 and peaking at #3 on the #Solar100, we knew we wanted to catch up with Varun Sivaram.

Varun reminds us of the solar industry’s very own early Alexander Hamilton. Bold claim, we know. But hear us out:

- Both are polymaths. Hamilton studied math, medicine, and law at King’s College (now Columbia University). Varun studied international relations in college, and finished a PhD in condensed matter physics in two years on a Rhodes Scholarship to Oxford University.

- Both started careers as advisors: Hamilton held his first important public office as a colonel on George Washington’s staff when he was only twenty years old. Within the first decade of his career, Varun’s managed to hold a position as a Georgetown professor, as a senior advisor to the Mayor of Los Angeles and the Governor of New York, and as a McKinsey consultant advising C-level executives.

- Both have big ideas and are compellingly articulate about those big ideas: Hamilton for the American Revolution, and Varun for the ‘Solar Revolution.’

- Both are prolific writers. Hamilton is credited with most of the Federalist Papers. Varun publishes regular op-eds on clean energy, and he also has a forthcoming book with MIT University Press.

- Both are not afraid of going against the grain, and maybe even enjoy it. Hamilton was based in New York, the hub of loyalists, and still regularly and loudly challenged conventional thinking. Varun was recently cited in a NYT article titled, “Fisticuffs Over the Route to a Clean-Energy Future.”

- Both are influential spokespeople for their groups. Hamilton became the leading spokesperson for the Federalist Party. It is not difficult to imagine that Varun will represent a set of thoughts and people in the future of the solar industry.

While Varun is early in his career, having only finished his Oxford PhD from 2011-2013, he is undeniably scrappy and hungry, and he is already establishing himself as a thought leader in our industry.

—

A Happenstance Beginning

Richard Matsui: Your educational background is in International Relations and Condensed Matter Physics. What drew you to working specifically in solar?

Varun Sivaram: You know, it was initially a little bit of happenstance. Right out of high school I got a job working for Nanosolar, a CIGS company that went on to raise half a billion dollars. Nanosolar was the first company I had ever worked for, and it was infectiously optimistic. I learned everything I knew about solar power from Nanosolar—which was a very skewed way to learn about solar. I learned that today’s solar panels are obsolete, that the future will look flexible and lightweight, that silicon will be replaced by necessarily superior materials, and that the Silicon Valley model of disruption is going to work great for this entire industry. It turned out many of those things would be wrong, at least for the next decade. But I stuck with solar.

At Stanford, I studied Physics because I was interested in solar, as well as International Relations because I had always been interested in policy. And at Oxford, I applied to study under a scientist, Henry Snaith, who just so happened to be on the cusp of discovering perovskite photovoltaics, a technology that has rocketed to over 22 percent efficiency in just five years. I was so lucky—it felt like the most exciting place to be in all of academia. And I was the only person in the lab who had startup experience. It was an interesting perspective, having been at Nanosolar, and while I was doing my PhD I was watching Nanosolar explode.

And it hit me that even though everybody in academia thinks that perovskite’s going to be the next big thing, it probably is not going to work in this environment, because there are various external factors that make it really hard for innovative solar companies to go to market. And I thought, “You know, even though I’m likely in the best position possible from a science perspective, I need to go out and solve this problem another way,” and that’s why I eventually made my way into policy.

Controversial Bylines & Technology Lock-In

RM: Speaking of policy, of the thought pieces you’ve written for local papers, journals, or CFR, which, if any, do you think have been the most controversial?

VS: I think there are two pieces in particular that have been controversial. The first piece is a report I co-authored through the MIT Energy Initiative called, “Venture Capital and Cleantech: The Wrong Model of Clean Energy Innovation.” The Greentech Media guys just skewered us for that one because they basically asked, “How can this be true? We see cleantech is having all kinds of successes—look at all these software companies.” And we should have been more careful in choosing the title. Our title should have specified hard Cleantech—materials, chemicals and processes—those are the wrong kinds of companies for VCs to invest in.

