At the end of 2016, the U.S. residential solar market completed a fundamental shift. As reported by GTM Research, during Q4 the portion of third-party solar – leases and power purchase agreements – fell below 50%, meaning that direct sales are now the main business model for the sector.

As we have documented before, this has been in no small part due to the increasing variety of loan options which have become available for homeowners to finance PV systems, through an increasingly diverse network of providers.

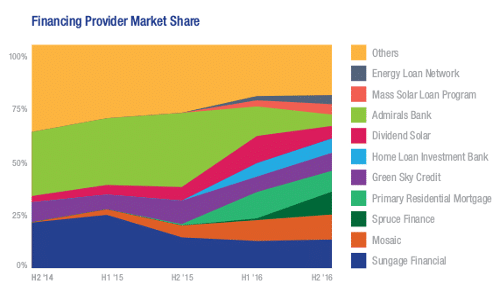

Yesterday EnergySage’s Market Intelligence report for the second half of 2016 provided further details as to just how diverse this network has become. The company affirms that among the top 10 loan providers through its online solar marketplace in the second half of 2016, no provider captured even 15% of the total market.

This fragmentation of the residential solar loan market has been very rapid. Only 18 months prior, two companies – Sungage Financial and Admirals Bank – provided 54% of the loans offered on the EnergySage marketplace. Today those two companies make up only 18%, with a host of new companies gaining share.

Among the loan providers gaining share is Mosaic, which entered the solar industry several years ago with a “crowdfunding” model which it said lowered the barrier to entry not only for loan recipients, but for investors in PV systems.

Mosaic came in second in market share in the second half of the year, followed by Spruce Finance. Spruce has rapidly gained market share in the EnergySage marketplace despite laying off staff without notice in February and rumors that the company is for sale.

EnergySage CEO Vikram Aggarwal says that he expects solar loan market fragmentation to continue, and offered two reasons for this trend. “First, more and more lenders, including banks, credit unions, and specialized loan providers are becoming comfortable with financing residential solar installations, as based on the success they’ve seen in the first-movers,” Aggarwal told pv magazine.

“Second, these lenders are beginning to understand that solar shoppers are valuable middle to upper-middle customers to support, as they not only have an interest in solar, but also in a variety of other home improvements, products and financial services.”

EnergySage is also getting in on the action with solar loans. In addition to the loans offered through installers on its online marketplace, the company began to offer financing directly last November, through agreements with BlueWave, Renew Financial and Wunder Capital.

LG, SolarEdge remain top brands

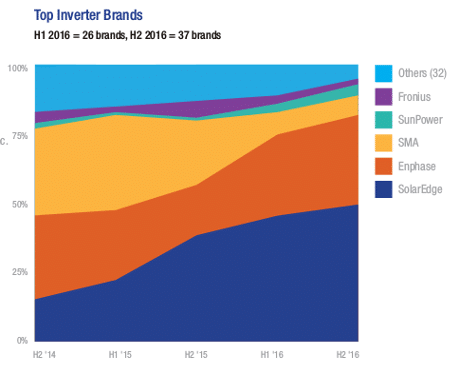

EnergySage’s report also provided information on the top brands of equipment provided through quotes on its marketplace, showing LG and SolarEdge and the top module and inverter brands, respectively.

While this is unchanged from the first quarter, the combined share of LG and the #2 module provider, SolarWorld, fell slightly to below 50%. At the same time Hanwha Q Cells and Centrosolar rapidly increased market share and joined the top 5.

Inverters showed the opposite trend. While 2/3 of providers on EnergySage offer two or more inverter brands, SolarEdge and Enphase increased their dominance of the market, together making up 81% of total quotes.

This is the second report where Enphase has increased its market share, in line with reports of business recovery and reversing a trend of market share losses in 2014 and 2015.

Falling prices

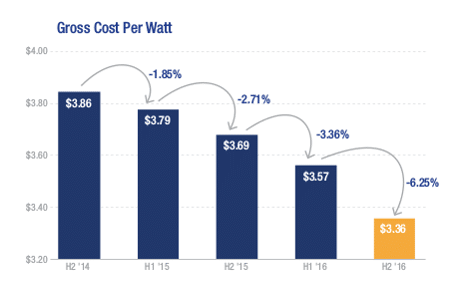

In addition to this information EnergySage documented the ongoing fall in system prices offered through its marketplace. During the second half of 2016 the company’s cost per watt fell by 6% – the greatest rate of decline in any report to date.

The average gross cost per watt of a system offered on the EnergySage marketplace was only $3.36 in the second half of the year. While this figure is not directly comparable to other reports, it appears to fall within the range of price estimates offered by Lawrence Berkeley National Labs and the U.S. Department of Energy’s National Renewable Energy Laboratories.

The fall in prices has been sharper in some regions than others. While the data shows that PV systems tend to be cheaper than the national average in the Sunbelt states of Florida, Texas and Arizona, this is also true for the Midwestern states of Illinois and Ohio.

New York and Massachusetts remained among the most expensive states for installed solar, these are also competing against high retail electricity prices. During second half of the year Florida and Virginia showed the greatest system cost declines, indicating that new markets offer opportunities for significant cost reduction.

As a result, EnergySage says that the LCOE of residential PV systems offered through its marketplace is now lower than residential electricity rates offered by select utilities in Illinois, New York, Virginia, Florida, California and Colorado.

Customers bought over $90 million worth of solar on the EnergySage marketplace in 2016 – more than double the level in 2015. Given the average cost per watt, this translates to somewhere in the neighborhood of 27 MW of rooftop solar PV.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.