The U.S. solar market surges during the fourth quarter every year, as developers rush to finish projects – particularly large-scale projects – before the end of the year for financial and tax purposes. However, due to the particular circumstances of 2016 this year the end-of-year market boom began during the third quarter, leading to the largest quarter of installations to date.

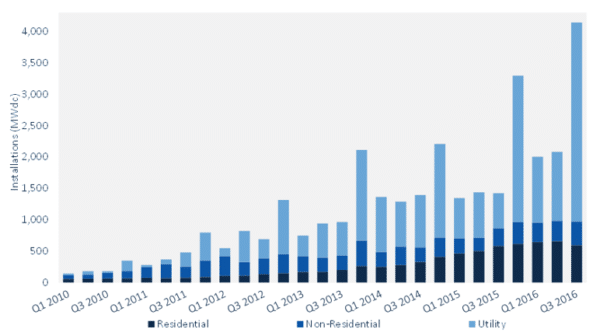

According to the latest report by GTM Research and Solar Energy Industries Association (SEIA), the United States installed a massive 4.1 GW-DC of solar PV during the third quarter of 2016, its best quarter to date. This was primarily due to a boom in utility-scale solar installations which were initially planned to come online by the end of 2016, before the 30% Investment Tax Credit was extended to 2020.

Utility-scale solar represented more than 3/4 of the new capacity that came online during the quarter, which was reflected in the states that saw the most installed capacity. Utah came out of nowhere to install 875 MW-DC, putting the state second only to California in terms of new market during Q3 and more than doubling its installed capacity in only one quarter. Texas also installed 374 MW – more than it installed during all of 2015, as the third-largest market during the quarter.

The “non-residential” sector, which includes commercial and industrial, non-profit and residential installations, showed a more modest 15% year-over-year growth rate to 375 MW-DC. The report authors say that part of this is due to community solar projects which are finally starting to come online, and which made up 20% of this segment.

Meanwhile, residential solar deployments grew only 2% year-over-year and actually declined quarter-over-quarter. While this segment still produced over 500 MW-DC of deployments, the report states that “changes in the sales cycles in mature state markets” such as California as well as regulatory and rate design challenges are making it hard for residential solar deployment to sustain its previous growth rates.

Even though regulators rarely grant all that is asked for, utilities have been chipping away at the economics of customer-sited solar – particularly residential solar – with a combination of attacks on net metering and rate design changes that force customers to pay more in fixed charges, meaning that net metering provides less value.

However, the state of the overall U.S. solar market still looks strong, at least for the near future. Report authors expect another 4.8 GW-DC of solar to come online during Q4, meaning that a total of 14.1 GW will be deployed over the full year. Furthermore, GTM Research describes a massive spill-over of projects into 2017, estimating that more than half the capacity which companies initially planned to complete by the end of 2016 has been pushed back into next year.

“Driven by a large pipeline of utility PV projects initially procured under the assumption of a 2016 federal ITC expiration, the third quarter of 2016 represents the first phase of this massive wave of project completion – a trend that will continue well into the first half of 2017,” said GTM Research Associate Director of U.S. Solar Cory Honeyman.

GTM Research has warned that the outlook becomes less clear after next year. The company notes a slow-down in power contract signings, due in part to utilities already procuring solar to meet renewable energy mandates several years in advance, despite current contract prices for utility-scale solar in the $35 to $60 per megawatt-hour range.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.