The other controversial piece was an article I wrote for Issues in Science and Technology titled, “Unlocking Clean Energy.” It’s about technology lock-in, and here’s the situation: There are first generation clean technologies—silicon for solar PV, compact fluorescent lights for efficient lighting, light water reactors for nuclear, and corn ethanol for biofuels. And many of these first generation technologies make it really hard for the next generation to take their place. When that happens, I argue we get stuck in what’s called technology lock-in.

Some fields have managed to beat technology lock-in. For example, LEDs have beaten CFLs, and so efficient lighting is not a victim of technology lock-in. But other fields—nuclear is the best known example—have gotten stuck in technology lock-in because people were not forward-looking enough to invest in innovation. And as a result, nuclear’s share of world electricity peaked in the 1990s and has declined ever since.

I fear that we in solar are approaching technology lock-in. I also suspect that technology lock-in could take hold for lithium ion batteries. These incumbent technologies are getting so entrenched, and their costs are declining as a function of scale, that new technologies just won’t be able to break in.

The conclusion is that it is really difficult to get around lock-in. Some public policies can worsen the situation by entrenching the incumbent, such as the renewable fuels standard or indiscriminate tax credits. But other public policies on support for R&D and public procurement of emerging technologies can also help; for example, by procuring emerging flexible PV technologies for use in battlefield, the military could encourage technological succession.

That’s the article. People hate it, obviously, because it basically takes everybody to task. It says existing policies are often ineffective at countering lock-in, and that today’s solar industry—though it’s come a remarkably long way—is in need of disruption and technological change.

Why Write a Book?

RM: You’re the author of the forthcoming book, Taming the Sun. The back story for you personally is fascinating, and I’m curious— why did you write a book and what are you looking to add to the discourse?

VS: I wrote the book because I feel like I’ve been very fortunate to see solar from different perspectives: from science, from startups, from the McKinsey experience of analyzing utilities, and from making and assessing public policy at the state, national, and international levels.

Each of these different perspectives has an incomplete view of what solar will need. The scientists think that obviously the next theoretically superior material is going to win. The business people understand the business constraints best and so are understandably biased toward minimizing risk. For example, I’ve heard utility executives caution that, “Changing the grid’s clean energy make-up is like switching out the engine of a 747 in flight, so why would you go and add technology risk?”

These different perspectives mean that everybody comes to solar with their own siloed views. And there are also a lot of unbalanced headlines that pose an additional challenge for folks interested in learning about the field. Some argue that we already have all the tools we need for a 100 percent renewable energy future; others slam subsidies for solar as wasteful handouts. Folks don’t have a single one-stop place to go to get an even-handed story. That’s what I was trying to create. The book aims to present an authoritative, even-handed view of solar’s coming of age, including both the terrific progress that’s been made and the innovation that’s still needed to harness the full potential of solar energy: creative financing, revolutionary technologies, and flexible energy systems.

Solar’s Biggest Challenges

RM: On the topic of what needs to change, what do you think are the top three challenges coming up for the solar industry?

VS: When I think about the rise of solar over the next few decades, without three kinds of innovation—financial, technological, and systemic—solar could hit a wall. That would be catastrophic, because we need solar to anchor the transition to a nearly completely decarbonized power sector. Fundamentally, solar’s rise could stall because the cost of solar power, although it’s declining, could get undercut by its sharply falling value.

The three kinds of innovation collectively work together to ensure that solar’s value stays above its cost, so that it stays economically competitive:

First, financial innovation is needed to massively increase capital flows into the sector, continue solar’s near-term growth, and continue to drive down costs as the industry gains experience with producing and deploying solar PV. I know I’m preaching to the choir here, but the world’s biggest investors have overlooked solar so far, and for solar to continue its growth will require trillions of dollars in capital that existing sources are not going to be able to supply.

