Lawrence Berkeley National Laboratory (LBNL) is one of the most respected research organizations in the United States for solar research. For years the lab has been the definitive source of information on solar PV costs through their reports, both at the utility-scale and distributed levels.

Today LBNL released its ninth annual version of its Tracking the Sun report, which looks at pricing trends for distributed PV, as well as its Utility-Scale Solar 2015 report. Both of these reports look at 2015 pricing trends, and document ongoing progress at both scales.

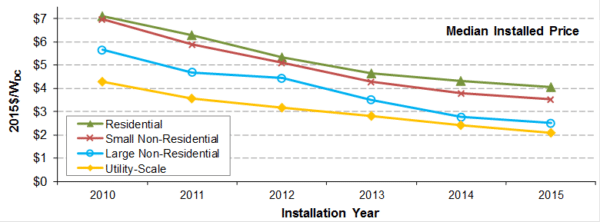

According to Tracking the Sun 9, average installed prices for distributed PV fell $0.20 per watt in 2015, 5% year-over-year for residential systems to around $4.00 per watt and by $0.30 per watt for “non-residential” systems, which includes the commercial and industrial market.

Since Tracking the Sun looks at “non-residential” systems at two scales, the average price declines were slightly different, with the larger systems falling 9% to around $2.50 per watt and the smaller systems falling 7% to $3.50 per watt.

Even larger price declines are being seen in the utility-scale segment, where prices have fallen 12% to an average of just over $2 per watt. However, this average conceals a wide range of actual prices, with the cheapest 20% coming in at under $1.60 per watt and the most expensive 20% at over $2.60 per watt.

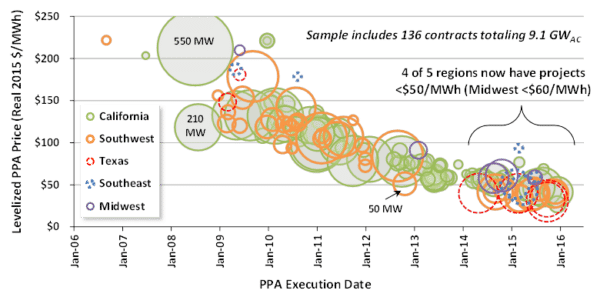

LBNL also documents the collapse in solar contract pricing which has been widely reported in pv magazine and elsewhere. Due to both lower installed project costs and higher capacity factors, the reports estimate that levelized power purchase agreement (PPA) prices for utility-scale projects have fallen by $20-30 annually on average from 2006 through 2013.

The result is that in 2015 most PPAs were priced at or below $50 per megawatt-hour, with a few at around $30/MWh. Researchers say this is enabling the geographic spread of solar PV. “Falling PPA prices have enabled the utility-scale market to expand beyond the traditional strongholds of California and the Southwest into up-and-coming regions like Texas, the Southeast, and even the Midwest,” stated Mark Bolinger of LBNL.

Along with this fall in price, capacity factors (CF) – the ratio of actual output to stated capacity – are rising for utility-scale solar. LBNL estimates a 21% CF for projects built in 2010, but a 27% CF for projects built in 2014. Part of this is the increased use of tracking systems. Only 12% of the systems built in 2010 utilized tracking, but this number had risen to 61% in 2014.

While these numbers are impressive, the trends of falling prices are continuing. LBNL notes that preliminary data for the first six months of 2016 shows continuing price declines in most states and market segments.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.