The industry faces the challenge of attracting institutional investors with appetites for long-dated, yield-oriented investment opportunities—solar lines up with this perfectly, but they just need a way to invest in it. In the developing world, however, oftentimes solar’s great advantages are overshadowed by country-specific challenges: political risk, currency risk, offtaker risk, credit risk, etc. Policymakers need to improve the investment environment to make solar’s inherently low risk and stable cash flows shine for large investors.

In summary, I think that solar needs financial innovation to help the industry access public capital markets, for example through securitization and maybe even the next generation of YieldCos. Data will be crucial to drive down the cost of capital, and firms such as kWh Analytics can enable investors to prudently invest in solar.

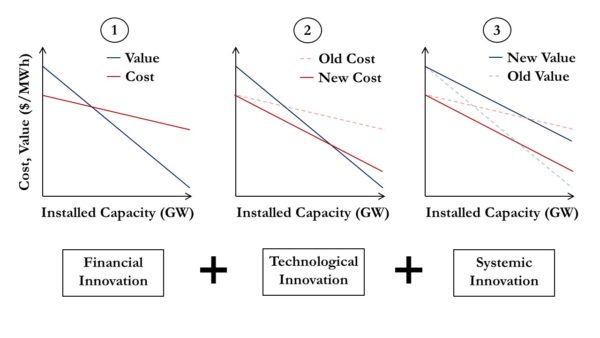

Second, technological innovation is also needed to bring down the cost of solar even faster. Let me use a figure from my upcoming book to explain why [figure appears below]:

Panel 1, on the left, plots the global average cost and value of the next unit of electricity from solar panels as the total installed solar capacity increases. Thanks to financial innovation, more and more solar panels get produced and installed, and the red curve shows costs declining steadily as a result (both axes are logarithmic).

Panel 1, on the left, plots the global average cost and value of the next unit of electricity from solar panels as the total installed solar capacity increases. Thanks to financial innovation, more and more solar panels get produced and installed, and the red curve shows costs declining steadily as a result (both axes are logarithmic).

But the blue curve shows how much a marginal kWh is actually worth, and that figure declines steeply as more solar power comes online in each region of the world. That effect, known as value deflation, occurs because solar starts to oversupply the grid in the middle of the day. We’ve already seen value deflation in a place like Chile. We had a bunch of solar on merchant contracts and then suddenly solar, in the middle of the day, started to get a price of zero dollars per megawatt-hour. And this is a problem that afflicts solar more than, say, a natural gas generator, because natural gas is dispatchable, whereas all the solar kilowatt-hours come at the same time. So, supply and demand tell you that with an oversupply of solar kilowatt-hours, you’ll have a mismatch in low prices with demand. A lot of people say, “Hey, solar won’t have this problem because it’s contracted on long term PPAs.” Those PPAs are basically masking the fundamental issue, which is value deflation. It doesn’t matter how you’ve done the contracting; if solar’s economic value is falling, you’ve got a problem.

Pretty soon, when solar produces 10 or 20 percent of the total electricity (kWhs) on the system, the value plunges below the cost. But with technological innovation, you can delay that point. Panel 2 shows the red curve falling more steeply, as new PV technologies, such as perovskites, enable dirt-cheap solar that falls in cost way faster than waiting for silicon PV to ride down the experience curve. New materials enable these cost reductions not just because they use cheap materials, but because they can be highly efficient, slashing balance-of-system costs. Still, I said that technological innovation only delays the point where solar value dips below cost. To prevent that from happening, we’ll need a third kind of innovation.

Third, systemic innovation is needed to prevent solar’s value from dropping so quickly, enabling it to remain above solar’s cost and making solar economically attractive. Systemic innovation entails reimagining energy systems, starting with the power system. A power system that can better match up solar supply with customer demand will mitigate value deflation by using every marginal kilowatt-hour of solar more effectively when demand is high. So in Panel 3, you can see that by adding systemic innovation, the blue curve becomes less steep—i.e., the value of solar drops less rapidly as more solar is installed. As a result, the blue curve always stays above the red curve, driving ever more solar deployment.

Systemic innovation encompasses modernizing the electricity grid, to make it bigger and also smarter. Connecting a diverse range of resources—from load-following nuclear plants to concentrated solar power plants with thermal storage to batteries to demand-side management tools—also helps to accommodate a high penetration of volatile solar PV on the grid. Another example of systemic innovation will be via sectoral linkage. For example, if you link the transportation sector by intelligently charging electric vehicles whenever there’s a surfeit of solar energy on the grid, or the heat sector by using electric heat pumps to track solar output, or even the water sector by modulating the operation of desalination plants, you’re basically making new ways to store intermittent solar power. This sectoral linkage reduces value deflation, because we will have many more valuable uses of solar power, no matter when it’s generated. And by keeping solar’s cost below its value, it can break through the ceiling that its penetration would otherwise hit.

RM: I hear you. My favorite iteration of that idea is that at some point, someone is going to realize that solar’s so cheap that you should hook up a Bitcoin mining machine to a solar panel. That could be a great way to make money from solar. Some day.

VS: Wait, hang on, that’s so interesting—Bitcoin is acting as a battery.

RM: Right. The same way that you’re describing desalination, it’s the idea of storing the value of energy not as energy but as something else that’s valuable.

VS: I love that idea. Has anybody written anything on this?

RM: No, it was my idea, but you should feel free to take it. You had already come up with the broad idea, I just said that specific iteration of it.

Data & Resource Based Financing

RM: As a data company, we think about data a lot. Are there areas for which you think data is uniquely positioned to cause systemic change?

VS: There’s a paper out from David Sandalow and colleagues from Columbia University called, “Financing Solar and Wind Power: Insights from Oil and Gas.” It’s interesting. They basically pick three different financing options from the oil and gas industry and ask, “Could we use this for solar and wind?” Data would help enable these options.

For example, in resource based financing, oil and gas companies get to basically take out loans in advance based on the value of the proven reserves, and they also get financing based on promising a cut of every barrel of oil they sell.

You can imagine a solar company could do the same with good data. Right now, banks think solar is too uncertain, and as a result it is hard for solar to get debt. A solar company with a parcel of land, plus good data on how much their projects produce in this particular area, plus an analytic model on how much money it will make—it would be a game changer if investors would look at that land that’s prime for solar development and value it for its solar potential, the same way that investors look at land with oil under it, and value the land for its oil reserves.

Call to Action

RM: It’s August 2017, and in the past few months, Trump announced that he’s pulling the U.S. out of the Paris Climate Agreement, some leading solar companies, such as Sungevity, have declared bankruptcy—my perception is that people in the industry are feeling quite down right now, even though our numbers on solar deployment and cost have actually never looked better. What would be your call to action or your parting thought for the people and the policy makers in the solar industry?

VS: I am infuriated with the Trump administration’s policy because first, I think the Paris Agreement is important for political and diplomatic reasons. And second, I think funding energy innovation through Trump’s budget proposal and supporting it through initiatives like Mission Innovation are really important, but he’s stepping away from both. He wants to slash energy innovation funding by half and cut support within the Department of Energy. I think that’s terrible.

Also, I think that profit compression in the solar industry, which we’re seeing both upstream and downstream, is an inevitable byproduct of a lack of innovation. If you’re making commodity profits and everybody’s trying to do the same, obviously you’ll have profit compression. The lack of innovation is what’s causing this compression. Given a commodity with no differentiation, no one makes any money. The fact that the value of solar is falling faster than the cost of solar—value deflation—is a critical problem for our industry’s future.

What is my call to action? Innovation funding in this country has stagnated for two decades. We certainly can’t afford for it to fall now. We instead need to strengthen it. We are not paying enough attention to this problem. Innovation is important both because it brings down the cost of solar to outrun value deflation, and also because it makes some producers more competitive than others, thereby enabling there to be profits in the industry. Innovation enables American companies to make money, as long as we’re the ones investing in innovation.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.